Students Centric

Placements Report

Trackable results, real numbers

Reviews

Proven success, real voices

Trainers

Expert-led, Industry-Driven Training

Life at IIDE

Vibrant Spirit student life

Alumni

Successful Journeys, Inspiring Stories

Learning Centre

Webinars

Blogs

Case studies

Live, Interactive Masterclasses

Fresh Insights, quick reads

Real-life, Industry relevant

More

Hire from us

Hire Top Digital Marketing Talent

Work with us

Join Our Team, Make an Impact

Customised Training

Personalised digital marketing training for your company

Refer & earn

Simple, easy rewards

Contact us

Get the answers you need

About us

Know more about IIDE

Explore all course options

FOR FRESH GRADUATES

Post Graduation Program in Digital Marketing & Business Strategy- Ideal for Age: 20–25 Years

Can’t decide? Explore all our

Digital Marketing CoursesFOR STUDENTSOn-campus

Advanced Certification in AIFOR WORKING PROFESSIONALSOnline

Professional Certification in AI StrategyIndustry-Aligned TRACKMost Popular

UG Program in Digital Business & Entrepreneurship- Ideal for 12th Pass out / FY Degree Student

PARTNER PROGRAMS

Can’t decide? Explore all

BBA In Digital Marketing Colleges

Orginally Written by Aditya Shastri

Updated on Jul 4, 2026

Share on:

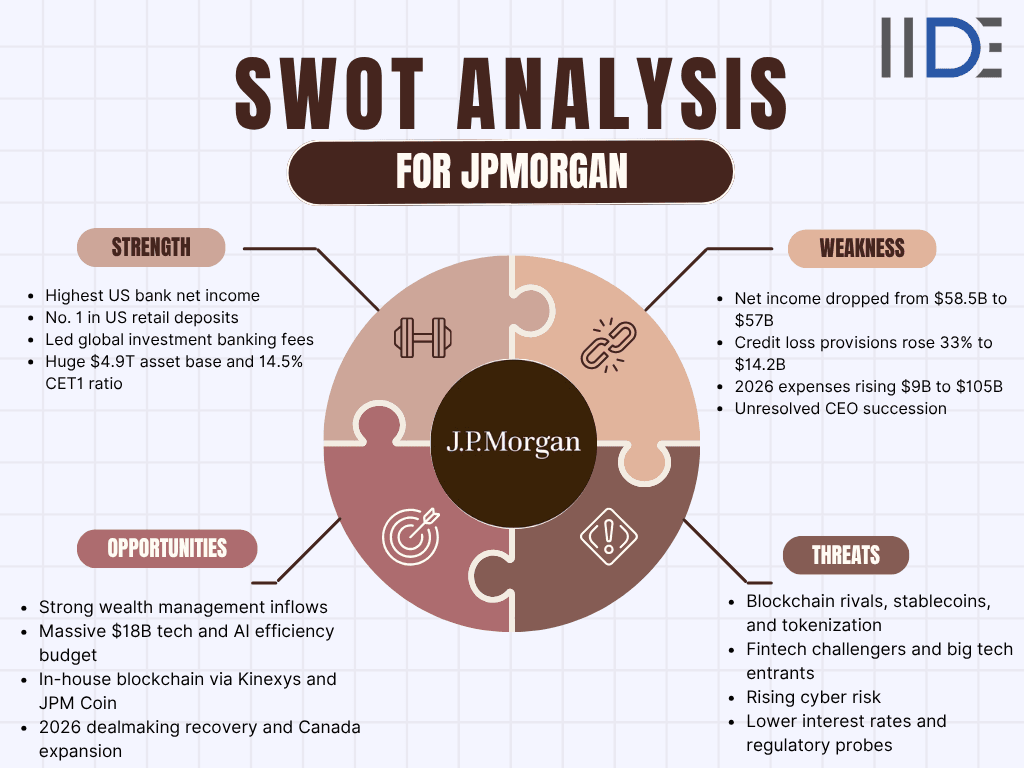

JPMorgan Chase's key strengths are its $57 billion annual profit, number one position in US retail deposits, and leadership in global investment banking fees. Its main weaknesses are rising credit costs and an unresolved CEO succession. The biggest opportunity lies in wealth management and AI, while blockchain-based competitors are its most pressing threat. Founded in 1799, it is the largest bank in the United States with 2025 revenue of $182.4 billion.

| SWOT ANALYSIS TABLE | |

|---|---|

| Strengths | Weaknesses |

|

$57 billion net income in 2025, the highest of any US bank (JPMorgan Chase Q4 2025 earnings release) |

