Students Centric

Placements Report

Trackable results, real numbers

Reviews

Proven success, real voices

Trainers

Expert-led, Industry-Driven Training

Life at IIDE

Vibrant Spirit student life

Alumni

Successful Journeys, Inspiring Stories

Learning Centre

Webinars

Blogs

Case studies

Live, Interactive Masterclasses

Fresh Insights, quick reads

Real-life, Industry relevant

More

Hire from us

Hire Top Digital Marketing Talent

Work with us

Join Our Team, Make an Impact

Customised Training

Personalised digital marketing training for your company

Refer & earn

Simple, easy rewards

Contact us

Get the answers you need

About us

Know more about IIDE

Explore all course options

FOR FRESH GRADUATES

Post Graduation Program in Digital Marketing & Business Strategy- Ideal for Age: 20–25 Years

Can’t decide? Explore all our

Digital Marketing CoursesCOMPARE ALL 3 PROGRAMSOnline & Offline

Explore Top AI CoursesIndustry-Aligned TRACKMost Popular

UG Program in Digital Business & Entrepreneurship- Ideal for 12th Pass out / FY Degree Student

PARTNER PROGRAMS

Can’t decide? Explore all

BBA In Digital Marketing Colleges

Orginally Written by Aditya Shastri

Updated on Jul 7, 2026

Share on:

Jaypee Group's key strengths are its four-decade infrastructure legacy, engineering execution (Yamuna Expressway), and land assets; its main weaknesses are a ₹57,185 crore debt pile and a completed insolvency resolution that wiped out shareholders. Its biggest opportunities now lie in India's ongoing infrastructure boom and the residual value of assets like Jaypee Greens, while its key threats are the loss of independent identity, intense competition, and legal overhang from the insolvency process.

In 2026, its flagship, Jaiprakash Associates, was delisted after Adani Enterprises won a ₹14,535 crore NCLT-approved resolution plan, absorbing its cement, power, and real estate assets. Founded in 1979 by Jaiprakash Gaur, the group is now a case study in how ambitious leverage-driven growth ends in a corporate takeover.

Before diving into this SWOT Analysis of Jaypee Group, we'd like to acknowledge that the research and initial analysis for this article were conducted by Kripa Pokhrel, a student of IIDE's Online Digital Marketing Course, 2026 batch.

If you found this article useful, feel free to connect with Kripa on LinkedIn and share your appreciation for their research!

| SWOT ANALYSIS TABLE | |

|---|---|

| Strengths | Weaknesses |

| Four-decade infrastructure legacy and brand recall | ₹57,185 crore in admitted creditor claims led to insolvency |

| Proven large-scale execution (165-km Yamuna Expressway) | Flagship JAL delisted (June 18, 2026); shareholders wiped out |

| Diversified historical expertise (cement, power, real estate, hospitality) | Founder-level entity under ED investigation (PMLA, Nov 2025) |

| Valuable land bank in Noida/Greater Noida | Core assets are now absorbed into the Adani Group, not independently owned |

| Deep experience executing government infrastructure projects | High dependence on cyclical, capital-intensive sectors |

| Opportunities | Threats |

| India's infrastructure investment cycle (Gati Shakti, Bharatmala) | Loss of independent identity as assets transfer to Adani/Suraksha |

| Urbanisation demand for townships (Jaypee Greens brand) | Intense competition from L&T, Adani, Tata Projects, Shapoorji Pallonji |

| Residual brand equity in real estate (if retained post-transfer) | Ongoing homebuyer litigation and reputational overhang |

| PPP-style models for any surviving group entities (e.g., JPVL) | Regulatory, ED, and legal scrutiny extending resolution risk |

| Digital construction tech adoption industry-wide | Rising input costs and interest-rate sensitivity across the sector |

