Students Centric

Placements Report

Trackable results, real numbers

Reviews

Proven success, real voices

Trainers

Expert-led, Industry-Driven Training

Life at IIDE

Vibrant Spirit student life

Alumni

Successful Journeys, Inspiring Stories

Learning Centre

Webinars

Blogs

Case studies

Live, Interactive Masterclasses

Fresh Insights, quick reads

Real-life, Industry relevant

More

Hire from us

Hire Top Digital Marketing Talent

Work with us

Join Our Team, Make an Impact

Customised Training

Personalised digital marketing training for your company

Refer & earn

Simple, easy rewards

Contact us

Get the answers you need

About us

Know more about IIDE

Explore all course options

FOR FRESH GRADUATES

Post Graduation Program in Digital Marketing & Business Strategy- Ideal for Age: 20–25 Years

Can’t decide? Explore all our

Digital Marketing CoursesCOMPARE ALL 3 PROGRAMSOnline & Offline

Explore Top AI CoursesIndustry-Aligned TRACKMost Popular

UG Program in Digital Business & Entrepreneurship- Ideal for 12th Pass out / FY Degree Student

PARTNER PROGRAMS

Can’t decide? Explore all

BBA In Digital Marketing Colleges

Orginally Written by Aditya Shastri

Updated on Jun 25, 2026

|3,871K+ views

Fonepay's SWOT in 2026 is the story of a platform that captured near-total dominance of Nepal's digital payment market in just six years and now faces the strategic question every dominant domestic player eventually confronts: how do you grow beyond the borders that made you powerful? Its strengths are structural and deeply moated; its weaknesses are mostly geographic and regulatory in nature.

Before diving into the article, I'd like to inform you that the research and initial analysis for this piece were conducted by Himanshi yaduka, a current student in the IIDE's Online Digital Marketing course batch, December 2025. If you found this helpful, feel free to send Himanshi yaduka a quick note of appreciation. It will mean a lot!

Before we break down each factor in detail, here is a snapshot of where Fonepay stands across all four dimensions:

