Students Centric

Placements Report

Trackable results, real numbers

Reviews

Proven success, real voices

Trainers

Expert-led, Industry-Driven Training

Life at IIDE

Vibrant Spirit student life

Alumni

Successful Journeys, Inspiring Stories

Learning Centre

Webinars

Blogs

Case studies

Live, Interactive Masterclasses

Fresh Insights, quick reads

Real-life, Industry relevant

More

Hire from us

Hire Top Digital Marketing Talent

Work with us

Join Our Team, Make an Impact

Customised Training

Personalised digital marketing training for your company

Refer & earn

Simple, easy rewards

Contact us

Get the answers you need

About us

Know more about IIDE

Explore all course options

FOR FRESH GRADUATES

Post Graduation Program in Digital Marketing & Business Strategy- Ideal for Age: 20–25 Years

Can’t decide? Explore all our

Digital Marketing CoursesFOR STUDENTSOn-campus

Advanced Certification in AIFOR WORKING PROFESSIONALSOnline

Professional Certification in AI StrategyIndustry-Aligned TRACKMost Popular

UG Program in Digital Business & Entrepreneurship- Ideal for 12th Pass out / FY Degree Student

PARTNER PROGRAMS

Can’t decide? Explore all

BBA In Digital Marketing Colleges

Orginally Written by Aditya Shastri

Updated on Jun 22, 2026

Share on:

Amazon, founded in 1994 by Jeff Bezos, runs the world's largest e-commerce platform and cloud business. Its key strengths are AWS dominance and a $68.5 billion advertising business; its main weakness is razor-thin retail margins. The biggest opportunity is generative AI, while the FTC antitrust trial is its most pressing threat. Revenue: $717 billion (FY2025).

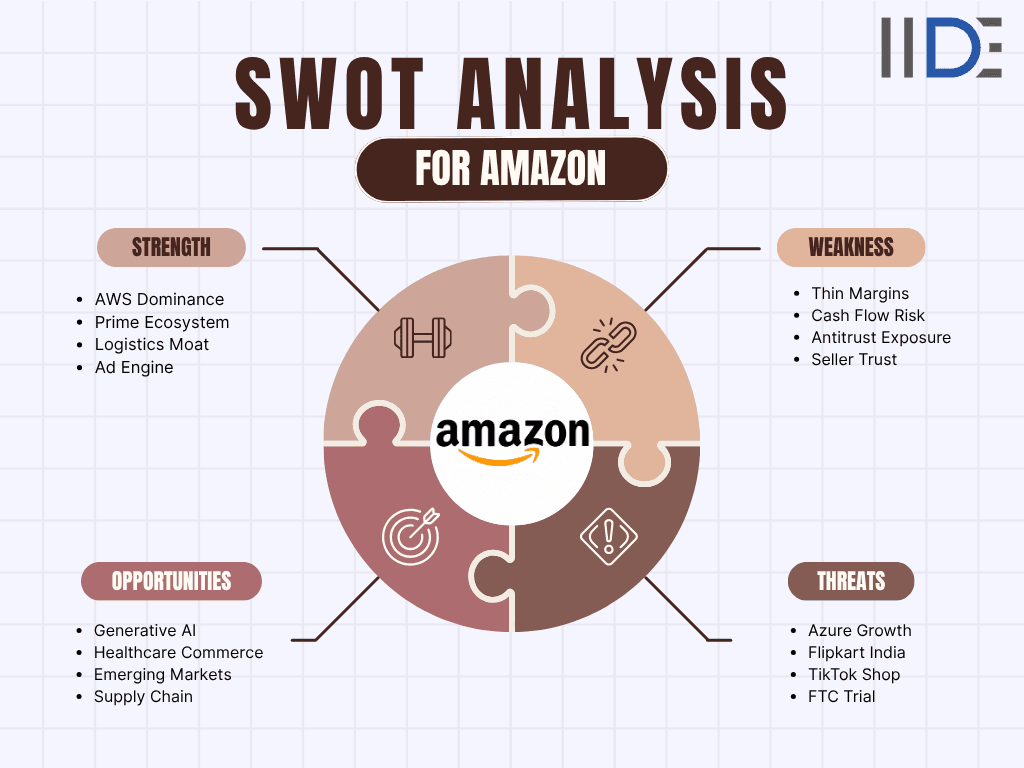

| SWOT TABLE | |

|---|---|

| STRENGTHS | WEAKNESSES |

| AWS: $128.7B revenue,19% cloud market share | Retail operating margins of just 1-3% |