Net income fell from a record $58.5 billion in 2024 to $57 billion in 2025 |

|

Number 1 in US retail deposits for 5 straight years, with $2.56 trillion in total deposits |

Credit loss provisions jumped 33% to $14.2 billion in 2025 |

|

Number 1 in global investment banking fees with an 8.4% share (Morningstar, 2026) |

2026 expense guidance of roughly $105 billion, up about $9 billion year on year |

|

$4.9 trillion in total assets and a 14.5% CET1 capital ratio |

CEO succession still unresolved; Jamie Dimon is 70 |

| Opportunities | Threats |

|

Wealth management momentum, with $52 billion in long-term net inflows in Q4 2025 alone |

Blockchain rivals: stablecoins, tokenisation, and smart contracts |

|

$18 billion annual technology budget powering AI-led efficiency |

Fintech challengers like Chime, SoFi, and Robinhood, plus big tech entrants |

|

Its own blockchain unit, Kinexys, JPM Coin, and the JPMD deposit token |

Cyber risk, which the bank itself calls its largest risk |

|

Dealmaking recovery in 2026 and expansion into Canada |

Falling interest rates are squeezing net interest income, plus regulatory probes |

Here's a quick visual snapshot of JPMorgan's SWOT Analysis:

Learn Digital Marketing for FREE

What Are the Strengths of JPMorgan Chase?

JPMorgan Chase's biggest strengths are its unmatched profitability, with $57 billion in 2025 net income, its number one rank in US retail deposits and global investment banking fees, a $4.9 trillion balance sheet, and one of the largest technology budgets in banking at around $18 billion a year.

1. Unmatched Profitability

- JPMorgan Chase is the most profitable bank in America, and it is not close.

- Net income of $57 billion in 2025 on revenue of $182.4 billion, more than any other US bank.

- Return on tangible common equity of 20% for the full year, roughly double what most large global banks manage.

- Nine consecutive years of revenue growth heading into 2026 show this is a trend and not a one-off.

2. Retail Deposit Leadership

- Chase is the number one retail deposit bank in the United States, and deposits are the cheapest funding a bank can get.

- Ranked first in US retail deposits for five consecutive years.

- Held $2.56 trillion in total deposits at the end of 2025, rising to $2.68 trillion by March 2026.

- Added over 400,000 net new checking accounts in a single quarter of 2025.

- Holds the number one retail deposit share in 22 of the top 125 US markets.

3. Investment Banking Dominance

- When companies anywhere in the world raise money or merge, J.P. Morgan is usually the first call.

- Number one globally in investment banking fees with an 8.4% market share in 2026.

- Ahead of Goldman Sachs, Morgan Stanley, and Bank of America on fee rankings.

- Also number one in Markets revenue and Treasury Services revenue, so the lead is across the investment bank, not just advisory.

4. Fortress Balance Sheet

- The bank's capital position gives it room to absorb shocks that would sink weaker rivals.

- $4.9 trillion in total assets and $364 billion in stockholders' equity as of March 2026.

- CET1 capital ratio of 14.5% against a regulatory requirement of 11.5%.

- Strong enough to raise the quarterly dividend to $1.65 per share and approve a $50 billion buyback in June 2026 at the same time.

5. Scale and Diversification

- JPMorgan earns from consumers, corporations, governments, and investors at once, so no single slowdown hurts it too much.

- Operations in over 60 countries with 318,512 employees at the end of 2025.

- More than 5,000 branches across the US, the widest network of any American bank.

- Over $7.1 trillion in client assets across wealth and asset management.

- More than 90% of Fortune 500 companies do business with the firm.

- Processes over $10 trillion in payments every day.

6. Technology Budget Advantage

- The firm spends more on technology in a year than most fintech challengers are worth in total.

- Annual technology spend of around $18 billion, among the highest of any bank globally.

- Management expects AI-driven efficiencies to support growth in 2026 as interest rate tailwinds fade.

- This spending gap is widening the divide between mega banks and smaller regional players who cannot keep up.

What Are the Weaknesses of JPMorgan Chase?

JPMorgan Chase's main weaknesses are a profit decline in 2025 after its record 2024, a 33% jump in credit loss provisions, a rising cost base with 2026 expenses guided near $105 billion, and an unresolved succession plan for its 70-year-old CEO Jamie Dimon.

1. Profit Decline in 2025

- For the first time in years, the profit line went down instead of up.

- Net income fell from a record $58.5 billion in 2024 to $57 billion in 2025.

