Students Centric

Placements Report

Trackable results, real numbers

Reviews

Proven success, real voices

Trainers

Expert-led, Industry-Driven Training

Life at IIDE

Vibrant Spirit student life

Alumni

Successful Journeys, Inspiring Stories

Learning Centre

Webinars

Blogs

Case studies

Live, Interactive Masterclasses

Fresh Insights, quick reads

Real-life, Industry relevant

More

Hire from us

Hire Top Digital Marketing Talent

Work with us

Join Our Team, Make an Impact

Customised Training

Personalised digital marketing training for your company

Refer & earn

Simple, easy rewards

Contact us

Get the answers you need

About us

Know more about IIDE

Explore all course options

FOR FRESH GRADUATES

Post Graduation Program in Digital Marketing & Business Strategy- Ideal for Age: 20–25 Years

Can’t decide? Explore all our

Digital Marketing CoursesCOMPARE ALL 3 PROGRAMSOnline & Offline

Explore Top AI CoursesIndustry-Aligned TRACKMost Popular

UG Program in Digital Business & Entrepreneurship- Ideal for 12th Pass out / FY Degree Student

PARTNER PROGRAMS

Can’t decide? Explore all

BBA In Digital Marketing Colleges

Orginally Written by Aditya Shastri

Updated on Jun 10, 2026

Share on:

About Zomato

From a canteen notice board in Delhi to India's most-watched tech conglomerate. This is the Zomato story.

In 2008, Deepinder Goyal and Pankaj Chaddah were sitting at Bain & Company in Delhi, frustrated that nobody could find restaurant menus easily. So they scanned them, put them online, and called it Foodiebay.

By 2010, it had a new name, Zomato and a mandate to go much further. The pivot to food delivery came post 2015, COVID-19 accelerated everything, and by FY2022–23, the platform was clocking over 450 million annual orders. The side project had become an institution.

Then, in February 2025, it went even further. The parent company was renamed Eternal Limited, a signal that Zomato was now the flagship of a full commerce ecosystem.

Four businesses now sit under one roof:

- Zomato - Food delivery and dining-out, the original core, still the largest revenue driver.

- Blinkit - Quick commerce, delivering groceries and essentials in under 10 minutes.

- Hyperpure - A B2B supply arm providing fresh, quality ingredients directly to restaurants.

- District - A going-out platform for live events, concerts, and experiences.

Zomato (Eternal): Key Stats at a Glance

Before we dissect the SWOT, it helps to stand back and see the full picture. Numbers have a way of cutting through noise, so here's exactly where Zomato stands today.

| Metric | Details |

|---|---|

| Founded | 2008 (as Foodiebay) |

| Headquarters | Gurugram, Haryana, India |

| Founders | Deepinder Goyal, Pankaj Chaddah & co-founders |

| Parent Company | Eternal Limited (rebranded Feb 2025) |

| Stock Ticker | NSE: ETERNAL | BSE: 543320 |

| Market Cap (May 2026) | ₹2,37,225 Crore ($28 Billion USD) |

| FY26 Revenue | ₹54,364 Crore (+168% YoY) |

| FY26 Net Profit | ₹366 Crore |

| Q4 FY26 Net Profit Growth | 346% YoY - ₹174 Crore |

| Total Funding Raised | $1.66 Billion (18 rounds, 52 investors) |

| Key Investors | Info Edge · Ant Group · Peak XV Partners |

| Active Delivery Partners | 4.8 Lakh+ monthly |

| Cities Served | 800+ cities across India |

| Dark Stores (Blinkit) | 2,000+ |

| Business Verticals | Zomato · Blinkit · Hyperpure · District |

| Current Group CEO | Albinder Singh Dhindsa (from Feb 2026) |

| 52-Week Share Range | ₹212.60 - ₹368.45 |

Why Does Zomato Need a SWOT Analysis?

Fair question, Zomato is profitable on an adjusted basis, growing revenues at 168% year-on-year, and commanding a market cap of ₹2.37 lakh crore. On paper, everything looks fine. But here's the thing about companies that move this fast: speed hides friction.

Rapid growth can mask inefficiencies, overstated strengths, and risks that haven't fully surfaced yet. A SWOT framework forces a slowdown and four honest questions:

- What is Zomato genuinely good at?

- Where is it still vulnerable?

- What opportunities can it capture?

- What could derail the story?

For a company operating across four verticals, managing 4.8 lakh delivery partners, and facing a tightening regulatory environment around 10-minute deliveries, with Swiggy fighting back hard, these aren't academic questions. A SWOT analysis doesn't just describe where Zomato is. It reveals whether where it's heading actually makes sense.