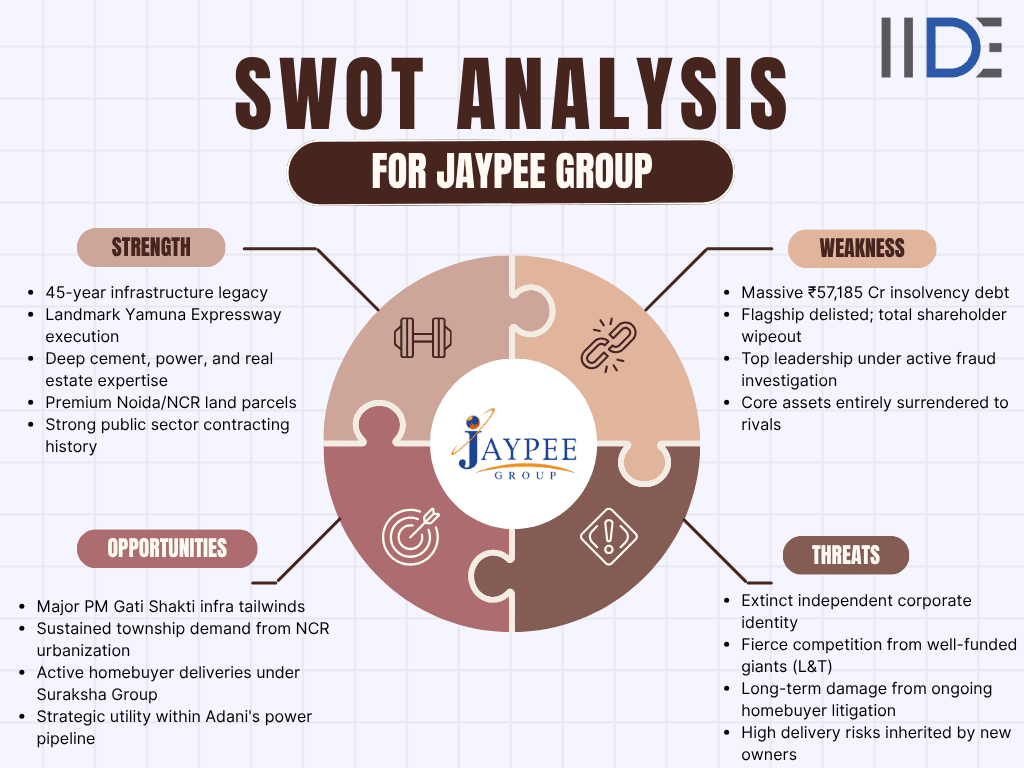

Here's a quick visual snapshot of Jaypee's SWOT Analysis:

Is Digital Marketing the Right Career for You?

Find out in a free 45-min masterclass · Career paths, roles and growth explained · By Karan Shah, Founder & CEO, IIDE

Is Digital Marketing the Right Career for You?

Find out in a free 45-min masterclass · Career paths, roles and growth explained · By Karan Shah, Founder & CEO, IIDE

What Are the Strengths of Jaypee Group?

Jaypee Group's core strength is its four-decade infrastructure legacy, built on large-scale execution capability and a recognisable brand among contractors and government bodies - even as its flagship entity has since gone through insolvency.

1. Four-Decade Infrastructure Legacy

- Founded in 1979, with over 45 years of executing large government-facing infrastructure and engineering projects.

- Operations spanned highways, power, and real estate across northern India.

- Long-standing recognition among contractors and government agencies.

- Institutional relationships with regulators were built up over decades.

- Brand recall that has outlasted the parent company's financial troubles.

2. Proven Large-Scale Execution

- The 165-km Yamuna Expressway remains one of India's notable expressway projects, connecting Greater Noida to Agra, one of India's longest access-controlled expressways at the time of construction.

- Anchored a broader township and real estate development (Jaypee Greens) along the corridor.

- Multiple hydropower projects executed across difficult terrain.

- Demonstrated capability in large, multi-year infrastructure builds, not just single contracts.

3. Diversified Historical Expertise

- Historically operated across cement, construction, real estate, hospitality, and power generation.

- Cement manufacturing at scale before divestment to UltraTech and later DCBL (Dalmia Cement).

- Power generation through Jaiprakash Power Ventures (2,200 MW, expandable to 4,000 MW).

- Real estate and township development in the Noida/Greater Noida corridor.

- Hospitality assets built alongside its infrastructure projects.

4. Valuable Land Bank

- Strategic land parcels in Noida and Greater Noida are developed through township projects, including Jaypee Greens.