| The ad business crossed $68.5B in FY2025 | Free cash flow dropped to $11B in FY2025 |

| 200M+ Prime members globally | FTC $2.5B settlement; EU DMA scrutiny |

| 30-year logistics moat; same-day delivery | Third-party seller trust issues |

| Proprietary AI: Bedrock, Trainium, Rufus | Overdependence is on AWS for profit |

| OPPORTUNITIES | THREATS |

| Generative AI driving AWS acceleration | Azure growing faster than AWS |

| Ad revenue still has massive runway | Temu & Shein are disrupting the price buyers |

| India & SE Asia e-commerce expansion | TikTok Shop bypassing the search model |

| Healthcare: $4.5T US market | 50% third-party sellers from China |

| Supply Chain by Amazon - B2B revenue | Consumer spending slowdown |

Here's a quick visual snapshot of Amazon's SWOT to make it easier to scan at a glance:

Learn Digital Marketing for FREE

What are the strengths of Amazon?

Amazon's strengths rest on three interlocking pillars: a cloud business that generates more profit than the entire retail operation, an advertising platform that benefits from purchase-intent data no social network can match, and a logistics network built over 30 years that would take any rival decades and hundreds of billions to replicate.

1. AWS The Profit Engine That Funds Everything

- AWS generated $128.73 billion in revenue in FY2025, growing 20% year-over-year. Its operating income for FY2025 stood at approximately $45.6 billion.

- This means AWS alone, which serves enterprises including Netflix, Adobe, and NASA, funds Amazon's retail expansion, AI investments, and logistics buildout.

Why it matters: Without AWS, Amazon's overall profitability collapses. It is the financial reason Amazon can afford to operate retail at near-zero margins and still invest billions in the future.

2. Advertising Third-Largest Platform in the World

- Amazon's ad revenue crossed $68.5 billion in FY2025, a 21.8% jump from $56.2 billion in FY2024. It now trails only Google and Meta in global digital advertising.

- Unlike social platforms where users scroll passively, Amazon's shoppers arrive actively, ready to buy, making every ad placement exponentially more valuable.

Why it matters: Ad revenue carries the highest margins in Amazon's business. It is growing faster than retail and is still in early innings relative to its full potential.

3. Prime The Retention Machine

- Amazon Prime has over 200 million global members, with approximately 185 million in the US alone. Subscription services generated $49.62 billion in revenue in FY2025, up 12% from 2024.

- Prime bundles shipping, video, music, pharmacy, and gaming. The longer members stay, the more embedded they become.

Why it matters: Prime members spend significantly more per year than non-members. It is Amazon's most powerful lock-in mechanism and its deepest loyalty driver.

4. Last-Mile Logistics A 30-Year Moat

- Amazon has built the most sophisticated consumer logistics network in history. In 2025, same-day delivery capacity in rural areas nearly doubled year-over-year.

- Amazon now completes more than 60% of its own deliveries in the US through its own fleet, a capability built over three decades that no rival can replicate quickly.

Why it matters: No competitor can match this network in any meaningful timeframe. Even Walmart's logistics, the closest alternative, still trails Amazon on delivery speed in most urban markets.

5. AI Infrastructure and Proprietary Chips

- Amazon committed record capital expenditure in 2025, dominated by AI infrastructure and its custom Trainium chip.

- AWS Bedrock gives enterprises access to multiple AI models through one platform, creating high switching costs for businesses already inside Amazon's ecosystem.

