Students Centric

Placements Report

Trackable results, real numbers

Reviews

Proven success, real voices

Trainers

Expert-led, Industry-Driven Training

Life at IIDE

Vibrant Spirit student life

Alumni

Successful Journeys, Inspiring Stories

Learning Centre

Webinars

Blogs

Case studies

Live, Interactive Masterclasses

Fresh Insights, quick reads

Real-life, Industry relevant

More

Hire from us

Hire Top Digital Marketing Talent

Work with us

Join Our Team, Make an Impact

Customised Training

Personalised digital marketing training for your company

Refer & earn

Simple, easy rewards

Contact us

Get the answers you need

About us

Know more about IIDE

Explore all course options

FOR FRESH GRADUATES

Post Graduation Program in Digital Marketing & Business Strategy- Ideal for Age: 20–25 Years

Can’t decide? Explore all our

Digital Marketing CoursesCOMPARE ALL 3 PROGRAMSOnline & Offline

Explore Top AI CoursesIndustry-Aligned TRACKMost Popular

UG Program in Digital Business & Entrepreneurship- Ideal for 12th Pass out / FY Degree Student

PARTNER PROGRAMS

Can’t decide? Explore all

BBA In Digital Marketing Colleges

Orginally Written by Aditya Shastri

Updated on Jul 9, 2026

Share on:

Nippon Life Insurance is strong because of its solid finances, long-standing trust, and presence in many countries. Its main weak spots are its heavy reliance on Japan and a slower shift to digital tools. The biggest opportunity for the brand is India's fast-growing insurance market, while its biggest challenge is competition from newer, tech-first insurers.

Before diving into the article, we'd like to acknowledge the research behind this analysis. The research and initial analysis for this article were conducted by Sonali Gadia, a current student of IIDE's Online Digital Marketing Course. If you found this article helpful, feel free to connect with Sonali on LinkedIn and send her a quick note of appreciation for her research and hard work. She'll surely appreciate it!

| SWOT ANALYSIS TABLE | |

|---|---|

| Strengths | Weaknesses |

|

|

| Opportunities | Threats |

|

|

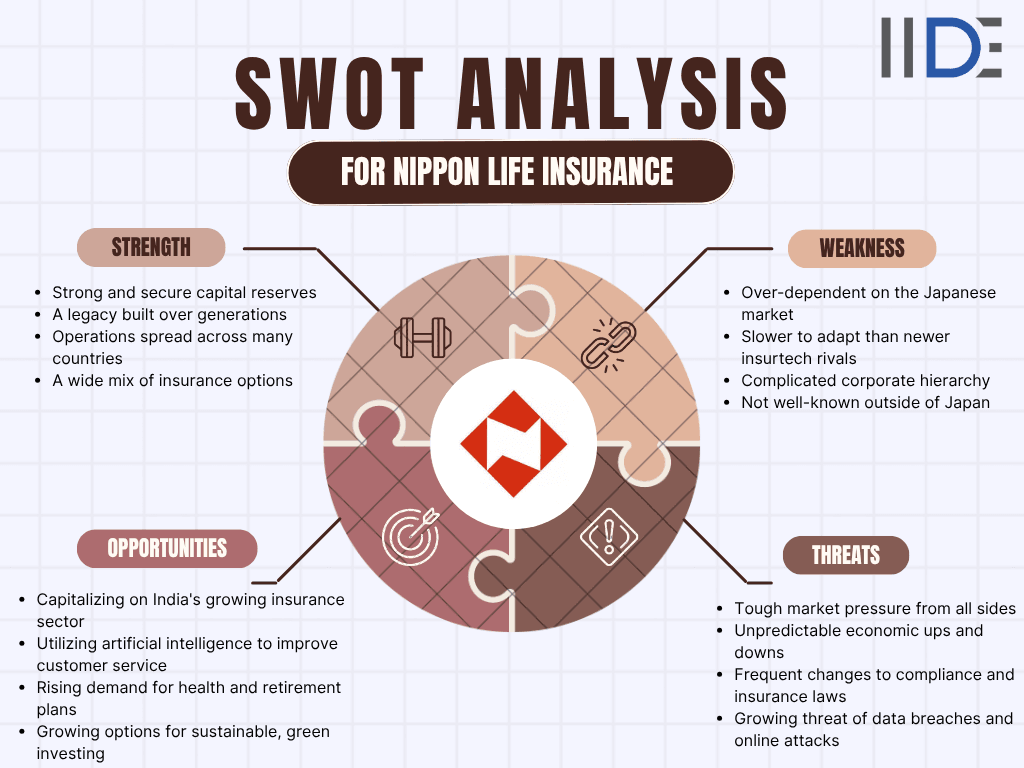

Here's a visual snapshot of SWOT Analysis of Nippon Life Insaurance:

Learn Digital Marketing for FREE

What Are Nippon Life Insurance's Strengths?

