Students Centric

Placements Report

Trackable results, real numbers

Reviews

Proven success, real voices

Trainers

Expert-led, Industry-Driven Training

Life at IIDE

Vibrant Spirit student life

Alumni

Successful Journeys, Inspiring Stories

Learning Centre

Webinars

Blogs

Case studies

Live, Interactive Masterclasses

Fresh Insights, quick reads

Real-life, Industry relevant

More

Hire from us

Hire Top Digital Marketing Talent

Work with us

Join Our Team, Make an Impact

Customised Training

Personalised digital marketing training for your company

Refer & earn

Simple, easy rewards

Contact us

Get the answers you need

About us

Know more about IIDE

Explore all course options

FOR FRESH GRADUATES

Post Graduation Program in Digital Marketing & Business Strategy- Ideal for Age: 20–25 Years

Can’t decide? Explore all our

Digital Marketing CoursesCOMPARE ALL 3 PROGRAMSOnline & Offline

Explore Top AI CoursesIndustry-Aligned TRACKMost Popular

UG Program in Digital Business & Entrepreneurship- Ideal for 12th Pass out / FY Degree Student

PARTNER PROGRAMS

Can’t decide? Explore all

BBA In Digital Marketing Colleges

Orginally Written by Aditya Shastri

Updated on May 18, 2026

Share on:

About Edelweiss Financial Services

Rashesh Shah started Edelweiss in 1995 with a team of three people and one conviction that India's capital markets were about to explode, and someone needed to build the infrastructure around them. What began as a boutique investment bank in Mumbai has since grown into one of India's most diversified financial conglomerates, touching everything from alternative asset management and mutual funds to insurance, credit, and asset reconstruction, with seven verticals, one holding company, and millions of customers.

The business runs on what Edelweiss calls a hub-and-spoke model, a central holding company that incubates independent businesses, each built to eventually stand on its own. That strategy is very much in motion right now, with several subsidiaries being prepared for independent listings, a move that could unlock value the market currently isn't giving it credit for.

The journey hasn't been without damage, though. The RBI restricted its asset reconstruction and finance units over concerns about the evergreening of stressed loans, and SEBI issued penalties related to AIF regulations. Those hits forced a real rethink, and what's emerged is a company deliberately pivoting away from high-debt lending towards a capital-light, fee-based model. Whether that transformation is complete or still halfway there is the most important question hanging over Edelweiss in 2026.

| Quick Stats | Edelweiss Financial Services (FY26) |

|---|---|

| Metric | Details |

| Founded | 1995 |

| Headquarters | Mumbai, India |

| Chairman & CEO | Rashesh Shah |

| Listed On | NSE & BSE |

| Consolidated Revenue | ₹10,865 crore |

| Consolidated PAT (Pre-MI) | ₹680 crore (+27% YoY) |

| Consolidated PAT (Post-MI) | ₹547 crore (+37% YoY) |

| Net Worth | ₹5,944 crore |

| Net Debt | ₹10,430 crore |

| Liquidity | ₹6,500 crore |

| Mutual Fund Equity AUM | ₹78,000 crore (+25% YoY) |

| Alternative Asset FPAUM | ₹44,710 crore (+32% YoY) |

| SIP Book | ₹623 crore (+58% YoY) |

| General Insurance GWP | ₹1,294 crore (+28% YoY) |

| 5-Year Stock Return | 230.51% vs Sensex 57.67% |

| Key Competitors | Bajaj Finance, HDFC, Kotak, ICICI Prudential |

| Business Verticals | 7 |

Products & Services by Edelweiss Financial Services

Here are some products and services Edelweiss Financial Services has to offer:

- General insurance

- Life insurance

- Mortgage loans

- Investment banking

- Investment management

- Wealth management

- Asset management

- Mutual fund

Competitors of Edelweiss Financial Services

- Goldman Sachs

- Morgan Stanley

- First Eagle

- ICICI Bank

If you're interested in how other Indian giants stack up, check out our SWOT analysis of Tata Motors for a detailed comparison of another diversified conglomerate navigating similar market pressures.

Now, since we learned about the bank, let us have a look at the SWOT Analysis of Edelweiss Financial Services.

SWOT Analysis of Edelweiss Financial Services

SWOT analysis of Edelweiss Financial Services is an examination of the company’s strengths, weaknesses, opportunities, and threats. This allows the organisation to understand its market position, as well as what areas need to be addressed and where it can shine. It also aids the corporation in strategising its business framework and elements affecting its growth.