Why it matters: Proprietary AI chips reduce Amazon's dependence on Nvidia and lower inference costs for AWS customers, a structural cost advantage that compounds over time.

6. Revenue Scale and Diversification

- Amazon's total revenue reached $717 billion in FY2025, growing 12% year-over-year. Net profit hit $77.6 billion, more than double its 2023 figure.

- No other company simultaneously leads in e-commerce, cloud computing, digital advertising, and subscription streaming.

Why it matters: Diversification means no single regulatory action, competitor, or macro shock can bring Amazon down. The flywheel keeps spinning even when individual segments face pressure.

To understand how Amazon's biggest retail rival is building its own logistics empire, read our detailed breakdown of the Marketing Mix of Walmart.

What are the weaknesses of Amazon?

- Amazon's biggest structural weakness is that its most visible business, retail, operates on margins too thin to sustain itself.

- The company effectively runs a cloud and advertising firm that subsidises the world's largest online store.

- Add mounting regulatory exposure and a trust problem with its own sellers, and the cracks beneath the record numbers become harder to ignore.

1. Retail Margins Are Almost Non-Existent

- Amazon's North American e-commerce segment operates at margins that leave almost no buffer for external cost shocks.

- While North America's operating income reached $25 billion in FY2024, the bulk came from the high-margin advertising layer, not from selling goods.

- CEO Andy Jassy confirmed in the Q1 2025 earnings call that tariff pressures were already pushing up consumer prices.

Why it matters: If AWS or advertising revenue ever stumbled, Amazon's retail operation would bleed cash quickly. The entire profit architecture depends on the two divisions staying healthy.

2. Free Cash Flow Under Severe Pressure

- Despite record revenues, Amazon's free cash flow dropped to $11 billion in FY2025, down sharply from $38 billion in FY2024, driven by a $50.7 billion year-over-year increase in property and equipment purchases.

- The AI infrastructure bet is enormous, and returns are not yet visible on quarterly P&Ls.

Why it matters: Investors cannot yet see matching returns on Amazon's historic capex. This creates valuation pressure and limits flexibility if macro conditions worsen.

3. Regulatory and Legal Exposure

- Amazon settled the FTC antitrust case for $2.5 billion in Q3 2025, one of the largest retail regulatory settlements in US history.

- Parallel investigations under the EU Digital Markets Act continue, creating dual-jurisdiction compliance costs across Amazon's two most important markets.

Why it matters: Regulatory proceedings distract management, generate ongoing negative headlines, and could force structural changes to how Amazon operates its marketplace and logistics together.

4. Third-Party Seller Trust Is Eroding

- Over 700 sellers boycotted Amazon's ad system in 2024-25 over alleged payout delays and unauthorised deductions.

- Premium brands, including Nike and Birkenstock, have exited the platform entirely over brand dilution concerns.

Why it matters: Amazon's marketplace breadth depends on sellers trusting the platform. Losing premium sellers pushes high-value consumers toward DTC channels where Amazon has no presence.

5. Counterfeit Products and Fake Review Problem

- Manipulated reviews and fake product listings continue to surface in high-value categories on Amazon's marketplace.

- Despite repeated enforcement efforts, the scale of the platform makes comprehensive monitoring extremely difficult.

Why it matters: Consumer trust is the foundation of repeat purchase behaviour. Every counterfeit incident nudges a shopper slightly closer to buying directly from the brand's own site.

What are the opportunities for Amazon?

Amazon's biggest opportunities sit at the intersection of its existing infrastructure and the trends reshaping the next decade. Generative AI is accelerating enterprise cloud demand exactly where Amazon is strongest. Advertising still has enormous room to grow. And emerging markets, especially India, are creating a new wave of first-time online buyers that Amazon is well-positioned to capture.

1. Generative AI Is an AWS Tailwind

- Enterprise demand for AI compute is accelerating, and AWS is the platform most enterprises are already on.