Nippon Life's biggest strength is that it's built on trust and financial stability. It has strong money reserves, a name people have relied on for generations, and a presence in several countries. These strengths have helped it survive tough markets and changing customer needs.

1. Strong and Stable Finances

- It holds a very large pool of assets, making it one of the biggest institutional investors in Japan.

- Its money is spread across many types of investments, like bonds, stocks, real estate, and infrastructure, so it isn't overly dependent on just one.

- It comfortably meets the money-safety rules set by regulators.

- It has stayed profitable even when the world economy has had rough patches.

- Credit rating agencies rate it highly, which builds confidence among customers and investors.

2. A Brand Trusted for Generations

- Families in Japan have trusted Nippon Life for several generations.

- It has a strong reputation for being honest and doing business the right way.

- Almost everyone in Japan recognizes the Nippon Life name.

- It has decades of experience in understanding risk, backed by huge amounts of past data.

- It knows how to plan for long-term risks, not just short-term ones.

3. A Strong Presence Across the World

- It now has a presence in Japan, India, the US, Australia, and Europe.

- In India, it works through IndusInd Nippon Life Insurance (formerly known as Reliance Nippon Life), combining its own know-how with local expertise.

- Partnering with local players lowers the risk of entering a brand-new market.

- Local partners help it understand local rules and customers faster.

- It can gain customers quicker with an already-existing network on the ground.

4. A Wide Range of Products

- Term life insurance

- Whole life insurance

- Retirement and pension plans

- Health insurance

- Group insurance for companies

- Investment-linked insurance plans

5. Smart Investment Management

- It invests customer premiums across government bonds, company bonds, stocks, real estate, and infrastructure projects.

- Spreading money across different areas lowers overall risk.

- Good investment returns help it offer better products while staying financially safe.

What Are Nippon Life Insurance's Weaknesses?

Nippon Life's biggest weakness is how much it depends on Japan, a market that isn't growing as fast as it used to. It's also slower to adopt digital tools compared to newer, tech-first insurers.

1. Too Dependent on Japan

- Japan's population is ageing fast, which means fewer young people are buying new policies.

- The birth rate in Japan is falling, which limits the industry's future growth.

- Interest rates in Japan have stayed low for years, which makes it harder to earn good returns on safe investments.

- Japan's economy is growing slowly, leaving less room for people to spend on insurance.

- The Japanese market is already saturated, leaving little room to grow further at home.

2. Slower to Go Digital

- Buying a policy takes longer than it does with fully digital insurers.

- It still relies heavily on traditional agents and sales channels.

- AI-based policy approval is still being rolled out, while some rivals already use it widely.

- Its offerings feel less personalized compared to data-driven digital insurers.

- Older technology systems can slow down how fast it can innovate.

3. A Complicated Company Structure

- Decisions take longer to make across different teams and countries.

- Running such a large structure costs more.

- Coordinating between international offices isn't easy.

- Bringing newly acquired businesses into the fold takes time.

- New plans and ideas take longer to actually roll out.

4. Not Very Well Known Outside Japan

- In markets like India, people know the local brand (like IndusInd Nippon Life) far better than "Nippon Life" itself.

- It mostly grows abroad through partnerships and joint ventures, not its own name.

- It doesn't advertise directly to consumers internationally the way global brands like Allianz do.

- It's better known among institutions and investors than everyday customers.

5. Higher Running Costs

- It runs a large network of branches.

- It still relies on traditional distribution methods.

- Following rules across many countries adds to compliance costs.

- Upgrading old technology needs constant investment.

- A large workforce means higher administrative costs.

6. Hit by Low Interest Rates

- Government bonds in Japan earn very little.

- This lowers the income the company earns from its investments.

- Long-term guaranteed products become harder to sustain.

- It has to take on riskier international investments just to earn a decent return.

Curious how another global insurance giant stacks up? Check out our SWOT analysis of MetLife to see how its strengths and challenges compare to Nippon Life's.

What Are Nippon Life Insurance's Opportunities?

Nippon Life's biggest opportunity lies in fast-growing markets like India, along with using AI and technology to serve customers better.

1. India's Growing Insurance Market

- It can grow its tie-up with IndusInd Bank to reach more customers through the bank's network.