- Land assets were a core part of the value that multiple bidders (Adani, Vedanta, Dalmia Bharat, Jindal Power, PNC Infratech) competed for.

- Includes the Jaypee International Sports City development.

- Positioned in one of India's fastest-growing NCR real estate corridors.

- Provides future monetisation potential regardless of which entity now controls it.

5. Government Project Experience

- Decades of coordinating with regulatory authorities on public infrastructure, building institutional knowledge of government contracting processes.

- Experience navigating environmental and land-acquisition approvals.

- Track record delivering public-facing infrastructure (expressways, power projects).

- Operational knowledge that transfers with the assets to new owners.

- A talent pool and project-execution team inherited by successor entities.

What Are the Weaknesses of Jaypee Group?

Jaypee Group's weaknesses centre on a debt burden that eventually forced its flagship company into insolvency, ending in a full shareholder wipeout and a takeover by Adani Enterprises in 2026.

1. Unsustainable Debt Load

- Jaiprakash Associates carried total admitted creditor claims of ₹57,185 crore, with outstanding borrowings disclosed at ₹55,357 crore as of January 14, 2026.

- RBI placed JAL on its list of 26 large loan defaulters as early as August 2017.

- Debt levels grew despite years of asset sales meant to reduce them.

- Interest coverage remained persistently weak through FY26.

- Debt ultimately exceeded what operating cash flows could service.

2. Formal Insolvency and Shareholder Wipeout

- JAL was admitted to the Corporate Insolvency Resolution Process (CIRP) on June 3, 2024, following an ICICI Bank petition.

- NCLT (Allahabad Bench) approved Adani Enterprises' ₹14,535 crore resolution plan on March 17, 2026.

- JAL was delisted from the BSE and NSE on June 18, 2026.

- 6.48 lakh shareholders, including 6.4 lakh retail investors, received zero consideration.

- Liquidation value was insufficient to cover even secured creditors' dues.

3. Founder-Level Legal Exposure

- Manoj Gaur, former Executive Chairman of JAL and former CMD of Jaypee Infratech, was arrested by the Enforcement Directorate under PMLA on November 13, 2025.

- The arrest relates to an alleged ₹14,599 crore homebuyer fraud.

- Adds leadership-level legal risk on top of the company's financial distress.

- Compounds reputational damage among homebuyers and investors.

- Signals scrutiny that may extend beyond the resolved insolvency case.

4. Loss of Independent Control Over Core Assets

- Under the approved resolution plan, control of nearly all core operating assets passes to Adani.

- Adani Enterprises takes over Jaypee Greens township projects and Jaypee International Sports City.

- Real estate, power, and hotel properties are included in the transferred portfolio.

- Adani Power separately acquires a ~24% stake in Jaiprakash Power Ventures.

- Adani Power also acquires the 180 MW Churk thermal power plant for ~₹1,200 crore.

5. High Dependence on Cyclical, Capital-Intensive Sectors

- The group's remaining businesses of power, real estate, and construction remain highly sensitive to interest rates and economic cycles.

- Jaiprakash Power Ventures posted a 97% YoY profit decline in Q3 FY26.

- Operating margins at JPVL contracted from 32.73% to 15.02% quarter-on-quarter.

- Revenue growth across group entities has stayed negative over the past five years.

- Earnings remain vulnerable to input-cost and rate cycles, independent of the JAL resolution.

Curious about another player in the infrastructure space? Check out our SWOT Analysis of Afcons Infrastructure.

What Are the Opportunities for Jaypee Group?

With its flagship absorbed into Adani, opportunities now mostly lie with whoever controls the underlying assets, though some residual value remains for the Jaypee brand and related entities.

1. India's Infrastructure Investment Cycle

- Government programmes continue to drive large-scale infrastructure spending, benefiting whoever now owns the underlying Jaypee-built assets.

- PM Gati Shakti and Bharatmala Pariyojana continue to channel investment into road and logistics infrastructure.

- The National Infrastructure Pipeline keeps demand high for the asset classes Jaypee built.

- Competing bids from Adani, Vedanta, Dalmia Bharat, Jindal Power, and PNC Infratech show this value was recognised in the market.

- The investment cycle is expected to continue over the next decade.