To better understand the SWOT analysis of Edelweiss Financial Services, refer to the infographics below:

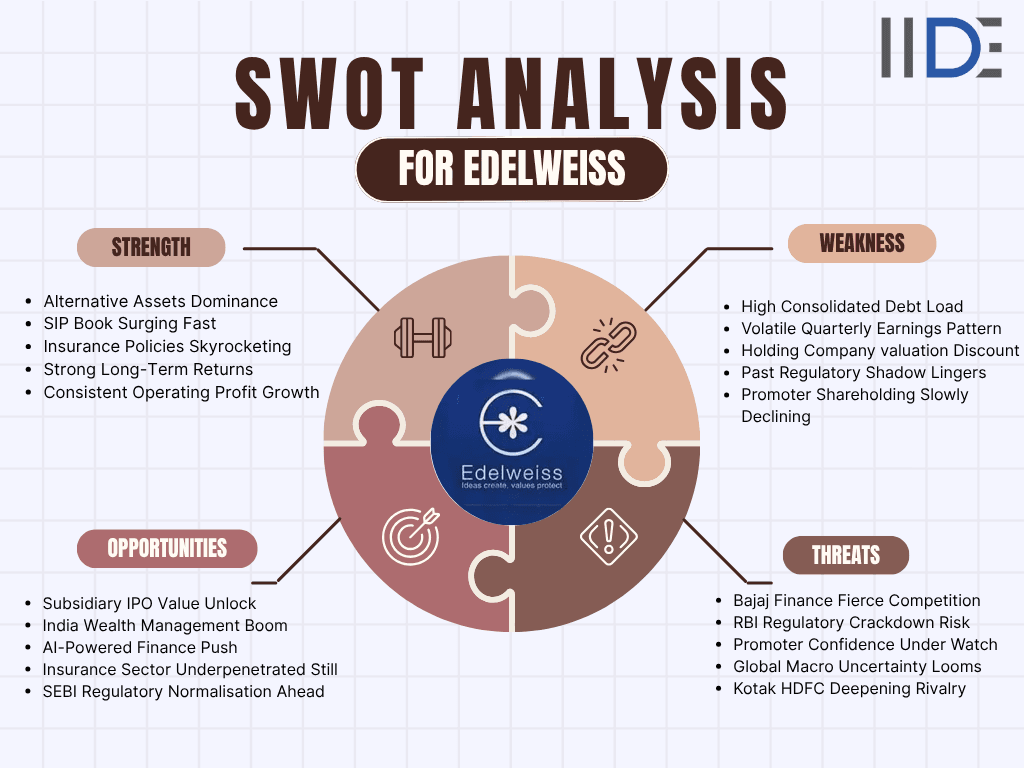

Strengths of Edelweiss Financial Services

Edelweiss Financial Services is one of the top companies in the industry and has many key advantages that help it succeed in the market. These advantages not only help it maintain its position in the markets it already operates in, but also allow it to grow and enter new ones.

- Alternative Asset Management is the Crown Jewel -The Alternatives business raised ₹10,855 crore in FY26, up 64% YoY, with FPAUM growing 32% to ₹44,710 crore. In a crowded asset management market, Edelweiss has built a dominant position in private credit, real estate, and infrastructure, a moat that's genuinely hard to replicate. Trendlyne

- Mutual Fund Business Has Real Momentum -Equity AUM grew 25% to ₹78,000 crore, and the SIP book expanded 58% to ₹623 crore. A 58% SIP growth means retail investors aren't just coming in, they're staying. That's sticky money, and sticky money builds durable businesses. Trendlyne

- Insurance is Quietly Becoming Serious - General insurance policies issued jumped 47% in FY26, with GWP rising 28% to ₹1,294 crore. In one of India's most underpenetrated sectors, Edelweiss is finding its footing faster than most people have noticed. Trendlyne

- Long-Term Stock Performance Speaks for Itself - Five-year stock return stands at 230.51% versus the Sensex's 57.67%. That kind of sustained outperformance doesn't happen by accident; it reflects a business that's compounding real value over time. Trendlyne

- Operating Profit Growth is Consistent - Edelweiss has delivered a 35.19% CAGR in operating profits, the kind of number that quietly earns long-term institutional confidence regardless of quarterly noise. iide

- Diversification is a Real Hedge - Seven verticals means no single bad quarter sinks the ship. When credit faced regulatory pressure, asset management compensated. When markets turned volatile, insurance premiums kept flowing. That natural balance is something most competitors simply don't have.