- It can launch cheaper, simpler plans for price-conscious buyers.

- It can sell more policies online to reach India's younger, internet-first population.

- It can expand into smaller towns and cities where insurance is still catching on.

- It can run awareness programs to help first-time buyers understand insurance.

2. Using AI and Digital Tools

- Using AI to speed up policy approvals.

- Automating how claims get settled.

- Offering personalised insurance suggestions to customers.

- Running chatbots for round-the-clock customer support.

- Using AI to catch fraud early.

3. Rising Demand for Health and Retirement Plans

As people live longer and healthcare gets more expensive worldwide, more people are looking for health and retirement cover. The following insaurance are covered:

- Health insurance

- Retirement planning

- Pension products

- Critical illness cover

- Long-term care insurance

4. Sustainable and ESG-Friendly Investments

- Green investment funds channel capital into eco-friendly assets for stable returns.

- Insurance products built around ESG values attract socially conscious consumers.

- Investments in sustainable infrastructure provide reliable, long-term yields for future claims.

- Insurance solutions for climate-related risks protect corporate clients from extreme weather losses.

5. Growing Through Partnerships

- Teaming up with local entities bypasses regulatory hurdles to enter markets faster.

- Partnering with regional organizations provides instant insights into local consumer habits.

- Sharing operational burdens with a local ally cuts the risk of expanding abroad.

- Combining distinct institutional strengths helps design unique products for diverse needs.

- Leveraging a partner's established network gives instant access to a large customer base.

What Are the Threats to Nippon Life Insurance?

Nippon Life's biggest threat is the rising competition from both large global insurers and newer, tech-first companies, along with changing rules and rising cyber risks.

1. Tough Competition From All Sides

- LIC has an unmatched network and deep trust across India.

- HDFC Life keeps pushing hard on digital products and marketing.

- SBI Life uses the massive reach of the State Bank of India to enter smaller towns.

- Allianz competes globally with deep pockets and a strong brand.

- AIA is strongly focused on fast-growing Asian markets.

- Prudential leans heavily on digital health platforms and emerging markets.

- Lemonade, a digital-only insurer, offers instant, AI-based policies that appeal to younger buyers.

- Ping An combines insurance with tech and healthcare in one ecosystem.

2. Changing Rules and Regulations

- Requirements to hold more capital force insurers to keep extra emergency funds, reducing money available for growth.

- New compliance standards create heavy administrative burdens and increase operational costs for global firms.

- Stronger customer protection laws demand higher transparency, reducing the risk of costly misselling penalties.

- Data privacy rules limit how customer information is processed, requiring expensive upgrades to security systems.

- Restrictions on investing money across borders make it harder to diversify assets and maximize international returns.

3. Rising Cybersecurity Risks

- Customer data leaks expose highly sensitive personal information, leading to massive regulatory fines and lawsuits.

- Identity theft allows criminals to open fraudulent accounts or claim benefits using stolen policyholder credentials.

- Ransomware attacks lock critical corporate databases, forcing expensive downtime or massive payouts to recover files.

- Financial fraud enables scammers to divert premium payments or submit fake claims that drain company cash.

- Disruptions to daily operations freeze digital platforms, preventing agents from selling policies and helping customers.

4. Economic Ups and Downs

- Fewer people buy new policies because households tighten their budgets and cut back on non-essential expenses.

- More people let existing policies lapse to save cash, causing insurers to lose steady premium revenue.

- Investment returns fall as stock markets drop and interest rates fluctuate, shrinking the insurer's core profits.

- More claims come in during tough times as hard-hit policyholders look to recoup losses through insurance benefits.

- People spend less overall, dampening general business activity and reducing commercial insurance sales.

5. Changing Customer Expectations

- Instant sign-ups require modern digital platforms that approve applications in minutes rather than weeks.

- Personalised plans demand flexible underwriting so policies fit an individual’s exact lifestyle and budget.

- Faster claim settlements push insurers to automate payouts so customers get financial relief immediately.

- Mobile-first experiences mean clients expect to manage all their policy needs through a smartphone app.

- Clear, upfront pricing eliminates hidden fees and confusing jargon to build immediate trust with buyers.

Curious how a global insurance leader like Allianz stacks up? Check out our SWOT analysis of Allianz to see its strengths, weaknesses, opportunities, and threats.