2. Urbanisation and the Jaypee Greens Brand

- Rapid NCR urbanisation continues to support demand for the townships the group built.

- The Jaypee Greens brand name may retain residual value under new ownership.

- Continued urban migration supports demand for residential and commercial development in Noida/Greater Noida.

- Brand equity in real estate can outlive a parent company's balance sheet.

- Execution and delivery continuity post-transfer will determine how much of this value is realised.

3. Homebuyer Delivery Progress Under Suraksha Group

- Jaypee Infratech (the Yamuna Expressway/Wishtown entity) was separately resolved to Suraksha Group in 2023-24.

- Suraksha Group is committed to completing stalled housing projects for ~20,000 pending buyers.

- By January 2026, ~6,000 homes had been delivered across 63 towers in Jaypee Wishtown.

- Continued delivery progress is the clearest sign that some Jaypee-originated projects can still create stakeholder value post-resolution.

- Sets a precedent for how the larger JAL assets might be handled under Adani.

4. Power Sector Consolidation Under Adani

- Jaiprakash Power Ventures' assets fit into Adani's broader power-capacity ambitions.

- JPVL's 2,200 MW capacity is expandable to 4,000 MW given available land.

- Fits Adani's stated plan to grow merchant power capacity by 20 GW by 2030.

- Shows the underlying assets carry genuine strategic value in India's power buildout.

- The opportunity now sits with the acquirer rather than the original promoter group.

5. Case-Study Value for the Broader Industry

- Technology-driven construction remains a broad industry opportunity for whichever entities inherit Jaypee's project pipeline and execution teams.

- AI-driven project monitoring and Building Information Modelling (BIM) adoption across the sector.

- Digital twins and IoT-enabled infrastructure monitoring are gaining traction industry-wide.

- Talent and process knowledge built over decades typically transfer with the assets.

- Position successor entities to modernise legacy project-delivery methods.

What Are the Threats to Jaypee Group?

The biggest threat facing Jaypee Group has already materialised - the loss of its flagship as an independent entity, alongside legal, competitive, and macroeconomic risks that continue to weigh on the group's remaining businesses.

1. Complete Loss of Independent Identity

- With JAL delisted and its core assets absorbed by Adani Enterprises and Adani Power, "Jaypee Group" as an independently listed, operating conglomerate effectively no longer exists in its original form.

- This is a completed outcome as of June 2026, not a forward-looking risk.

- The flagship entity's equity has been fully cancelled and extinguished.

- Only Jaiprakash Power Ventures remains separately listed.

- The Jaypee name may persist only as a brand within larger acquirers' portfolios.

2. Intense Competition for Any Remaining Operations

- Larger, better-capitalised rivals dominate the sector Jaypee once led.

- Larsen & Toubro, Tata Projects, and Shapoorji Pallonji all hold stronger balance sheets.

- Adani Group is now both a competitor and a direct acquirer of Jaypee assets.

- Any surviving or spun-off Jaypee-linked entity competes from a position of scale disadvantage.

- Access to capital markets remains constrained for smaller successor entities.

3. Ongoing Legal and Regulatory Overhang

- Legal exposure persists even after the NCLT resolution.

- The ED's PMLA case against Manoj Gaur remains active.

- Continued scrutiny from homebuyers over delayed project deliveries.

- Creditor recovery concerns given the ~76% haircut lenders are absorbing.

- Reputational risk can outlast a corporate restructuring and affect associated, still-listed brands (Jaypee Infratech, JPVL).

4. Execution Risk for New Owners

- Adani's ability to deliver stalled projects and pay remaining tranches will determine outcomes for stakeholders.

- A second payment of ₹6,026 crore is due around March 2028.

- ₹1,500 crore in NCDs backed by the Adani group guarantees is to be issued to secured creditors.

- If delivery falters under new ownership, reputational damage still attaches to Jaypee-origin projects in public memory.

- Homebuyers and creditors remain dependent on Adani's execution timeline.

5. Macro and Sector-Wide Cost Pressures

- Structural, sector-wide risks affect even well-capitalised successors as they integrate these assets.

- Rising cement, steel, and fuel costs continue to pressure margins.