- The dip is small in percentage terms, but it breaks a multi-year streak of record earnings.

- At this size, growing profit gets harder every year, and investors have started pricing in that ceiling.

2. Rising Credit Costs

- The bank is setting aside a lot more money for loans it expects to go bad.

- Provisions for credit losses rose to $14.2 billion in 2025 from $10.7 billion in 2024, a jump of about 33%.

- Card Services drove most of the increase through higher charge-offs and reserve builds.

- Card loan growth of 6 to 7% is forecast for 2026, so the card book that is producing the losses keeps growing too.

3. Growing Expense Base

- Costs are rising faster than revenue, which is the one trend no bank wants.

- 2026 expenses are guided to roughly $105 billion, an increase of about $9 billion year on year.

- The size of the jump drew sharp questions from analysts on the Q4 2025 earnings call.

- Q1 2026 expenses rose 14% year on year, faster than the 10% revenue growth in the same quarter.

4. Net Interest Income Pressure

- The rate environment that inflated bank profits from 2022 to 2024 is now working against it.

- Throughout 2025, lower rates and deposit margin compression dragged on net interest income excluding Markets.

- Interest income is still the largest revenue line, so small margin compression across trillions in assets costs billions.

- Consumer deposit growth is only expected to pick up in the second half of 2026.

5. CEO Succession Uncertainty

- Nobody knows who runs the bank after Jamie Dimon, or when the handover happens.

- Dimon is 70 and has led the bank since 2006, making him banking's biggest key-person risk.

- In June 2026, long-time successor candidate Marianne Lake retired after 25 years, and COO Jennifer Piepszak ruled herself out.

- Doug Petno and Troy Rohrbaugh were named co-presidents with $30 million retention awards each, but no timeline has been given.

- Dimon has suggested he could stay as long as three more years, extending the uncertainty.

6. Lumpy One-Off Charges

- Big strategic bets keep producing big upfront hits to quarterly earnings.

- A $2.2 billion credit reserve was booked in Q4 2025 for the forward purchase of the Apple Card portfolio.

- That single charge cut quarterly EPS from $5.23 to $4.63.

- Charges like these make quarterly results harder to predict, even when the underlying business is healthy.

Explore the IndusInd Bank SWOT analysis to uncover the key strengths and risks shaping this rising Indian banking leader.

What Are the Opportunities for JPMorgan Chase?

JPMorgan Chase's biggest opportunities lie in wealth management, where client money is flowing in at a record pace, AI-led efficiency from its $18 billion technology budget, its own blockchain products like JPM Coin and the JPMD deposit token, and a deal-making recovery expected through 2026.

1. Wealth Management Growth

- Fee income from managing money is steadier than lending income, and this is where the money is flowing.

- $52 billion in long-term net inflows in Q4 2025 alone.

- Over $7.1 trillion in client assets across wealth and asset management.

- 21 straight years of positive total client asset flows, a consistency no large rival matches.

- Asset and Wealth Management posted a pre-tax margin of 38% in Q4 2025.

2. AI-Led Efficiency

- With rate tailwinds fading, management has publicly pinned 2026 growth on AI.

- The plan for 2026 rests on balance sheet growth, record wealth inflows, and AI-driven efficiencies.

- Even a 2 to 3% efficiency gain on a cost base near $105 billion frees up billions in profit.

- The $18 billion technology budget gives it more room to experiment with AI than any competitor.

3. Blockchain and Tokenised Money

- Rather than waiting to be disrupted, JPMorgan is building the disruption itself.

- Its blockchain unit, Kinexys, runs JPM Coin and tokenised deposits for institutional clients.

- It has developed JPMD, a deposit token, and is in talks with other major banks on a joint stablecoin project.

- If tokenised money becomes the future of payments, the bank intends to own the rails.

4. Dealmaking Recovery

- M&A and IPO activity is picking up, and the number one fee earner captures the largest slice of every recovery.

- Investment banking fees dipped 5% in Q4 2025, partly because deal timing shifted into 2026.

- Q1 2026 revenue rose 10% to $50.5 billion on higher Markets revenue, asset management fees, and investment banking fees.

- The firm was involved in promoting the high-profile SpaceX IPO in June 2026.

5. International Expansion

- Growth outside the US reduces dependence on the American rate cycle.

- In 2026, the firm extended its $1.5 trillion, 10-year Security and Resiliency Initiative to Canada.

- Its Canadian franchise has nearly doubled revenue and grown headcount by a third in five years.

- The Canada playbook can be repeated in other developed markets where the firm is underrepresented.