Learn Digital Marketing for FREE

SWOT Analysis of Zomato

SWOT Analysis is an abbreviation for Strengths, Weaknesses, Opportunities, and Threats. This study focuses on the internal and external elements that might affect every company. Internal variables include strengths and weaknesses, whereas external ones include opportunities and threats.

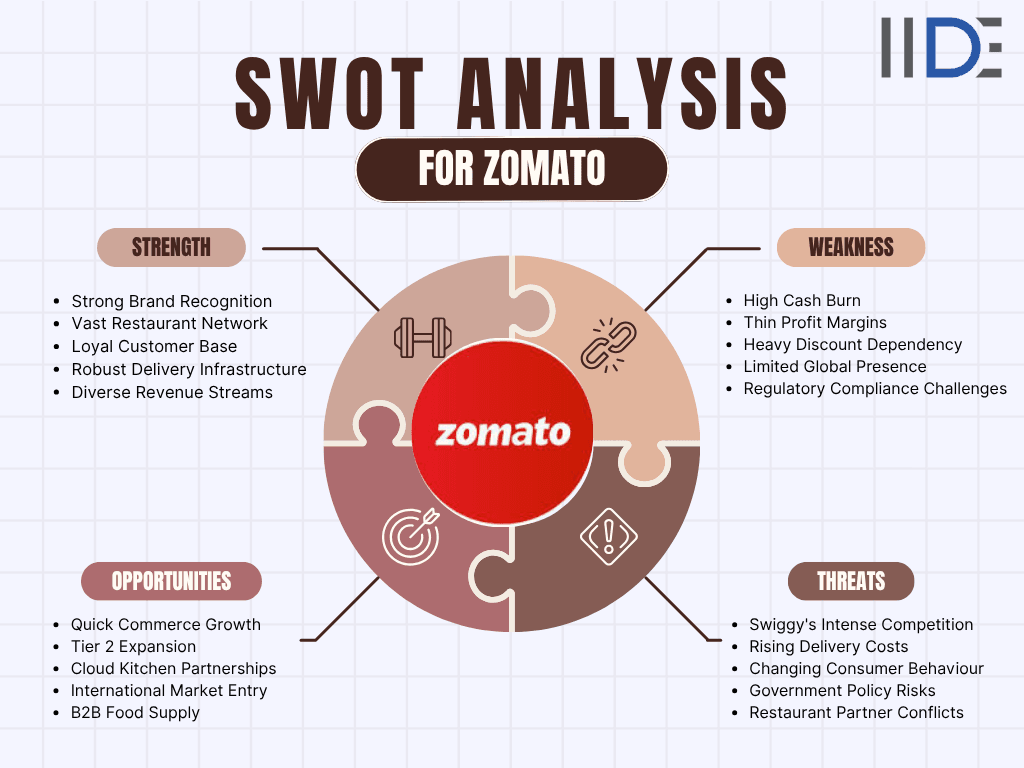

1. Strengths of Zomato - What Zomato Gets Genuinely Right

Zomato has spent years building advantages that are hard to copy and harder to dislodge. Here's what's genuinely working in its favour in 2026.

- Market Dominance That's Actually Earned - Zomato holds 57% of India's food delivery gross order value and ranked 21st on Kantar BrandZ 2025 with a $6B brand value up 69% YoY. Swiggy grew just 4% in the same period. That gap is not accidental.

- A Multi-Vertical Ecosystem That Creates Lock-In - Zomato isn't just a food app, it's food (Zomato), groceries (Blinkit), restaurant supplies (Hyperpure), and live events (District). Users embedded across verticals don't just order, they stay.

- Blinkit The Rocket Inside the Company - It hit EBITDA breakeven in Q3 FY26, commands 50%+ of India's quick commerce market, and runs 2,200+ dark stores. In a market projected to reach $12.97B by 2029, Blinkit is Eternal's biggest growth engine.

- Data and AI as a Competitive Weapon - Zomato targets 900,000+ keywords, uses AI-driven dynamic pricing and personalised recommendations across millions of daily transactions. That data depth takes years to build, and competitors simply don't have it.

- A Marketing Voice No One Can Copy - Zomato's brand doesn't feel corporate; it feels like a friend texting you. That tone, built over years across social media and campaigns, creates emotional loyalty that no budget can manufacture overnight.

2. Weaknesses of Zomato - Where the Cracks Are Showing

No company at this scale is without its pressure points. These are the cracks in Zomato's story that competitors will try to exploit.

- Profitability Is Still a Work in Progress -Revenue grew 168% in FY26, but net profit fell 30% to ₹366 crore. Heavy investment in expansion is the reason, but at a P/E of ~988, there's very little room for execution mistakes.