- Interest-rate sensitivity affects any capital-intensive infrastructure or power business.

- Land acquisition and environmental compliance costs remain a persistent industry-wide friction.

- Demand cycles tied to broader economic growth affect project pipelines.

Don't miss our SWOT Analysis of Bharti Infratel for another deep dive into the infrastructure sector.

About Jaypee Group

Founded in 1979 by Jaiprakash Gaur, Jaypee Group built its reputation across engineering, construction, cement, power generation, real estate, and hospitality, operating through its flagship company, Jaiprakash Associates Limited (JAL), headquartered in Noida, Uttar Pradesh.

At its peak, it was among India's most prominent infrastructure conglomerates, known for the 165-km Yamuna Expressway and multiple hydropower projects. Following a debt crisis exceeding ₹57,000 crore, JAL entered insolvency in June 2024; its assets were acquired by Adani Enterprises under a ₹14,535 crore NCLT-approved resolution plan, and the company was delisted in June 2026.

| Particulars | Details |

|---|---|

| Official Name |

Jaypee Group (flagship: Jaiprakash Associates Limited) |

| Founder | Jaiprakash Gaur |

| Founded | 1979 (JAL incorporated 1995) |

| Headquarters | Noida, Uttar Pradesh, India |

| Industry | Infrastructure, Construction, Real Estate, Power |

| Core Businesses (historical) |

Engineering & construction, cement, real estate, power, hospitality |

| Total Admitted Creditor Claims | ₹57,185 crore (NCLT filing, 2024–26) |

| Q3 FY26 Revenue (JAL, consolidated) | ₹724.76 crore (quarter ended Dec 31, 2025) |

| Q3 FY26 Net Loss (JAL, consolidated) | ₹305.33 crore (quarter ended Dec 31, 2025) |

| Resolution Applicant |

Adani Enterprises Limited - ₹14,535 crore plan, NCLT-approved March 17, 2026 |

| Delisting Date | June 18, 2026 (BSE & NSE) |

| Major Competitors |

Larsen & Toubro, Adani Group, DLF, Tata Projects, Shapoorji Pallonji |

| Related Entities |

Jaypee Infratech (resolved to Suraksha Group, 2023-24), Jaiprakash Power Ventures (still listed) |

What's Happening With the Brand in 2026?

Jaypee Group's flagship, Jaiprakash Associates, moved through the final stages of its insolvency resolution over the course of 2026. On March 17, 2026, the NCLT's Allahabad Bench approved Adani Enterprises' ₹14,535 crore resolution plan for the company, ending a long-running Corporate Insolvency Resolution Process that began in June 2024.

Rival bidder Vedanta challenged the decision at the NCLAT, but the tribunal dismissed the appeal on May 4, 2026, clearing the way for Adani to proceed. In May 2026, Adani paid an initial ₹6,000 crore to lenders, while JAL sold its cement assets to Dalmia Cement for ₹2,850 crore.

The process concluded on June 18, 2026, when JAL was delisted from both the BSE and NSE, with around 6.48 lakh shareholders, including 6.4 lakh retail investors, receiving zero consideration for their holdings. Jaiprakash Power's Q3 FY26 profit plunged 97% YoY, while Suraksha Group has delivered ~6,000 of 20,000 delayed Jaypee Infratech homes.

IIDE Student Takeaway, Recommendations & Conclusion

This SWOT Analysis of Jaypee Group captures a story that has now reached its conclusion at the flagship level. Its four-decade legacy collapsed under aggressive debt, culminating in a 2026 insolvency, an Adani takeover, and a total shareholder wipeout.

Core Tension: Jaypee had great assets but poor financial discipline; aggressive leverage simply ended up feeding a better-capitalised competitor.

Recommendations:

- Cut debt before growing: Expanding fast on borrowed money without steady cash forces you to sell assets at a loss.

- Fix legal issues early: Trouble for top bosses shows that reputation damage and angry customers can outlive the financial crisis.

- Team up, don't go alone: Partnerships and joint ventures keep the whole company from crashing down on a single massive project.

- Be honest in a crisis: Homebuyers and small investors suffered the most because the company delayed sharing bad news.