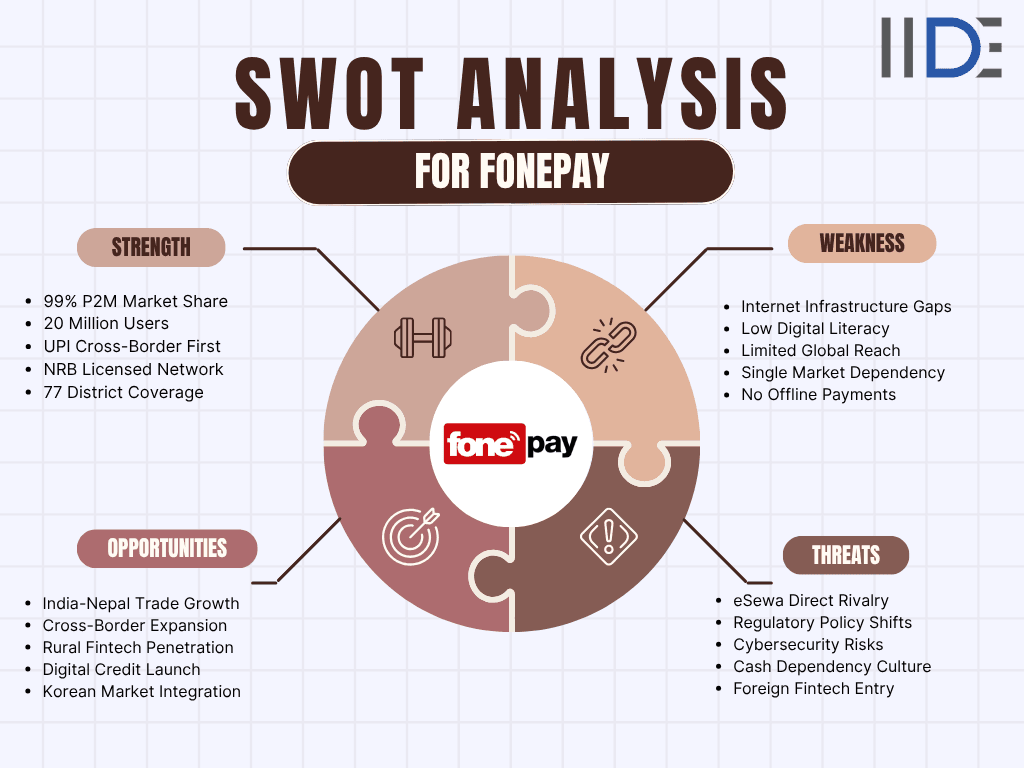

| STRENGTHS | WEAKNESSES |

|---|---|

| 99% of Nepal's merchant digital payments run on Fonepay | Revenue 100% dependent on Nepal, with no other market |

| 20M+ users; 1.8M+ merchants across Nepal | Poor internet in rural Nepal limits growth |

| Present in all 77 districts of Nepal | Indians can pay in Nepal via Fonepay, but not vice versa |

| Government-licensed payment network with global security certifications | No public revenue or profit figures available |

| Works offline too, even without an internet connection | Many registered users are not active daily users |

| Nepal's first digital credit card has 20,000+ users | Competes with eSewa under the same parent company |

| OPPORTUNITIES | THREATS |

| Enable Nepali users to pay in India via the same network | The central bank can change rules overnight |

| Korean tourists can soon pay at Fonepay merchants | Biggest cybersecurity target in Nepal's fintech sector |

| Sri Lanka payment corridor in progress | eSewa has a stronger brand recall among young users |

| Millions of rural Nepalis are still using cash, an untapped market | Global payment giants could enter Nepal |

| Government pushing digital payments for public services | Most Nepalis still prefer cash over digital payments |

| Major Nepali conglomerate now holds 14% stake | Rising digital fraud cases are putting user trust at risk |

Understanding Fonepay's competitive position becomes clearer when you see how Nepal's fintech rivals stack up, much like the battle explored in the SWOT Analysis of Paytm, where market dominance met unexpected disruption.

Learn Digital Marketing for FREE

- 45 Mins Masterclass

- Watch Anytime, Anywhere

- 1,00,000+ Students Enrolled

Learn Digital Marketing for FREE

- 45 Mins Masterclass

- Watch Anytime, Anywhere

- 1,00,000+ Students Enrolled

Strengths of Fonepay

Fonepay's strengths are not incremental competitive advantages they are structural moats built through regulatory trust-building, network expansion, and product innovation that no competitor can replicate quickly.

1. 99% P2M Market Share Near-Total Dominance

- Fonepay holds 99% of all person-to-merchant digital payments in Nepal.

- It also controls 62% of all person-to-person (P2P) digital transfers.

- On March 30, 2025, Fonepay processed a record 1,002,702 merchant QR payments in a single day totalling NPR 26.28 billion.

- No other fintech network in South Asia has achieved comparable single-country market concentration in the P2M segment.

Why it matters: 99% market share creates a self-reinforcing flywheel every new merchant joins because buyers are on Fonepay; every new buyer joins because merchants accept Fonepay. Breaking this network effect requires either a regulatory intervention or a categorically better product.

2. 20 Million Users and 1.8 Million Merchants

- Fonepay has 20 million+ registered users in a country of roughly 30 million people.

- Its merchant network has reached 1.8 million+ as of January 2026 spanning kirana stores, petrol pumps, supermarkets, restaurants, and major brands across all 77 districts.

- The Fonepay Credit Card, launched in 2024, is already accepted at 1.8 million QR merchant locations compared to fewer than 50,000 POS terminals available to traditional credit cards.

Why it matters: Network effects compound at this scale. Each additional merchant makes Fonepay more valuable to every existing user, and each new user makes the platform more attractive to every merchant considering joining.