- Heavy India Dependence - Almost all of Eternal's revenue comes from one country. A domestic economic shock, food inflation spike, or regulatory blow hits with nothing to cushion the fall.

- Heavy Discount Dependency - Much of Zomato's user base was acquired and retained through deals. When a rival offers a deeper discount, that loyalty disappears fast. 1,200 restaurant partners once threatened to exit over aggressive discounting.

- Cheap growth has a price. Delivery Partner Cost Risk - 4.8 lakh gig workers power every delivery. Payouts rose by ~58% in one quarter. If regulators mandate formal benefits for gig workers, Zomato's cost structure changes overnight.

- Regulatory and Antitrust Headwinds - CCI found Zomato violated competition laws in 2024. A pending ₹803 crore GST notice adds to the pressure. The legal calendar is getting crowded and distracting.

- Operational Consistency at Scale - 800+ cities, millions of daily orders, 2,000+ dark stores and one viral food safety complaint can undo months of goodwill. FSSAI is already watching Blinkit closely.

Zomato isn't just a food app; it runs four businesses under one parent company. If you want to understand how each vertical actually generates revenue, our deep dive into the business model of Zomato breaks down exactly how the money flows from restaurant to customer.

3. Opportunities for Zomato - The Runway Ahead and Its Long

3. Opportunities for Zomato - The Runway Ahead and Its Long

India's food and quick commerce market is still in its early innings. The opportunity space in front of Zomato in 2026 is genuinely compelling if it executes well.

- Tier 2 & Tier 3 India The Next 500 Million-Cheap data and smartphones are pulling smaller-city India online fast. Blinkit is already in Kochi, Haridwar, Vijayawada, and there are hundreds more cities to go. The demand is there. The infrastructure just needs to catch up.

- Quick Commerce Is Still Exploding-India's quick commerce market hit ₹64,000 crore in FY25, doubling in one year and is headed to $12.97B by 2029. Blinkit leads with 50%+ share. The runway ahead is longer than most people realise.

- District The Going-Out Economy Is Barely Tapped-India's live events market is projected at ₹14,700 crore. District already has a $500M+ annualised GOV run-rate. Every Zomato Gold member is a potential District user; the cross-sell is sitting right there.

- Cloud Kitchen Partnerships-Delivery-only kitchens need a platform. Zomato needs exclusive, margin-friendly inventory. Deeper cloud kitchen partnerships solve both, especially in high-demand zones where traditional restaurants are scarce.

- International Market Entry- Southeast Asia, the Middle East, parts of Africa, growing urban populations, low food delivery penetration, and underdeveloped infrastructure. These are exactly the conditions Zomato cracked in India. The playbook already exists.

- Hyperpure The B2B Flywheel - It nearly doubled revenue YoY and is approaching profitability. The more restaurants depend on it for supplies, the tighter Zomato's grip on the entire food ecosystem from kitchen to customer.

- AI and Deeper Personalisation - Millions of daily transactions = unmatched behavioural data. Predictive reordering, smarter recommendations, and dynamic pricing, Zomato's AI edge widens every day. New entrants simply cannot replicate this overnight.

Threats to Zomato- What Could Actually Derail the Story

Threats aren't hypothetical for Zomato; several of them are actively playing out right now. This is where the SWOT gets uncomfortable, and also where it's most useful.

- Competition That's Well-Funded and Getting Sharper - Swiggy raised $1.3B in its 2024 IPO. Zepto is scaling fast. Amazon Fresh is pushing sub-30-minute delivery. Flipkart Minutes has just entered. Every new player forces more spending and thinner margins.

- Regulatory Pressure Is Escalating Fast - Government crackdown on 10-minute delivery claims (Jan 2026), FSSAI tightening hygiene norms, an unresolved CCI ruling, and a live ₹803 crore GST dispute. The regulatory heat is on and rising.

- Consumer Spending Sensitivity - Food delivery is a discretionary spend, the first cut when budgets tighten. Late 2025 already showed 'subdued demand' signals. Food inflation doesn't help. One bad macro quarter can dent order volumes sharply.

- Restaurant Partner Conflicts - 1,200 restaurants once threatened to leave over aggressive commission and discounting practices. CCI flagged Zomato's exclusivity contracts in 2024. Partners who feel squeezed will build their own ordering channels or leave.

- Cybersecurity and Data Risk - A past breach exposed 17 million user records. As Zomato expands into groceries, events, and financial services, the data footprint and the risk only grow larger. One serious breach could shatter user trust.

- Premium Valuation, High Expectations - At a $29B valuation and P/E near 988, Zomato has no room for disappointment. Any slowdown in Blinkit's growth or a regulatory shock could trigger a sharp and swift correction.