- Deliver to rebuild trust: For Adani, finishing stalled projects is the only way to win back the public confidence that Jaypee lost.

Conclusion

Jaypee Group's story is, in many ways, a classic one in Indian business: a company built on genuine ambition and real engineering capability that ultimately could not outrun the debt it took on to fund its own growth. What began as a nation-building enterprise, shaping highways, townships, and power projects across northern India, ended up ceding control of those very assets to a larger, better-capitalised rival.

For students of business and marketing, the lesson isn't really about infrastructure or construction at all. It's about the gap between building something valuable and being able to hold on to it. Scale without financial discipline, however impressive in the short term, tends to catch up with a company eventually.

Jaypee Group's legacy will likely be remembered less for what it built and more for how its inability to manage debt ultimately decided who got to keep it.

Want to Know Why 2,50,000+ Students Trust Us?

Dive into the numbers that make us the #1 choice for career success

MBA - Level

Post Graduate in Digital Marketing & Business Strategy

Best For

Fresh Graduates

Mode of Learning

On Campus (Mumbai & Delhi)

Starts from

Oct 1, 2026

Duration

11 Months

Live & Online

Advanced Online Digital Marketing Course

Best For

Working Professionals

Mode of Learning

Online

Starts from

Aug 7, 2026

Duration

4-6 Months

Online

Professional Certification in AI Strategy

Best For

AI Enthusiasts

Mode of Learning

Online

Starts from

Sep 8, 2026

Duration

5 Months

On Campus

Advanced Certification in Artificial Intelligence

Best For

AI Enthusiasts

Mode of Learning

On Campus (Mumbai)

Starts from

Sep 1, 2026

Duration

3 Months

Online or Offline

Top AI Courses to Make You Future Ready!

Best For

AI Enthusiasts

Mode of Learning

2–5 Month Program

Starts from

Sep 8, 2026

Duration

Flexiable

Offline

Undergraduate Program in Digital Business & Entrepreneurship

Best For

12th Passouts

Mode of Learning

On Campus (Mumbai)

Starts from

Aug 19, 2026

Duration

3 Years

Offline

Degree In 2026 ≠ Enough Degree + Digital Skills = Future-Ready

Best For

12th Passouts

Mode of Learning

At IIDE Campus

Starts from

Aug 19, 2026

Duration

3 Years

Recent Post

Its four-decade infrastructure execution track record, most visibly the 165-km Yamuna Expressway.

An unsustainable debt load (₹57,185 crore in admitted claims) that forced its flagship Jaiprakash Associates, into insolvency and eventual delisting.

Its flagship company, Jaiprakash Associates, was delisted from the BSE and NSE on June 18, 2026, after NCLT approved Adani Enterprises' ₹14,535 crore resolution plan; existing shareholders received zero compensation.

Larsen & Toubro, Adani Group, DLF, Tata Projects, and Shapoorji Pallonji.

No - its flagship entity has been fully resolved through insolvency, with total creditor claims of ₹57,185 crore and a complete loss for equity shareholders.

Positive for the assets themselves under new ownership (Adani, Suraksha Group), given India's ongoing infrastructure investment cycle - but the "Jaypee Group" as an independent conglomerate no longer exists in its original form.

Lead Trainer & Business Development Head at IIDE

Aditya Shastri leads the Business Development segment at IIDE and is a seasoned Content Marketing expert. With over a decade of experience, Aditya has trained more than 20,000 students and professionals in digital marketing, collaborating with prestigious institutions and corporations such as Jet Airways, Godrej Professionals, Pfizer, Mahindra Group, Publicis Worldwide, and many others. His ability to simplify complex marketing concepts, combined with his engaging teaching style, has earned him widespread admiration from students and professionals alike.

Aditya has spearheaded IIDE’s B2B growth, forging partnerships with over 40 higher education institutions across India to upskill students in digital marketing and business skills. As a visiting faculty member at top institutions like IIT Bhilai, Mithibai College, Amity University, and SRCC, he continues to influence the next generation of marketers.

Apart from his marketing expertise, Aditya is also a spiritual speaker, often traveling internationally to share insights on spirituality. His unique blend of digital marketing proficiency and spiritual wisdom makes him a highly respected figure in both fields.