3. NRB Licensed + PCI DSS + ISO 27001 Triple Trust Layer

- Fonepay is licensed by Nepal Rastra Bank as a Payment System Operator (PSO) received February 2020.

- It is the first non-card-based PSO in Nepal to achieve PCI DSS certification.

- It holds ISO 27001:2013 certification (information security management), achieved in April 2022.

- Every transaction is encrypted and authenticated through partner bank mobile apps no separate Fonepay wallet required.

Why it matters: Regulatory trust is the foundation of any payment network. No fintech startup domestic or foreign can replicate Fonepay's NRB licence, PCI DSS, and ISO 27001 combination overnight. These credentials form the highest entry barrier in Nepal's payment sector.

4. FoneTAG Nepal's First Offline Payment Solution

- FoneTAG is Nepal's first offline payment solution, launched February 2023, using NFC (Near Field Communication) and Customer Presented QR (CPQR) technology.

- It allows users to make merchant payments even in areas with limited or no internet connectivity directly from their mobile banking app.

- It directly addresses Nepal's biggest digital payment adoption barrier: unreliable mobile data outside major cities.

Why it matters: Every connectivity dead zone used to be a lost Fonepay transaction. FoneTAG converts those dead zones into active payment opportunities no competitor currently offers a comparable offline solution at this scale in Nepal.

5. Cross-Border UPI First in South Asia

- On February 28, 2024, Fonepay became the first network in South Asia to enable Indian tourists to pay Nepali merchants via UPI.

- Over 563,000 cross-border UPI transactions have been processed, totalling NPR 1.59 billion, saving NPR 31.8 million in forex outflow.

- 100,000+ Nepali merchants now accept Indian UPI payments across hospitality, retail, travel, and restaurants.

- Supported apps include PhonePe, Google Pay, Paytm, and BHIM.

Why it matters: The UPI integration opened a new revenue corridor linked to India's 700,000+ annual tourist visits to Nepal. It also positioned Fonepay as a cross-border fintech innovator not just a domestic payment utility.

To understand how India's largest payment ecosystem works and how Fonepay's UPI integration connects to it, read our detailed Business Model of Paytm.

Weaknesses of Fonepay

Fonepay's weaknesses are largely the structural flip side of being Nepal's dominant domestic platform. None are fatal but each limits the growth ceiling in ways that better infrastructure, policy change, and product development can eventually address.

1. Near-Total Single Market Dependency

- Almost 100% of Fonepay's revenue comes from Nepal a country with a GDP of approximately $40 billion.

- Any domestic regulatory shift, economic slowdown, political disruption, or NRB policy change hits the full business simultaneously with no geographic buffer.

- Nepal has experienced multiple political transitions and economic pressures in recent years that directly affect consumer spending and digital transaction volumes.

Why it matters: Market concentration risk is the silent weakness of every dominant domestic platform. Fonepay's size in Nepal is simultaneously its greatest strength and its greatest vulnerability.

2. Internet Infrastructure Gaps

- Nepal's internet penetration stands at approximately 65%, with reliable connectivity outside major cities still inconsistent.

- Real-time QR payments require stable mobile data every connectivity dead zone is a lost transaction.

- FoneTAG addresses this partially but NFC-enabled merchant terminal adoption is still limited to selected merchants.

Why it matters: Fonepay cannot grow rural market share beyond a structural ceiling until Nepal's connectivity infrastructure catches up. This is a macro constraint not a product problem but it directly limits addressable market size.

3. Reciprocal UPI Not Yet Live

- Currently, only Indian users can pay Nepali merchants via UPI Nepali users cannot yet pay in India via Fonepay.

- This reciprocal feature is pending regulatory approvals from both Nepal Rastra Bank and the Reserve Bank of India.

- Until it launches, Fonepay's cross-border utility is one-directional valuable for inbound tourism, but not yet for Nepal's large diaspora in India.

Why it matters: Nepal has millions of citizens living and working in India. A reciprocal UPI feature would unlock an enormous daily-use case for the diaspora that currently flows through informal money transfer channels.

