Students Centric

Placements Report

Trackable results, real numbers

Reviews

Proven success, real voices

Trainers

Expert-led, Industry-Driven Training

Life at IIDE

Vibrant Spirit student life

Alumni

Successful Journeys, Inspiring Stories

Learning Centre

Webinars

Blogs

Case studies

Live, Interactive Masterclasses

Fresh Insights, quick reads

Real-life, Industry relevant

More

Hire from us

Hire Top Digital Marketing Talent

Work with us

Join Our Team, Make an Impact

Customised Training

Personalised digital marketing training for your company

Refer & earn

Simple, easy rewards

Contact us

Get the answers you need

About us

Know more about IIDE

Explore all course options

FOR FRESH GRADUATES

Post Graduation Program in Digital Marketing & Business Strategy- Ideal for Age: 20–25 Years

Can’t decide? Explore all our

Digital Marketing CoursesCOMPARE ALL 3 PROGRAMSOnline & Offline

Explore Top AI CoursesIndustry-Aligned TRACKMost Popular

UG Program in Digital Business & Entrepreneurship- Ideal for 12th Pass out / FY Degree Student

PARTNER PROGRAMS

Can’t decide? Explore all

BBA In Digital Marketing Colleges

Orginally Written by Aditya Shastri

Updated on May 20, 2026

Share on:

Aditya Birla Group generates over $65 billion in annual revenue across 36+ countries, yet one of its most prominent businesses, Vodafone Idea, has been bleeding losses for years.

That contrast between imperial scale and operational vulnerability is exactly what makes studying this conglomerate so compelling in 2026.

UltraTech Cement is India's undisputed market leader. Hindalco is a global metals powerhouse. Aditya Birla Capital is riding India's financial inclusion wave. And yet, the group carries crushing telecom debt, battles Reliance and Tata on multiple fronts simultaneously, and is visibly playing catch-up in the digital economy, a space where hesitation is expensive.

This SWOT analysis of the Aditya Birla Group breaks down exactly what powers this conglomerate, where it is structurally exposed, and what the next decade could look like for one of India's most fascinating business empires.

If analysing conglomerates like this excites you, IIDE's Online Digital Marketing Courses are built to give you that exact strategic edge.

About Aditya Birla Group

The story begins in 1857, when Seth Shiv Narayan Birla laid the foundation of what would grow into a truly global enterprise.

Today, under Chairman Kumar Mangalam Birla, the group operates across 36+ countries, employs over 140,000 people, and generates annual revenues of approximately $65 billion.

It's tagline "Taking India to the World," is not marketing copy. It captures a deliberate, decades-long strategy of building Indian enterprise far beyond domestic borders, from textiles and cement to copper and fintech.

Quick Stats about Aditya Birla Group:

| Detail | Information |

|---|---|

| Founded | 1857 |

| Headquarters | Mumbai |

| Chairman | Kumar Mangalam Birla |

| Annual Revenue | ~$65 Billion (FY 2024–25) |

| Global Footprint | 36+ Countries |

| Workforce | 140,000+ Employees |

| Key Competitors | Reliance Industries, Tata Group, JSW Group, HDFC Group |

Why This SWOT Matters in 2026

India's business landscape has shifted dramatically. Legacy conglomerates no longer compete only against each other. They now face digital-first challengers, ESG-driven capital markets, and a generation of consumers whose expectations reset faster than any boardroom strategy cycle.

- Rival Ambition is Accelerating: Reliance has crossed $100 billion in revenue and Tata is pushing aggressively into EVs, semiconductors, and consumer tech, both moving deeper into Aditya Birla's core territory every year.

- Gen Z is Rewriting the Rules: Younger Indian consumers expect digital-first experiences and genuine sustainability values. Brands that fail to deliver on both will simply not make the consideration list.

- Digital Investment is Now Urgent: AI and automation are reshaping sectors from cement logistics to personal lending. Every year of delay widens the gap with rivals who are already ahead.

- Macro Pressures are Permanent: Rising raw material costs, stricter environmental compliance, and global supply chain disruptions are not passing headwinds. For a capital-intensive group like Aditya Birla, they are ongoing strategic realities.