- AWS revenue grew 20% year-over-year to $128.73 billion in FY2025, the fastest annual pace in several years.

- Amazon's $4 billion investment in Anthropic gives it a seat at the enterprise AI model layer, not just the infrastructure layer.

Why it matters: Every enterprise that builds AI on AWS deepens its dependency on Amazon's ecosystem. Switching costs increase every quarter, making AWS stickier as AI adoption grows.

2. Advertising Still Has a Massive Runway

- Amazon's ad business grew 21.8% to $68.5 billion in FY2025. But retail media globally is still a small fraction of total digital ad spend.

- Prime Video ads reached 315 million monthly active viewers in Q4 2025, adding a full-funnel dimension most retail media platforms cannot offer.

Why it matters: As advertisers demand provable ROI, Amazon's platform, where ads sit next to the buy button, becomes more valuable every year.

3. India and Southeast Asia E-Commerce Expansion

- India's e-commerce market is growing rapidly, fuelled by rising smartphone penetration and a fast-expanding middle class.

- Amazon is investing in regional language support, UPI payment integration, and Prime Video local content to close the gap on Flipkart, which currently holds approximately 48% of the Indian market.

Why it matters: Building market leadership in India now is far more valuable than competing for incremental share in already-saturated Western markets.

To see how Amazon's biggest competitor in India is approaching the same market, explore our in-depth look at the Marketing Strategy of Flipkart.

4. Healthcare Disruption

- Through Amazon Pharmacy, Amazon Clinic, and the One Medical acquisition, Amazon is assembling an integrated consumer healthcare offering in the $4.5 trillion US healthcare market.

- Its logistics network gives it a genuine edge in same-day prescription delivery that no traditional pharmacy chain can easily match.

Why it matters: If Amazon successfully bundles healthcare into Prime, it creates a retention layer that makes the subscription almost impossible to cancel.

5. Supply Chain by Amazon B2B Logistics Revenue

- Amazon is monetising its existing logistics infrastructure by offering fulfilment services to third-party businesses, competing directly with UPS and FedEx.

- This turns decades of sunk capital investment into a new commercial revenue stream with minimal additional build cost.

Why it matters: Amazon already owns the warehouses, the vans, and the software. Every B2B fulfilment contract it wins is almost pure incremental margin on assets already paid for.

What are the threats to Amazon?

Amazon's threats in 2026 are coming from multiple directions simultaneously, and several are targeting its most profitable segments. Azure is gaining cloud market share, Temu is rewriting price competition in retail, TikTok Shop is pulling younger buyers away from search-driven shopping, and the regulatory environment has never been more active in Amazon's three-decade history.

1. Microsoft Azure Is Closing the Cloud Gap

- AWS held approximately 30-31% global cloud market share through 2024, but Azure has been growing faster, powered by its OpenAI partnership and deep integration with Microsoft 365.

- Google Cloud is also gaining aggressively, making this a genuine three-way fight rather than AWS's solo race.

Why it matters: Cloud is Amazon's most profitable segment. Losing even a few percentage points of market share here has a disproportionate impact on overall profitability.

2. Temu and Shein Are Rewriting Price Expectations

- Temu and Shein are winning price-sensitive buyers with direct-from-factory pricing that Amazon's cost structure cannot easily match.

- These platforms are not trying to build a better Amazon; they are making cheap online shopping look entirely different.

Why it matters: These are precisely the categories where Amazon built its earliest loyal customer base. Losing price-sensitive buyers is a long-term threat to Prime's growth.

3. TikTok Shop Is Bypassing Amazon's Search Model

- TikTok Shop places purchase intent inside entertainment content, entirely bypassing Amazon's keyword search and buy model.

- If discovery-first shopping becomes the default behaviour for buyers under 30, Amazon risks losing a generation of consumers before they ever open the app.

Why it matters: Amazon's entire advertising model is built on capturing buyer intent at the search bar. If intent forms on TikTok before a buyer even searches, Amazon's ad network loses its most valuable moment.