4. Digital Literacy Gap Limiting Active Usage

- Acquiring 20 million registered users is one achievement; converting them into active daily users is another entirely.

- A significant portion of Nepal's rural population particularly older demographics still lacks the digital confidence to use mobile payment platforms independently.

- Fonepay does not publicly disclose active user rates, making the real engagement picture impossible to verify.

Why it matters: Passive registered users generate no transaction revenue. The gap between 20 million registered accounts and genuinely active daily users represents Fonepay's most significant untapped revenue pool.

5. Internal Competition From eSewa Same Parent Group

- eSewa, Nepal's first digital wallet, is also under F1Soft Group but operates independently from Fonepay.

- eSewa has 5 million+ active users and stronger brand recall among younger, urban Nepali consumers.

- Both platforms compete for the same merchant onboarding, co-branded partnerships, and user mindshare within the same parent ecosystem.

Why it matters: Internal competition within one parent group creates strategic tension resources, partnerships, and regulatory bandwidth must be divided rather than unified. This is a management challenge that external competitors simply do not face.

Opportunities for Fonepay

Fonepay's opportunity set is unusually large for a six-year-old company precisely because Nepal's digital payment market is still early-stage, and Fonepay controls its core infrastructure. Every major fintech trend in South Asia 2026 points in its direction.

1. Reciprocal UPI Nepali Diaspora Paying in India

- Plans are underway for Nepali citizens to make UPI-based payments in India via Fonepay, pending RBI and NRB approvals.

- Nepal has one of South Asia's largest diaspora populations in India millions of Nepali workers remit money home regularly.

- A reciprocal UPI corridor would make Fonepay the primary financial app for Nepali citizens in India, not just within Nepal.

Why it matters: This single regulatory approval could significantly expand Fonepay's addressable transaction volume by adding a diaspora use case that currently flows through informal and hawala-style transfer channels.

2. Korea GLN MOU New Tourist Payment Corridor

- Fonepay signed an MOU with GLN International (South Korea) in March 2024 to enable Korean tourists to pay at Fonepay QR merchants via GLN-partnered apps.

- GLN's network includes major Korean banking apps including Hana 1Q, KB Wallet, iMBank, Toss, and Hana Money.

- South Korea is a notable source of trekkers and tourists visiting Nepal's Himalayan regions.

Why it matters: Each new inbound tourist payment corridor adds transaction volume without any new domestic user acquisition cost. The Korea corridor follows the same proven model as the India UPI integration.

3. LankaPay MOU Sri Lanka Cross-Border Corridor

- Fonepay and LankaPay signed an MOU in May 2023 to explore cross-border interoperable payments between Nepal and Sri Lanka.

- A Nepal-Sri Lanka payment corridor would be the first of its kind in South Asia outside the India-Nepal axis.

Why it matters: Every bilateral payment corridor Fonepay builds before competitors creates a network asset that compounds in value over time. Early-mover advantage in cross-border South Asian fintech is a significant strategic prize.

4. Nepal Government Digital Push

- Nepal's government is actively promoting cashless transactions across public services tax payments, utility bills, government fees, and public transport.

- As the dominant payment network, Fonepay is the natural infrastructure partner for this institutional transition.

- Government-mandated digital payment adoption would give Fonepay near-captive, recurring transaction volume that no competitor can replicate.

Why it matters: Institutional payment volume is recurring, predictable, and high-frequency the most valuable type of transaction revenue for a payment network. Government adoption creates a stable baseline regardless of consumer sentiment.

5. Rural Fintech Penetration First-Time Digital Users

- Nepal's rural population remains largely cash-dependent, but smartphone adoption is rising steadily.

- NRB's financial inclusion mandate is actively pushing banks to onboard rural customers onto digital platforms.

- Fonepay's FoneTAG offline capability and 77-district reach give it a structural advantage in reaching first-time digital payment users.