Weaknesses of Edelweiss Financial Services

A company’s weaknesses keep it from realising its greatest potential. To assist the company to excel in all areas, one should assess the weaknesses and seek to improve them.

- High Consolidated Debt Load - This is the number that makes analysts pause. Net debt currently sits at ₹10,430 crore, significant for a company that's trying to reinvent itself as a capital-light business. The pivot sounds good on paper, but the debt on the balance sheet tells a different story of where it's coming from. Trendlyne

- Volatile Quarterly Earnings Pattern - The annual numbers look great until you dig into the quarters. Revenue swung from ₹1,860 crore in September 2025 to ₹4,400 crore in December 2025, before crashing back to ₹1,918 crore in March 2026. That kind of swing makes forecasting nearly impossible and keeps conservative investors at arm's length. Trendlyne

- Holding Company Valuation Discount - This is a structural problem Edelweiss can't easily fix. As a conglomerate, the market rarely values it at the sum of its parts; there's always a discount applied for complexity, cross-holdings, and lack of a clean earnings story. Until subsidiaries list independently, that discount isn't going away.

- Past Regulatory Shadow Lingers - The RBI previously ordered Edelweiss Asset Reconstruction Company and ECL Finance to halt certain transactions over evergreening concerns, while SEBI issued penalties related to AIF regulations. The restrictions may have eased, but the reputational overhang with institutional investors hasn't fully disappeared. Embapro

- Promoter Shareholding Slowly Declining - It's a small move but worth watching. Promoter holding dropped from 32.71% in March 2025 to 32.26% in March 2026. No single quarter is alarming, but a consistent downward trend in promoter confidence is never a signal investors should ignore. Trendlyne

Opportunities for Edelweiss Financial Services

Opportunities are external variables that work in the company’s favour, and the company can take advantage of them to grow.

- Subsidiary IPO Value Unlock - This is arguably the biggest near-term opportunity on the table. Chairman Rashesh Shah specifically highlighted the filing of EAAA's DRHP for IPO as a key milestone, and the market is watching closely. Independent listings of subsidiaries would force the market to price each business on its own merit, effectively dismantling the holding company discount that's been suppressing the stock for years. iide

- India's Wealth Management Boom - India's affluent class is growing faster than the financial infrastructure built to serve it. Demand for sophisticated investment products, private credit, AIFs, and portfolio management services is at an all-time high. Edelweiss, with its alternatives platform already scaled, is sitting exactly where this wave is heading.

- Insurance Sector Still Largely Underpenetrated - India's insurance penetration remains well below the global average, and that gap is closing fast. Edelweiss General Insurance has already grown the policies issued by 47% in FY26. If that momentum continues, insurance could quietly become one of the company's most valuable businesses within the next five years. Trendlyne

- AI-Powered Finance Push - Every major financial services company is racing to embed AI into wealth advisory, credit underwriting, and customer acquisition. Edelweiss has the data, the customer base, and the product diversity to make AI work meaningfully across multiple verticals, not just as a gimmick but as a genuine cost and efficiency lever.

- SEBI and RBI Regulatory Normalisation - The worst of the regulatory trouble appears to be behind the company. As compliance improves and restrictions ease, previously closed business lines could reopen, particularly in asset reconstruction and structured credit, where Edelweiss has deep expertise and a head start over most competitors.

Threats to Edelweiss Financial Services

Threats are external elements that may have an impact on the bank. To avoid inflicting damage to the company, these concerns should be addressed as quickly as possible. The threats to Edelweiss Financial Services are as follows:

- Competition That Outguns You - Bajaj Finance, HDFC, Kotak, ICICI Prudential, these competitors consistently set performance benchmarks that Edelweiss is measured against, despite having far deeper pockets, stronger brand recall, and decades of customer trust. Competing across seven verticals against giants is expensive and exhausting. Embapro

- Regulatory Risk Isn't Fully Gone - The RBI and SEBI troubles may have eased, but haven't disappeared. Past restrictions on asset reconstruction and AIF-related penalties mean one fresh regulatory action could trigger a disproportionate market reaction, given the history. Embapro

- Global Macro Hits Alternatives Hard - Edelweiss's strongest business is also its most globally exposed. Foreign institutional capital pulls back fast when global risk appetite drops, and a prolonged rate cycle or geopolitical shock could slow alternatives fundraising significantly.