Learn Digital Marketing for FREE

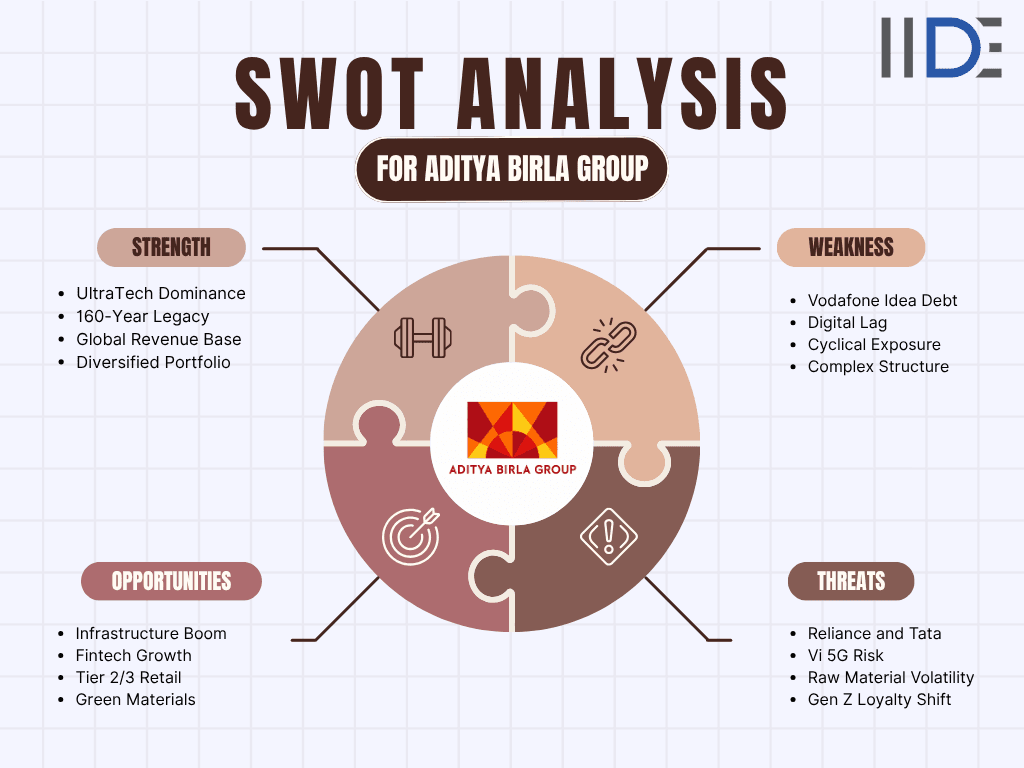

SWOT Analysis of Aditya Birla Group

Strengths of Aditya Birla Group

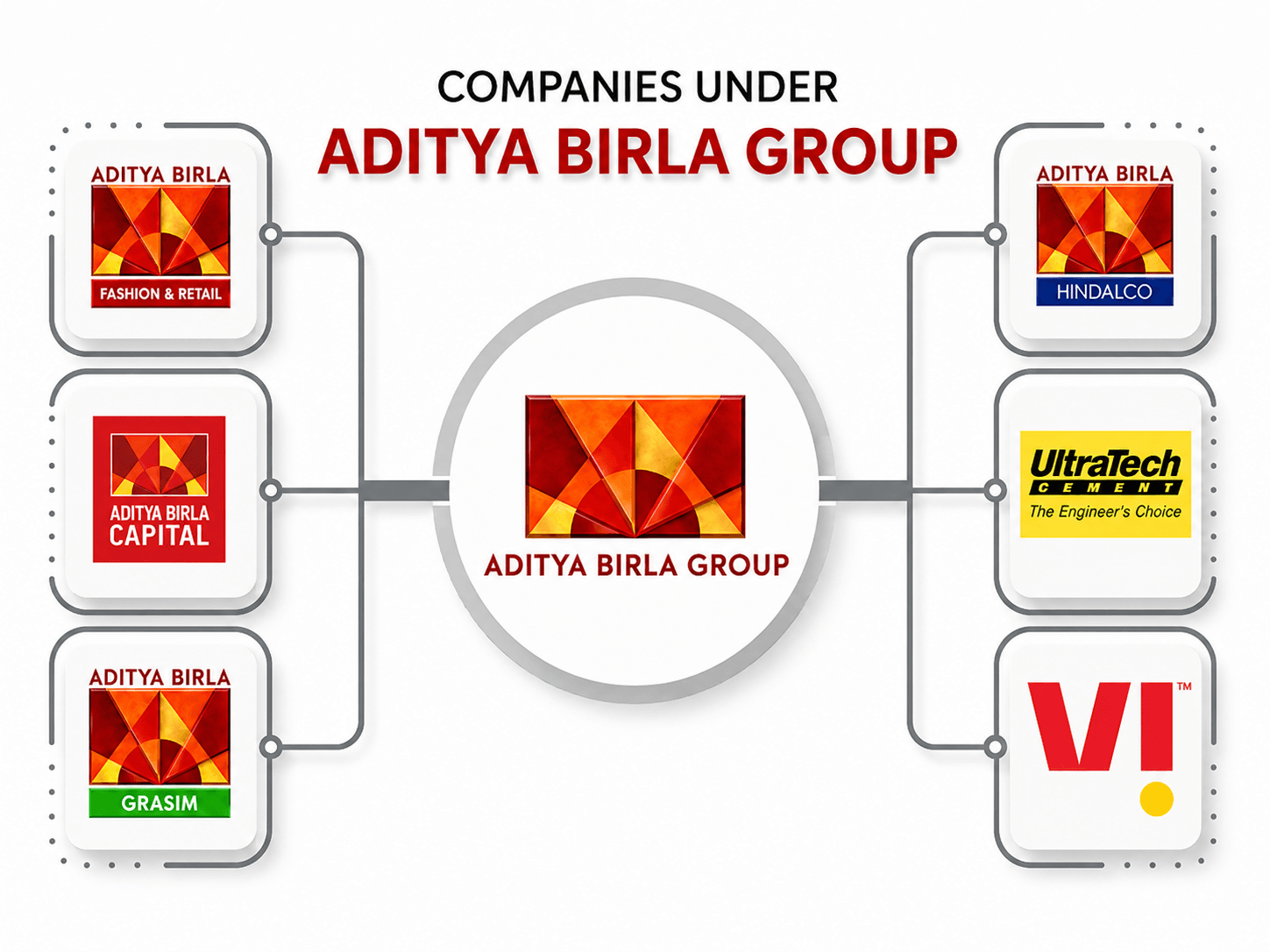

A Genuinely Diversified Business Portfolio:

- Very few Indian conglomerates match Aditya Birla's sector breadth. Cement, metals, telecom, financial services, fashion, and chemicals all operate on different economic cycles and serve different customer segments.

- When cement demand softens due to a construction slowdown, financial services or retail can compensate, and vice versa.

- This cross-sector revenue buffering is a structural competitive moat that focused, single-industry players simply cannot replicate.

UltraTech's Unrivalled Cement Dominance:

- UltraTech Cement is India's largest cement producer with installed capacity exceeding 150 million tonnes per annum (MTPA).

- With India's Union Budget allocating over Rs. 10 lakh crore to infrastructure covering highways, metro rail, affordable housing, and smart cities, UltraTech sits at the centre of the country's most consequential long-run growth story.

- No domestic competitor comes close to matching its logistics reach, brand equity, or production scale.

Nearly 50% Revenue from International Markets:

- Roughly half the group's revenue comes from operations across Asia, Africa, North America, and the Middle East.

- This global footprint insulates the group from overdependence on India's domestic cycle, opens exposure to faster-growing emerging markets, and meaningfully reduces currency concentration risk.

Over 160 Years of Brand Equity:

- A century and a half of operating history is an active business asset, not just a heritage story.

- The Aditya Birla brand carries deep credibility with consumers, institutional investors, government bodies, and international partners.

- Sub-brands like UltraTech, Pantaloons, and Aditya Birla Capital are household names that translate directly into pricing power, customer loyalty, and lower acquisition costs when entering adjacent markets.

Financial Scale to Fund Long-Horizon Bets:

- Generating approximately $65 billion annually gives the group capital reserves to weather downturns, fund acquisitions, and invest in green energy, fintech, and AI-driven operations.

- This financial firepower is a decisive advantage over mid-sized rivals forced to choose between sustaining operations and investing in transformation.

Early and Credible ESG Positioning:

- The group has committed to net-zero emissions by 2050, with UltraTech investing in alternative fuels, waste heat recovery, and low-carbon cement blends.