Why it matters: First-time digital users are the most valuable long-term cohort for any payment platform. The first app used for payments tends to create lasting habits. Fonepay is better positioned than any competitor to be that first app for rural Nepal.

Threats to Fonepay

Fonepay's threats come from three directions simultaneously regulatory risk at home, competitive pressure from within and outside Nepal, and the stubborn pace of behavioural change in a cash-dependent society.

1. NRB Regulatory Policy Risk Overnight Exposure

- Nepal Rastra Bank controls every aspect of Fonepay's operating environment transaction limits, interoperability rules, fee structures, and PSO licensing conditions.

- Any change in NRB policy can fundamentally alter Fonepay's revenue model overnight a risk that no amount of market share can insulate against.

- Nepal has seen multiple NRB governor changes and policy shifts in recent years, each capable of resetting digital payment operating rules.

Why it matters: No level of market dominance protects a payment network from its central bank regulator. This is Fonepay's highest-impact, least-controllable risk.

2. Cybersecurity Nepal's Highest-Value Fintech Target

- As Nepal's largest payment network processing billions of rupees daily, Fonepay is the highest-value target for cyber fraud and system breaches in the country.

- Digital payment fraud cases in Nepal have been increasing in line with overall digital adoption growth.

- One major security incident could permanently damage the user trust that six years of network-building created.

Why it matters: Payment platform trust is binary users either trust it completely or they stop using it. A single high-profile breach can trigger user exodus that no marketing campaign can reverse.

3. eSewa's Brand Strength The Rival Inside the House

- eSewa is Nepal's first digital wallet, with 5 million+ active users and stronger brand recall among younger, urban consumers.

- Despite both being under F1Soft Group, eSewa and Fonepay compete for merchant relationships, co-branded partnerships, and user mindshare.

- eSewa's wallet model gives users a more direct relationship with their funds a perceived advantage for some consumer segments over Fonepay's bank-linked model.

Why it matters: In consumer fintech, brand familiarity drives daily usage. eSewa was in Nepali consumers' phones before Fonepay existed and habitual payment app users rarely switch without a compelling reason.

4. Foreign Fintech Entry Risk

- As Nepal's digital economy grows and regulation matures, it becomes an increasingly attractive market for global fintech players.

- Any regulatory opening that allows foreign payment giants to operate directly in Nepal could rapidly erode Fonepay's urban market share.

- The UPI cross-border integration is itself a double-edged sword it familiarises Indian tourists with scanning Nepali QR codes, but also normalises Indian payment apps in Nepal's retail environment.

Why it matters: Global fintech platforms bring marketing budgets, brand recognition, and engineering teams that far exceed anything in Nepal's domestic market. Their entry would not be a fair competitive fight on any dimension except regulatory and network advantage.

5. Cash Dependency The Deepest Structural Barrier

- Despite Fonepay's growth, Nepal remains predominantly cash-based particularly outside Kathmandu, Pokhara, and major urban centres.

- Changing deeply ingrained cash habits among older demographics and rural populations requires sustained behaviour change investment, not just product features.

- Cash offers zero transaction failure risk, no data requirements, and universal acceptance advantages that even Fonepay's 1.8M merchant network cannot fully match in areas with unreliable infrastructure.

Why it matters: Cash dependency is not a technology problem it is a trust and behaviour problem. Technology alone cannot solve it, and meaningful rural cash replacement in Nepal is measured in decades, not years.

About Fonepay

![]()

Think about how you pay at a chai stall in Mumbai, you open PhonePe, you scan a QR code, and the payment is done in three seconds. Now imagine building that same experience from scratch in a country where 95% of transactions still happen in cash, and most people have never owned a credit card. That's exactly what Fonepay did in Nepal.

Launched in 2019 as a dedicated Payment System Operator licensed by Nepal Rastra Bank, Fonepay was built to solve a problem every Nepali knew too well: sending money between banks was slow, expensive, and painful. Fonepay's interoperable network has changed that overnight, connecting banks, digital wallets, merchants, and consumers on a single platform for real-time P2P and P2M transactions.