4. Geopolitical Risk: China Seller Dependency

- Approximately 50% of Amazon's third-party marketplace sellers originate from China.

- A structural US-China trade decoupling would directly undermine the price competitiveness that makes Amazon's marketplace attractive to both buyers and sellers alike.

Why it matters: Amazon cannot quickly replace Chinese seller volume with alternatives from India, Vietnam, or Mexico. A forced transition would reduce product selection and push up prices simultaneously.

5. Consumer Spending Slowdown

- Tariff escalation in 2025 pushed up prices on thousands of consumer goods sold through Amazon.

- CEO Andy Jassy confirmed on the Q1 2025 earnings call that shoppers were already trading down and delaying non-essential purchases.

Why it matters: Amazon's retail business has almost no margin buffer. A consumer slowdown that would dent Walmart's profits would hit Amazon's retail P&L much harder.

To see how Amazon has built and evolved its commercial playbook over three decades, read our complete breakdown of the Marketing Strategy of Amazon.

About Amazon

Amazon.com, Inc. was founded by Jeff Bezos in 1994. Starting as an online bookstore, it quietly became the infrastructure layer the modern world depends on.

Retail, cloud computing, artificial intelligence, digital advertising, healthcare, and same-day logistics all operate under one roof, with each division strengthening the others.

The brand's guiding belief, "Work Hard. Have Fun. Make History," is not a tagline but a cultural contract, one that explains why Amazon consistently invests decades ahead of where returns are visible.

In 2026, Amazon committed a historic $200 billion in capital expenditure, the largest single-year infrastructure investment any company has ever made. That one number tells you everything about where the business is headed.

Quick stats of Amazon:

| Parameter | Details |

|---|---|

| Official Company Name | Amazon.com, Inc. |

| Founded | Tue Jul 05 1994 00:00:00 GMT+0530 (India Standard Time) |

| Founder | Jeff Bezos |

| Headquarters | Seattle, Washington, USA |

| CEO (2026) | Andy Jassy |

| Industries Served | E-commerce, Cloud Computing, Advertising, Streaming, Logistics, AI, Healthcare |

| Geographic Presence | 200+ countries and territories |

| Revenue (FY 2025) | $638 Billion |

| Net Income (FY 2025) | $59.2 Billion |

| Employees | 1.5 Million (worldwide) |

| Prime Members | 250+ million globally |

| Key Competitors | Walmart, Flipkart, Microsoft Azure, Google Cloud, Alibaba, Temu, TikTok Shop |

What's Happening with Amazon in 2026?

- Amazon settled its long-running FTC antitrust case in Q3 2025 for $2.5 billion, one of the largest regulatory settlements in US retail history.

- Parallel investigations remain active under the EU Digital Markets Act.

- AWS crossed $128 billion in annual revenue for FY2025, growing 20% year-over-year.

- Amazon's advertising business passed $68 billion for the first time, making it the world's third-largest digital ad platform behind only Google and Meta.

- Capital expenditure hit a record high in 2025, driven almost entirely by AI infrastructure and data centre expansion.

- Amazon's next decade is clearly being built on cloud and AI not retail.

Amazon's Key Takeaways & Conclusion

Amazon in 2026 is not just the world's largest online store; it is a cloud company, an advertising giant, and an AI infrastructure builder all running under one roof. AWS remains the real profit engine, generating $128.73 billion in FY2025, while advertising crossed $68.5 billion for the first time. Retail, despite its massive scale, still runs on margins too thin to survive without these two divisions holding it up.

The logistics moat is real and took 30 years to build. The regulatory exposure is equally real, as a $2.5 billion FTC settlement and active EU scrutiny are not small footnotes. Azure is closing the cloud gap, Temu is rewriting price expectations, and TikTok Shop is pulling the next generation of buyers away from search-driven shopping entirely.

What keeps Amazon formidable is the same thing that built its patience, long bets, and a flywheel that compounds every year. The AI infrastructure play underway today will likely look obvious in 2030, just like AWS did in 2006.