- As ESG criteria increasingly govern global institutional capital, this early positioning strengthens the group's appeal to international investors and premium buyers in sustainable construction.

Weaknesses of Aditya Birla Group

Vodafone Idea: A Live and Material Liability:

- Vi carries over Rs. 2 lakh crore in total debt, including statutory dues owed to the government.

- Despite repeated bailouts and management changes, it continues losing subscribers to Jio and Airtel at scale.

- Unlike Jio, which was built on 4G-native architecture, Vi inherited costly legacy infrastructure that has proven nearly impossible to rationalize.

- Beyond the financial drain, the crisis consumes management bandwidth and depresses investor confidence in the broader group.

If you want to go deeper on exactly where Vi stands today, the SWOT analysis of Vodafone Idea is worth a read the debt numbers alone tell a story that no boardroom presentation can sugarcoat.

Organizational Complexity That Slows Execution:

- Running 40+ business units across industries and geographies creates structural friction. Decision cycles lengthen, resource allocation becomes complicated, and strategic pivots take quarters to execute.

- In a competitive environment where digital-native rivals can act on market shifts in weeks, this inertia is a real and costly disadvantage.

Cyclical Revenue Concentration in Cement and Metals:

- Cement and metals are deeply tied to global economic conditions.

- When construction slows or commodity prices fall, margins in both segments compress simultaneously.

- The 2023-24 period demonstrated this clearly, as global demand softness pressured both UltraTech's realizations and Hindalco's metals margins at the same time.

Elevated Group-Level Debt:

- The capital intensity of cement and metals manufacturing means significant debt obligations exist even outside telecom.

- In a sustained high-interest-rate environment, debt servicing costs reduce financial flexibility and raise the hurdle rate for new investments, making bold strategic moves harder to justify at the board level.

A Visible Digital Gap vs. Reliance and Tata:

- Reliance Jio has redefined India's digital infrastructure. Tata Digital is building an ambitious super-app ecosystem through Tata Neu.

- Aditya Birla's digital initiatives, while growing, have not achieved comparable consumer mindshare, platform scale, or ecosystem stickiness.

- In a market expecting seamless digital experiences across banking, retail, and lifestyle services, this gap directly impacts customer acquisition and retention costs.

Opportunities of Aditya Birla Group

India's Multi-Year Infrastructure Boom:

- The government's sustained push across highways, metro rail, affordable housing, ports, and smart cities creates a structural demand tailwind for UltraTech Cement and Hindalco's aluminium division.

- With India targeting 50 smart cities and 11,000+ km of new highway corridors, elevated demand for cement and aluminium is projected to sustain for the next five to seven years.

The Fintech and Financial Inclusion Wave:

- Over 80% of Indians hold bank accounts, but formal credit penetration in rural and semi-urban India remains low.

- Aditya Birla Capital, managing over Rs. 4 lakh crore in AUM, is well-positioned to capture growth in mutual funds, digital insurance, and MSME lending.

- Gen Z consumers who prefer mobile-first financial products represent a particularly high-value acquisition opportunity.

Green Materials as a Premium Opportunity:

- Global demand for low-carbon construction materials and sustainable metals is accelerating, driven by regulatory mandates and institutional procurement preferences.

- UltraTech's low-carbon cement pilots and Hindalco's green aluminium investments give the group a genuine head start in a category that will command price premiums and attract ESG-aligned capital over the next decade.

Retail Growth in Tier 2 and Tier 3 India:

- India's apparel and retail market is projected to reach $350 billion by 2030, with most new growth coming from aspirational consumers in smaller cities.

- Aditya Birla Fashion and Retail Limited and Pantaloons can capture this wave through physical store expansion, direct-to-consumer digital channels, and brand collaborations that build loyalty among first-time fashion buyers.

AI-Driven Operational Efficiency:

- AI and predictive analytics offer deployable, near-term gains across cement, metals, and financial services. Predictive maintenance could reduce unplanned plant downtime by 15 to 20 percent.

- AI-driven credit scoring could expand Aditya Birla Capital's lending book with stronger risk calibration.

- These are not future possibilities.

Expansion in Africa and Southeast Asia:

- Africa and Southeast Asia are high-growth markets for building materials, where urbanisation and construction activity are accelerating sharply.