Today, Fonepay connects 60+ banking and financial institution partners, serves 20 million registered users, and reaches 1.7 million merchants across all 77 districts of Nepal. It holds a 99% market share in person-to-merchant digital payments and 62% in person-to-person transfers. In 2024, it became the first network in South Asia to enable Indian tourists to pay Nepali merchants via UPI, a milestone that put Nepal's fintech ambitions firmly on the global map.

Before we get into the SWOT, here's a data-backed snapshot of where Fonepay stands today.

| Quick Stats Table | |

|---|---|

| Metric | Details |

| Founded | 2019, Kathmandu, Nepal |

| Parent Company | F1Soft Group |

| Founder | Biswas Dhakal (F1Soft) |

| CEO | Diwas Sapkota |

| Headquarters | Kathmandu, Nepal |

| Registered Users | 20 Million+ |

| Merchant Network | 1.7 Million+ |

| Banking Partners | 60+ Banks & Financial Institutions |

| Market Share (P2M) | 0.99 |

| Market Share (P2P) | 0.62 |

| Licensed By | Nepal Rastra Bank (NRB) |

| Coverage | All 77 Districts of Nepal |

| Key Milestone | First South Asian UPI Cross-Border Payment (2024) |

| Key Competitors |

eSewa, Khalti, IME Pay, |

What's Happening with Fonepay in 2026?

- On March 30, 2025, Fonepay processed a record 1,002,702 merchant QR payments in a single day, totalling NPR 26.28 billion with Indian UPI transactions among the contributors.

- Merchant network has grown to 1.8 million+ as of January 2026, with the Fonepay Credit Card now used across all 77 districts.

- Fonepay Credit Card has crossed 20,000 users operating on the QR network and giving access to 1.8M merchants, compared to fewer than 320,000 physical credit cards in all of Nepal.

- Khetan Group acquired a 14% stake in Fonepay in September 2025 , signalling strong institutional confidence in Nepal's largest fintech network.

- The GLN International MOU (March 2024) is progressing toward commercial launch, which would enable Korean tourists to pay via GLN-partnered apps at Fonepay QR merchants across Nepal.

- Reciprocal UPI enabling Nepali citizens to pay in India via Fonepay is pending regulatory approval from both Nepal Rastra Bank and the Reserve Bank of India.

Key Takeaways & Conclusion

Fonepay's rise from PSO licence in February 2020 to Nepal's dominant payment infrastructure, 99% P2M market share, 20 million users, 1.8 million merchants, and a record NPR 26.28 billion processed in a single day is one of South Asia's most underrated fintech success stories. The UPI cross-border integration, FoneTAG offline payments, Fonepay Credit Card crossing 20,000 users, and Khetan Group's 14% stake acquisition in September 2025 all signal that Fonepay is actively building the next layer, not coasting on existing dominance.

The risks are equally real. Near-total Nepal market dependency, NRB regulatory exposure, a cash-dependent consumer base, and internal competition from eSewa within the same parent group are not small problems. Fonepay has built a remarkable platform inside Nepal's borders. The question for 2026 and beyond is whether it can extend that platform credibly across them before someone else defines what cross-border South Asian payments look like.

The next chapter is not about adding more users in Kathmandu. It is about getting reciprocal UPI live, activating the Korea GLN corridor, and converting Nepal's cash-dependent rural population into first-time digital payment users all simultaneously.

Recommendations:

- Prioritise reciprocal UPI regulatory approvals with NRB and RBI. This is the single feature that unlocks the diaspora use case and meaningfully expands addressable transaction volume

- Fast-track Korea GLN corridor to commercial launch before any competitor occupies the Korean tourist payment space in Nepal

- Invest in rural digital literacy programmes alongside FoneTAG rollout technology adoption, which requires behaviour change support, not just product availability

- Publish quarterly transaction volume data to strengthen E-E-A-T and investor confidence as Khetan Group's institutional backing increases scrutiny

- Build a dedicated cybersecurity incident response infrastructure at 1.8M merchants and 20 users; the cost of a breach far outweighs any savings from under-investing in security

Want to Know Why 2,50,000+ Students Trust Us?