- Promoter Stake Slowly Slipping - Promoter holding fell from 32.71% to 32.26% in just one year. Small move, but in a founder-driven company, any consistent downward trend gets amplified by the market at the worst possible time. Trendlyne

- Quarterly Volatility Eroding Institutional Trust - Q4 FY26 profit dropped 66.80% quarter-on-quarter, sending the stock down 8% on results day. Sustained unpredictability makes it harder to attract the stable long-only institutional money needed for a meaningful valuation re-rating. Trendlyn

To better understand the SWOT analysis of Edelweiss Financial Services, refer to the infographics below:

If the AI opportunity in financial services caught your attention, understanding the business model of Google shows exactly how data-driven businesses build moats that are nearly impossible to break.

Now that we have come to the end of this thorough SWOT Analysis of Edelweiss Financial Services. Let’s see the summation of this article in the conclusion.

Learn Digital Marketing for FREE

Want to Know Why 2,50,000+ Students Trust Us?

Dive into the numbers that make us the #1 choice for career success

MBA - Level

Post Graduate in Digital Marketing & Business Strategy

Best For

Fresh Graduates

Mode of Learning

On Campus (Mumbai & Delhi)

Starts from

Jul 31, 2026

Duration

11 Months

Live & Online

Advanced Online Digital Marketing Course

Best For

Working Professionals

Mode of Learning

Online

Starts from

Aug 7, 2026

Duration

4-6 Months

Online

Professional Certification in AI Strategy

Best For

AI Enthusiasts

Mode of Learning

Online

Starts from

Jul 28, 2026

Duration

5 Months

Online or Offline

Top AI Courses to Make You Future Ready!

Best For

AI Enthusiasts

Mode of Learning

2–5 Month Program

Starts from

Jul 28, 2026

Duration

Flexiable

On Campus

Advanced Certification in Artificial Intelligence

Best For

AI Enthusiasts

Mode of Learning

On Campus (Mumbai)

Starts from

Jul 27, 2026

Duration

3 Months

Offline

Undergraduate Program in Digital Business & Entrepreneurship

Best For

12th Passouts

Mode of Learning

On Campus (Mumbai)

Starts from

Aug 19, 2026

Duration

3 Years

Offline

Degree In 2026 ≠ Enough Degree + Digital Skills = Future-Ready

Best For

12th Passouts

Mode of Learning

At IIDE Campus

Starts from

Aug 6, 2026

Duration

3 Years

Recent Post

Edelweiss is a diversified financial services company based in Mumbai. It operates across seven business verticals, including alternative asset management, mutual funds, life and general insurance, credit, and asset reconstruction. Think of it as a full-stack financial conglomerate, not just a bank, not just an asset manager, but both and more.

Yes, on an annual basis. Edelweiss reported a consolidated PAT of ₹680 crore in FY26, up 27% year-on-year. However, quarterly performance has been inconsistent, which is something investors should factor in before concluding from any single quarter.

Its primary competitors vary by business segment. In lending and credit, it competes with Bajaj Finance and Kotak. In asset management, ICICI Prudential and HDFC AMC are the key rivals. In insurance, it goes up against established players like HDFC Life and Star Health. No single competitor mirrors its exact business mix, which is both an advantage and a challenge.

The outlook is cautiously optimistic. The alternatives and mutual fund businesses are growing strongly, insurance is gaining real traction, and subsidiary IPOs could unlock significant hidden value. The company is actively pivoting towards a capital-light, fee-based model if that transition completes cleanly, the stock could look meaningfully undervalued at current levels. s

Two things stand out. First, the company's quarterly earnings remain highly volatile, with revenue swinging dramatically fluctuating across consecutive quarters in FY26. Second, the regulatory history with RBI and SEBI hasn't fully faded from institutional memory. Neither is a dealbreaker, but both deserve attention.

Lead Trainer & Business Development Head at IIDE

Aditya Shastri leads the Business Development segment at IIDE and is a seasoned Content Marketing expert. With over a decade of experience, Aditya has trained more than 20,000 students and professionals in digital marketing, collaborating with prestigious institutions and corporations such as Jet Airways, Godrej Professionals, Pfizer, Mahindra Group, Publicis Worldwide, and many others. His ability to simplify complex marketing concepts, combined with his engaging teaching style, has earned him widespread admiration from students and professionals alike.

Aditya has spearheaded IIDE’s B2B growth, forging partnerships with over 40 higher education institutions across India to upskill students in digital marketing and business skills. As a visiting faculty member at top institutions like IIT Bhilai, Mithibai College, Amity University, and SRCC, he continues to influence the next generation of marketers.

Apart from his marketing expertise, Aditya is also a spiritual speaker, often traveling internationally to share insights on spirituality. His unique blend of digital marketing proficiency and spiritual wisdom makes him a highly respected figure in both fields.