- The group already holds footholds in several of these markets.

- The opportunity lies in converting that presence into dominance through targeted acquisitions, local partnerships, and distribution investment before global competitors move in.

Threats of Aditya Birla Group

Relentless Competition from Reliance and Tata:

- This is the defining competitive reality for Aditya Birla in 2026.

- Reliance has surpassed $100 billion in revenue and is expanding aggressively into retail, green energy, media, and financial services.

- Tata Group is pushing into EVs, semiconductors, and consumer tech with renewed ambition.

- Both are well-capitalised and targeting the same consumers and institutional clients across multiple sectors simultaneously.

Tata's ambition runs deeper than most realise the SWOT analysis of Tata Group shows exactly why Aditya Birla cannot afford to underestimate them.

Vodafone Idea's Uncertain 5G Future:

- India's telecom market has consolidated into a near-duopoly between Jio and Airtel, leaving Vi fighting for relevance.

- If Vi cannot raise sufficient capital for a credible 5G rollout, it risks becoming strategically redundant.

- That outcome would write off a significant portion of the group's telecom investment and damage its broader reputation for capital discipline.

Global Economic Slowdown Risk:

- A potential global recession could significantly depress demand for cement, metals, and building materials.

- Hindalco's overseas operations are particularly exposed to a slowdown in China's construction sector, which remains a critical driver of global metals prices.

Tightening Environmental and Regulatory Compliance:

- Rising emission reduction requirements, waste disposal standards, and water use compliance are pushing up operational costs globally.

- At the same time, SEBI and RBI are increasing scrutiny of financial services businesses.

- Compliance missteps in either domain carry financial penalties and lasting reputational damage.

Raw Material Price Volatility:

- Coal, bauxite, and copper prices remain subject to sharp swings driven by geopolitical events and global supply chain shifts.

- Any sustained input cost spike that cannot be passed on to customers directly erodes margins in the group's most capital-intensive businesses, a recurring and structurally difficult challenge.

Shifting Brand Loyalty Among Gen Z:

- Younger Indian consumers are increasingly choosing digital-native brands with authentic sustainability credentials over legacy players.

- In fashion, sustainability has become a purchase driver, not just a differentiator. In financial services, digital ease matters more than branch presence.

- Brands that fail to credibly evolve their communication and digital experience risk losing this generation before they ever become loyal customers.

Summary Table - SWOT of Aditya Birla Group

IIDE Student Takeaway, Recommendations & Conclusion for Aditya Birla Group in 2026 and Beyond

Aditya Birla Group's SWOT analysis reveals a business that is impressively resilient yet genuinely exposed. UltraTech's market leadership, Hindalco's global metals franchise, and Aditya Birla Capital's growing financial services business are formidable assets in an economy with decades of infrastructure investment ahead.

But Vodafone Idea remains a live risk that goes far beyond a balance sheet problem. It depresses investor confidence and diverts strategic attention from higher-return priorities.

Core Tension: The group's scale and diversification provide stability, but that same complexity slows execution speed precisely when agility matters most. Reliance and Tata are not just competitors. They are redefining the benchmark for how fast large businesses can move.

Future Outlook: India's growth story remains one of the strongest globally, and Aditya Birla is positioned across nearly every sector that will benefit from it. The decisive variable is not opportunity. It is execution velocity.

Recommendations:

- Resolve Vodafone Idea Decisively: Ambiguity around Vi drains investor confidence and leadership focus. A clear resolution, whether merger, restructuring, or wind-down, immediately unlocks group-level value.

- Go Digital or Fall Behind: Retail and financial services must shift to mobile-first, AI-driven experiences that meet Gen Z where they already are. Incremental upgrades will not close the gap with Reliance and Tata.

- Make Sustainability a Revenue Driver: UltraTech's low-carbon cement and Hindalco's green aluminium deserve bold pricing strategies and louder brand narratives, not compliance footnotes.

Aditya Birla Group's diversified portfolio, global scale, and 160-year brand legacy position it strongly for continued leadership in India's rapidly growing economy.

However, the group faces real challenges, particularly the Vodafone Idea debt crisis, a widening digital gap, and relentless competition from Reliance and Tata across nearly every sector it operates in.