6. Untapped US Markets

- Chase is the number one retail deposit bank in only 22 of the top 125 US markets, leaving over 100 where it is not.

- Branch expansion into under-penetrated cities is a proven playbook the bank has run for a decade.

- Each new market feeds low-cost deposits into the rest of the business.

What Are the Threats to JPMorgan Chase?

JPMorgan Chase's most pressing threats are blockchain-based competitors such as stablecoins and tokenised assets, fintech challengers like Chime and SoFi, cyber attacks that the bank itself ranks as its largest risk, falling interest rates squeezing margins, and mounting regulatory scrutiny.

1. Blockchain-Based Competitors

- The CEO himself has named this as the structural threat to watch.

- In his April 2026 shareholder letter, Jamie Dimon warned that a new class of competitors built on blockchain, including stablecoins and smart contracts, could change how payments, trading, and asset management fundamentally work.

- Near-instant tokenised settlement threatens fee income and even the deposits that fund the entire bank.

- Dimon has said the bank must move faster on its own blockchain efforts to keep up.

2. Stablecoin Regulation Gap

- The bank's leadership worries that crypto rivals may get to play by easier rules.

- CFO Jeremy Barnum warned in April 2026 that stablecoins could become regulatory arbitrage, offering bank-like products without bank-like rules.

- Dimon raised the same concern about a parallel banking system forming outside regulation on the Q4 2025 earnings call.

- If crypto firms can take deposits without capital requirements, the playing field tilts against regulated banks.

3. Fintech and Big Tech Rivals

- Digital-first challengers do not need to beat JPMorgan everywhere; taking young customers at the margin is enough.

- Chime, SoFi, and Robinhood target specific customer segments with lower fees and better app experiences.

- Big tech companies hold the deepest daily customer relationships of all and keep edging into payments.

- The bank has responded by charging fintechs new fees for access to customer banking data, which itself has become a point of public conflict.

4. Cyber Risk

- The bank has publicly identified cyber attacks as its single largest risk.

- A firm processing over $10 trillion in payments daily is the most valuable hacking target in finance.

- It spends heavily on protection, employs top security experts, and stays in constant contact with government agencies.

- One major breach would damage trust in a way no balance sheet can fix.

5. Falling Interest Rates

- The macro cycle has turned from tailwind to headwind.

- Lower rates compressed deposit margins throughout 2025.

- Further rate cuts would squeeze net interest income while also signalling weaker loan demand.

- A downturn would hit the bank twice, through thinner margins and higher credit losses at the same time.

6. Regulatory and Legal Pressure

- For a bank this size, regulation moves profit pools by billions, and legal headlines carry their own cost.

- Analysts have flagged possible caps on credit card APRs as a direct risk to the card business.

- In June 2026, the US Department of Justice was reported to be probing JPMorgan and Citigroup transactions tied to a business network linked to Iran's supreme leader.

- Capital rules on the Markets business remain a live debate, with the bank arguing they hurt its international competitiveness.

Explore the Karnataka Bank SWOT analysis to analyse the strengths and risks of its aggressive digital banking expansion.

About JPMorgan Chase

JPMorgan Chase & Co. is the largest bank in the United States, tracing its roots to 1799 in New York. Headquartered in New York City and led by Chairman and CEO Jamie Dimon since 2006, it operates across consumer banking, investment banking, commercial banking, payments, and asset and wealth management, serving customers in over 60 countries with $4.9 trillion in assets.

| Field | Detail |

|---|---|

| Company name | JPMorgan Chase & Co. (NYSE: JPM) |

| Founded |

1799 (oldest predecessor); current company formed in 2000, via the J.P. Morgan and Chase Manhattan merger |

| Headquarters | New York City, USA |

| Chairman & CEO | Jamie Dimon, CEO since 2006 |

| Co-Presidents |

Doug Petno and Troy Rohrbaugh, appointed June 2026 |

| Industry | Banking and financial services |

| Revenue | $182.4 billion in FY2025 |

| Net income | $57.0 billion in FY2025 |

| Total assets | $4.9 trillion as of March 2026 |

| Employees | 318,512 at the end of 2025 |

| Market cap | Around $890 billion as of July 2026 |

| Main competitors |

Bank of America, Citigroup, Wells Fargo, Goldman Sachs, Morgan Stanley |

What Is Happening With JPMorgan Chase in 2026?