Dive into the numbers that make us the #1 choice for career success

MBA - Level

Post Graduate in Digital Marketing & Business Strategy

Best For

Fresh Graduates

Mode of Learning

On Campus (Mumbai & Delhi)

Starts from

Oct 1, 2026

Duration

11 Months

Live & Online

Advanced Online Digital Marketing Course

Best For

Working Professionals

Mode of Learning

Online

Starts from

Aug 7, 2026

Duration

4-6 Months

Online

Professional Certification in AI Strategy

Best For

AI Enthusiasts

Mode of Learning

Online

Starts from

Sep 8, 2026

Duration

5 Months

On Campus

Advanced Certification in Artificial Intelligence

Best For

AI Enthusiasts

Mode of Learning

On Campus (Mumbai)

Starts from

Sep 1, 2026

Duration

3 Months

Online or Offline

Top AI Courses to Make You Future Ready!

Best For

AI Enthusiasts

Mode of Learning

2–5 Month Program

Starts from

Sep 8, 2026

Duration

Flexiable

Offline

Undergraduate Program in Digital Business & Entrepreneurship

Best For

12th Passouts

Mode of Learning

On Campus (Mumbai)

Starts from

Aug 19, 2026

Duration

3 Years

Offline

Degree In 2026 ≠ Enough Degree + Digital Skills = Future-Ready

Best For

12th Passouts

Mode of Learning

At IIDE Campus

Starts from

Aug 6, 2026

Duration

3 Years

Recent Post

Interesting Reads

Frequently Asked Questions

Fonepay is Nepal's leading digital payment network, enabling seamless transactions via mobile banking and QR codes. It facilitates a wide range of services, including Person-to-Person (P2P) transfers and Person-to-Merchant (P2M) payments, aiming to drive the country's transition to a cashless economy.

Fonepay's key strengths lie in its extensive network of partner banks and merchants, its adoption of modern technologies like QR codes and UPI, and its commitment to expanding digital financial inclusion across Nepal. The succesful implementation of cross border UPI transactions, is a large advantage.

The rapid expansion of Nepal's digital economy, coupled with increasing mobile phone and internet usage, presents significant growth opportunities. Additionally, government initiatives supporting digital transactions create a favorable environment for Fonepay's expansion.

Fonepay competes with established digital wallets like eSewa and Khalti, as well as IME Pay, the bank-to-bank system connectIPS, and mobile banking services offered by individual banks, each vying for a share of Nepal's digital payment market.

The cross-border UPI system, a collaboration with NPCI, significantly boosts transaction volumes, especially from Indian tourists, and enhances Fonepay's role in facilitating international economic activity within Nepal, and strengthens ties between India and Nepal.

Lead Trainer & Business Development Head at IIDE

Aditya Shastri leads the Business Development segment at IIDE and is a seasoned Content Marketing expert. With over a decade of experience, Aditya has trained more than 20,000 students and professionals in digital marketing, collaborating with prestigious institutions and corporations such as Jet Airways, Godrej Professionals, Pfizer, Mahindra Group, Publicis Worldwide, and many others. His ability to simplify complex marketing concepts, combined with his engaging teaching style, has earned him widespread admiration from students and professionals alike.

Aditya has spearheaded IIDE’s B2B growth, forging partnerships with over 40 higher education institutions across India to upskill students in digital marketing and business skills. As a visiting faculty member at top institutions like IIT Bhilai, Mithibai College, Amity University, and SRCC, he continues to influence the next generation of marketers.

Apart from his marketing expertise, Aditya is also a spiritual speaker, often traveling internationally to share insights on spirituality. His unique blend of digital marketing proficiency and spiritual wisdom makes him a highly respected figure in both fields.