While UltraTech's infrastructure dominance, Hindalco's metals franchise, and Aditya Birla Capital's fintech growth ensure the group's near-term relevance, the pressure to modernise and move faster grows stronger every year.

Looking ahead, the group's future will depend on how decisively it resolves its telecom liability and how seriously it invests in digital-first consumer experiences. Expanding into green materials, deepening presence in Tier 2 and Tier 3 retail markets, and capturing India's fintech boom will be critical for staying ahead of a younger, more agile generation of competitors.

By leveraging its financial scale, global footprint, and early ESG commitments, Aditya Birla can stay ahead of rivals while building the digital and sustainability credentials that the next decade demands.

If it embraces these opportunities with the urgency they deserve, Aditya Birla Group will not just remain relevant. It will define what Indian conglomerate leadership looks like in 2030 and beyond.

Want to Know Why 2,50,000+ Students Trust Us?

Dive into the numbers that make us the #1 choice for career success

MBA - Level

Post Graduate in Digital Marketing & Business Strategy

Best For

Fresh Graduates

Mode of Learning

On Campus (Mumbai & Delhi)

Starts from

Jul 31, 2026

Duration

11 Months

Live & Online

Advanced Online Digital Marketing Course

Best For

Working Professionals

Mode of Learning

Online

Starts from

Aug 7, 2026

Duration

4-6 Months

Online

Professional Certification in AI Strategy

Best For

AI Enthusiasts

Mode of Learning

Online

Starts from

Sep 8, 2026

Duration

5 Months

On Campus

Advanced Certification in Artificial Intelligence

Best For

AI Enthusiasts

Mode of Learning

On Campus (Mumbai)

Starts from

Aug 31, 2026

Duration

3 Months

Online or Offline

Top AI Courses to Make You Future Ready!

Best For

AI Enthusiasts

Mode of Learning

2–5 Month Program

Starts from

Sep 8, 2026

Duration

Flexiable

Offline

Undergraduate Program in Digital Business & Entrepreneurship

Best For

12th Passouts

Mode of Learning

On Campus (Mumbai)

Starts from

Aug 19, 2026

Duration

3 Years

Offline

Degree In 2026 ≠ Enough Degree + Digital Skills = Future-Ready

Best For

12th Passouts

Mode of Learning

At IIDE Campus

Starts from

Aug 6, 2026

Duration

3 Years

Recent Post

You May Also Like

Aditya Birla Group is one of India's largest conglomerates with a 150+ year legacy, operating across cement, metals, fashion, financial services, telecom, and chemicals in 36+ countries.

Massive diversification across high-growth sectors, global scale in metals (Hindalco/Novelis) and cement (UltraTech India's largest), strong brand equity, and a 188,000+ employee global workforce.

Vodafone Idea's (Vi) ongoing financial distress, high debt levels in certain subsidiaries, commodity price sensitivity in metals and cement, and the complexity of managing a highly diversified conglomerate.

Tata Group and Reliance Industries at the conglomerate level; Ambuja/ACC in cement; Vedanta in metals; Reliance Retail & Trent in fashion; Jio Financial in financial services.

Through strategic global acquisitions (Novelis), continuous sector diversification, strong brand-building in B2C businesses like fashion and insurance, and sustained investment in R&D and green technology transitions.

Lead Trainer & Business Development Head at IIDE

Aditya Shastri leads the Business Development segment at IIDE and is a seasoned Content Marketing expert. With over a decade of experience, Aditya has trained more than 20,000 students and professionals in digital marketing, collaborating with prestigious institutions and corporations such as Jet Airways, Godrej Professionals, Pfizer, Mahindra Group, Publicis Worldwide, and many others. His ability to simplify complex marketing concepts, combined with his engaging teaching style, has earned him widespread admiration from students and professionals alike.

Aditya has spearheaded IIDE’s B2B growth, forging partnerships with over 40 higher education institutions across India to upskill students in digital marketing and business skills. As a visiting faculty member at top institutions like IIT Bhilai, Mithibai College, Amity University, and SRCC, he continues to influence the next generation of marketers.

Apart from his marketing expertise, Aditya is also a spiritual speaker, often traveling internationally to share insights on spirituality. His unique blend of digital marketing proficiency and spiritual wisdom makes him a highly respected figure in both fields.