Recommendations:

- Diversify the seller base away from China dependency before geopolitical shifts force it

- Mandate third-party seller verification to fix marketplace quality and reduce regulatory risk

- Prioritise UPI-first checkout and regional language search to win India

- Bundle Amazon Pharmacy and One Medical into a Prime healthcare tier

- Scale Trainium aggressively to cut Nvidia dependence and lower AWS inference costs

Want to Know Why 2,50,000+ Students Trust Us?

Dive into the numbers that make us the #1 choice for career success

MBA - Level

Post Graduate in Digital Marketing & Business Strategy

Best For

Fresh Graduates

Mode of Learning

On Campus (Mumbai & Delhi)

Starts from

Jun 25, 2026

Duration

11 Months

Live & Online

Advanced Online Digital Marketing Course

Best For

Working Professionals

Mode of Learning

Online

Starts from

Jul 3, 2026

Duration

4-6 Months

Online

Professional Certification in AI Strategy

Best For

AI Enthusiasts

Mode of Learning

Online

Starts from

Jul 21, 2026

Duration

5 Months

On Campus

Advanced Certification in Artificial Intelligence

Best For

AI Enthusiasts

Mode of Learning

On Campus (Mumbai)

Starts from

Jul 20, 2026

Duration

3 Months

Offline

Undergraduate Program in Digital Business & Entrepreneurship

Best For

12th Passouts

Mode of Learning

On Campus (Mumbai)

Starts from

Aug 1, 2026

Duration

3 Years

Recent Post

You May Also Like

Amazon was founded in 1994 in Bellevue, Washington, USA by Jeff Bezos. He started the company as an online bookstore before expanding it into one of the world’s biggest technology and retail businesses.

Amazon's primary strengths include its AWS cloud dominance, a 250 million member Prime ecosystem, and a $60 billion advertising engine. Its proprietary logistics network also creates a massive competitive advantage.

Amazon operates on razor-thin retail margins of 1 to 3 percent, making it heavily dependent on cloud computing and ads for profit. The company also faces intense cash flow pressure from its $200 billion AI investments.

The most significant threats include the 2027 FTC antitrust trial and intense cloud competition from Microsoft Azure. Retailers like Temu and social platforms like TikTok Shop are also pulling younger shoppers away.

Amazon Web Services is the financial engine of the company, generating over $100 billion annually with high profit margins. This cloud revenue funds Amazon's retail expansion, logistics, and massive AI projects.

Amazon uses generative AI across its business, from the Rufus shopping assistant to enterprise cloud tools like Bedrock. It is also investing $25 billion in Anthropic to secure its position in enterprise AI infrastructure.

In global e-commerce, Amazon competes with Walmart, Temu, and Alibaba, while Flipkart is its biggest rival in India.

India is one of the fastest-growing digital economies with rising smartphone usage and millions of new online buyers. Amazon is investing heavily in local infrastructure and regional languages to compete with Flipkart.

Lead Trainer & Business Development Head at IIDE

Aditya Shastri leads the Business Development segment at IIDE and is a seasoned Content Marketing expert. With over a decade of experience, Aditya has trained more than 20,000 students and professionals in digital marketing, collaborating with prestigious institutions and corporations such as Jet Airways, Godrej Professionals, Pfizer, Mahindra Group, Publicis Worldwide, and many others. His ability to simplify complex marketing concepts, combined with his engaging teaching style, has earned him widespread admiration from students and professionals alike.

Aditya has spearheaded IIDE’s B2B growth, forging partnerships with over 40 higher education institutions across India to upskill students in digital marketing and business skills. As a visiting faculty member at top institutions like IIT Bhilai, Mithibai College, Amity University, and SRCC, he continues to influence the next generation of marketers.

Apart from his marketing expertise, Aditya is also a spiritual speaker, often traveling internationally to share insights on spirituality. His unique blend of digital marketing proficiency and spiritual wisdom makes him a highly respected figure in both fields.