Zomato's brand doesn't feel corporate; it feels like a friend texting you. That tone is no accident. Zomato's digital marketing strategy is one of the most studied in Indian consumer tech, and for good reason.

Conclusion

In conclusion, has evolved from a restaurant discovery platform into a diversified commerce ecosystem under Eternal Limited, driven by strong brand value, market leadership, and rapid expansion across food delivery, quick commerce, B2B supplies, and live experiences.

While its strengths lie in its multi-vertical ecosystem, Blinkit’s explosive growth, AI-driven operations, and strong customer engagement, the company still faces key challenges such as profitability pressure, regulatory scrutiny, heavy discount dependency, and rising delivery costs. At the same time, opportunities in Tier 2 and Tier 3 markets, quick commerce, AI personalisation, and international expansion provide significant long-term growth potential.

However, intense competition, cybersecurity risks, and changing consumer spending behaviour remain major threats that could impact future performance. Overall, Zomato’s future success will depend on how effectively it balances aggressive growth with operational efficiency, profitability, and regulatory compliance.

Want to Know Why 2,50,000+ Students Trust Us?

Dive into the numbers that make us the #1 choice for career success

MBA - Level

Post Graduate in Digital Marketing & Business Strategy

Best For

Fresh Graduates

Mode of Learning

On Campus (Mumbai & Delhi)

Starts from

Jul 31, 2026

Duration

11 Months

Live & Online

Advanced Online Digital Marketing Course

Best For

Working Professionals

Mode of Learning

Online

Starts from

Aug 7, 2026

Duration

4-6 Months

Online

Professional Certification in AI Strategy

Best For

AI Enthusiasts

Mode of Learning

Online

Starts from

Sep 8, 2026

Duration

5 Months

On Campus

Advanced Certification in Artificial Intelligence

Best For

AI Enthusiasts

Mode of Learning

On Campus (Mumbai)

Starts from

Aug 31, 2026

Duration

3 Months

Online or Offline

Top AI Courses to Make You Future Ready!

Best For

AI Enthusiasts

Mode of Learning

2–5 Month Program

Starts from

Sep 8, 2026

Duration

Flexiable

Offline

Undergraduate Program in Digital Business & Entrepreneurship

Best For

12th Passouts

Mode of Learning

On Campus (Mumbai)

Starts from

Aug 19, 2026

Duration

3 Years

Offline

Degree In 2026 ≠ Enough Degree + Digital Skills = Future-Ready

Best For

12th Passouts

Mode of Learning

At IIDE Campus

Starts from

Aug 6, 2026

Duration

3 Years

Recent Post

You May Also Like

Eternal Limited is the parent company of Zomato, rebranded in February 2025. It operates four businesses Zomato (food delivery), Blinkit (quick commerce), Hyperpure (B2B restaurant supply), and District (live events). The Zomato app name remains unchanged.

Zomato holds approximately 57% of India's food delivery gross order value, making it the market leader ahead of Swiggy. In quick commerce, its subsidiary Blinkit commands over 50% market share.

Zomato was founded in 2008 by Deepinder Goyal and Pankaj Chaddah in Delhi. It was originally called Foodiebay before being renamed Zomato in 2010.

Zomato is profitable on an adjusted EBITDA basis. In FY26, it reported a net profit of ₹366 crore, though this was 30% lower than the previous year due to heavy investment in Blinkit expansion and new verticals. Q4 FY26 net profit grew 346% YoY to ₹174 crore.

Zomato's primary competitors are Swiggy (food delivery and quick commerce), Zepto (quick commerce), Amazon Fresh, and Flipkart Minutes. In the dining-out space, it competes with Dineout and EazyDiner.

Lead Trainer & Business Development Head at IIDE

Aditya Shastri leads the Business Development segment at IIDE and is a seasoned Content Marketing expert. With over a decade of experience, Aditya has trained more than 20,000 students and professionals in digital marketing, collaborating with prestigious institutions and corporations such as Jet Airways, Godrej Professionals, Pfizer, Mahindra Group, Publicis Worldwide, and many others. His ability to simplify complex marketing concepts, combined with his engaging teaching style, has earned him widespread admiration from students and professionals alike.

Aditya has spearheaded IIDE’s B2B growth, forging partnerships with over 40 higher education institutions across India to upskill students in digital marketing and business skills. As a visiting faculty member at top institutions like IIT Bhilai, Mithibai College, Amity University, and SRCC, he continues to influence the next generation of marketers.

Apart from his marketing expertise, Aditya is also a spiritual speaker, often traveling internationally to share insights on spirituality. His unique blend of digital marketing proficiency and spiritual wisdom makes him a highly respected figure in both fields.