In January 2026, the bank reported $57 billion in full-year profit and guided to higher spending of around $105 billion for 2026. In June 2026, it raised its quarterly dividend to $1.65 per share, approved a new $50 billion share buyback, and reshaped its leadership by naming Doug Petno and Troy Rohrbaugh co-presidents after Marianne Lake's retirement, the clearest signal yet on who might eventually succeed Jamie Dimon.

Meanwhile, the firm is pushing deeper into blockchain through Kinexys and JPM Coin, extending its $1.5 trillion Security and Resiliency Initiative to Canada, and preparing for its Q2 2026 results on 14 July 2026.

JPMorgan Chase Key Takeaways & Recommendations

JPMorgan Chase enters 2026 as the most profitable, best-capitalised bank in America, number one in retail deposits and investment banking fees. But profit dipped in 2025, credit costs jumped 33%, expenses are guided sharply higher, and the CEO question remains open.

The core tension: JPMorgan is a fortress being circled by faster, lighter attackers. Its scale is its moat, yet that same scale makes growth slow and margins sensitive to rates, while blockchain and fintech rivals get to build without legacy costs or, in some cases, legacy rules.

Future outlook: The near-term outlook is solid. Q1 2026 revenue rose 10%, dealmaking is recovering, and wealth inflows are at record levels. The bigger question is the five-year one - who leads the bank after Dimon, and whether tokenised finance strengthens or erodes its payments dominance.

Actionable recommendations:

- Resolve succession visibly, since a clear timeline would remove the single largest overhang on the stock.

- Keep converting the blockchain threat into products, scaling JPMD and Kinexys before non-bank stablecoins reach critical mass.

- Hold the line on expenses by making the promised AI efficiencies show up in the cost line, not just in press releases.

- Watch card credit closely, because the 33% jump in provisions is the earliest warning light on US consumer health.

- Push international growth, using the Canadian playbook to reduce dependence on the US rate cycle.

Final word: For students of business, JPMorgan Chase is the definitive case study in incumbency done right - dominate your market, out-invest everyone in technology, and buy or build your way into every threat before it matures. The 2026 chapter will test whether that playbook survives a leadership change and a new monetary technology at the same time.

Want to Know Why 2,50,000+ Students Trust Us?

Dive into the numbers that make us the #1 choice for career success

MBA - Level

Post Graduate in Digital Marketing & Business Strategy

Best For

Fresh Graduates

Mode of Learning

On Campus (Mumbai & Delhi)

Starts from

Jul 31, 2026

Duration

11 Months

Live & Online

Advanced Online Digital Marketing Course

Best For

Working Professionals

Mode of Learning

Online

Starts from

Aug 7, 2026

Duration

4-6 Months

Online

Professional Certification in AI Strategy

Best For

AI Enthusiasts

Mode of Learning

Online

Starts from

Jul 28, 2026

Duration

5 Months

On Campus

Advanced Certification in Artificial Intelligence

Best For

AI Enthusiasts

Mode of Learning

On Campus (Mumbai)

Starts from

Jul 27, 2026

Duration

3 Months

Online or Offline

Top AI Courses to Make You Future Ready!

Best For

AI Enthusiasts

Mode of Learning

2–5 Month Program

Starts from

Jul 28, 2026

Duration

Flexiable

Offline

Undergraduate Program in Digital Business & Entrepreneurship

Best For

12th Passouts

Mode of Learning

On Campus (Mumbai)

Starts from

Aug 1, 2026

Duration

3 Years

Offline

Undergraduate Program in Digital Business & Entrepreneurship

Best For

12th Passouts

Mode of Learning

On Campus (Mumbai)

Starts from

Aug 1, 2026

Duration

3 Years

Recent Post

Lead Trainer & Business Development Head at IIDE

Aditya Shastri leads the Business Development segment at IIDE and is a seasoned Content Marketing expert. With over a decade of experience, Aditya has trained more than 20,000 students and professionals in digital marketing, collaborating with prestigious institutions and corporations such as Jet Airways, Godrej Professionals, Pfizer, Mahindra Group, Publicis Worldwide, and many others. His ability to simplify complex marketing concepts, combined with his engaging teaching style, has earned him widespread admiration from students and professionals alike.

Aditya has spearheaded IIDE’s B2B growth, forging partnerships with over 40 higher education institutions across India to upskill students in digital marketing and business skills. As a visiting faculty member at top institutions like IIT Bhilai, Mithibai College, Amity University, and SRCC, he continues to influence the next generation of marketers.

Apart from his marketing expertise, Aditya is also a spiritual speaker, often traveling internationally to share insights on spirituality. His unique blend of digital marketing proficiency and spiritual wisdom makes him a highly respected figure in both fields.