About Nippon Life Insurance

Founded in 1889 in Osaka, Japan by Sukesaburo Hirose, Nippon Life Insurance (also known as Nissay) is one of Japan's oldest and largest life insurance companies. It's a mutual company, meaning it's owned by its policyholders rather than outside shareholders. Beyond life insurance, it also manages pensions, healthcare plans, and large-scale investments, and has grown into one of the world's biggest institutional investors.

Outside Japan, it has expanded through partnerships and acquisitions across Asia, the US, Europe, and Australia, including a growing presence in India through IndusInd Nippon Life Insurance. Its focus has always been on long-term financial security rather than chasing quick growth. Brand Slogan: "For Your Future," reflecting its mission of helping customers build lasting financial confidence.

| Particular | Details |

|---|---|

| Founded | 1889 |

| Founder | Sukesaburo Hirose |

| Headquarters | Osaka, Japan |

| Industry | Life Insurance & Financial Services |

| Global Presence | Japan, India, USA, Australia, Europe & Asia |

| Indian Business | IndusInd Nippon Life Insurance (formerly Reliance Nippon Life) |

| Core Products | Life Insurance, Retirement Plans, Investment Products, Health Insurance |

| Business Model | Mutual Life Insurance Company |

Key Takeaways & Recommendations

Nippon Life's story shows that trust, financial discipline, and a focus on the customer can carry a company for over a century. But holding onto that position today means moving faster on technology and connecting better with younger customers, who expect instant, digital-first service.

The core tension for Nippon Life is this: it's a company built on old-world trust, trying to compete in a new, fast-moving, digital-first industry. Legacy brand value alone won't be enough going forward.

Recommendations:

- Speed up the use of AI in underwriting and claims processing.

- Build more digital-first insurance options aimed at younger customers.

- Strengthen brand visibility in fast-growing markets outside Japan.

- Invest more in cybersecurity and data protection.

- Use its strong financial base to launch new health and retirement products.

Future Outlook: Nippon Life is well-placed for the future if it can balance its long-standing values with faster innovation, especially in markets like India where growth potential is high.

Want to Know Why 2,50,000+ Students Trust Us?

Dive into the numbers that make us the #1 choice for career success

MBA - Level

Post Graduate in Digital Marketing & Business Strategy

Best For

Fresh Graduates

Mode of Learning

On Campus (Mumbai & Delhi)

Starts from

Jul 31, 2026

Duration

11 Months

Live & Online

Advanced Online Digital Marketing Course

Best For

Working Professionals

Mode of Learning

Online

Starts from

Aug 7, 2026

Duration

4-6 Months

Online

Professional Certification in AI Strategy

Best For

AI Enthusiasts

Mode of Learning

Online

Starts from

Sep 8, 2026

Duration

5 Months

On Campus

Advanced Certification in Artificial Intelligence

Best For

AI Enthusiasts

Mode of Learning

On Campus (Mumbai)

Starts from

Aug 31, 2026

Duration

3 Months

Online or Offline

Top AI Courses to Make You Future Ready!

Best For

AI Enthusiasts

Mode of Learning

2–5 Month Program

Starts from

Sep 8, 2026

Duration

Flexiable

Offline

Undergraduate Program in Digital Business & Entrepreneurship

Best For

12th Passouts

Mode of Learning

On Campus (Mumbai)

Starts from

Aug 19, 2026

Duration

3 Years

Offline

Degree In 2026 ≠ Enough Degree + Digital Skills = Future-Ready

Best For

12th Passouts

Mode of Learning

At IIDE Campus

Starts from

Aug 6, 2026

Duration

3 Years

Recent Post

Its biggest strength is the trust and financial strength it has built over more than 130 years. Customers expect an insurer to still be around decades later to honour their claims, and Nippon Life's large reserves, spread-out investments, and strong credit ratings back that up.

Its main weakness is how much it still depends on Japan for the bulk of its business. Japan's population is ageing, birth rates are falling, and interest rates have stayed low for years, all of which makes it harder to grow at home the way it once did.

The biggest threats are rising competition and a fast-changing industry. It's up against both established rivals like Allianz and LIC and newer digital-first insurers like Lemonade, while also facing tighter regulations and growing cybersecurity risks as insurance moves online.

Globally, it competes with names like Allianz, AIA, and Prudential. In India, where it operates through IndusInd Nippon Life Insurance, its rivals include LIC, HDFC Life, and SBI Life. It also faces newer digital-first players like Lemonade and Ping An.

India is one of the world's fastest-growing insurance markets, with rising incomes and low insurance penetration leaving a lot of room to grow. Nippon Life already has a foothold here through IndusInd Nippon Life Insurance, making it a key growth market as Japan's own market slows down.

Lead Trainer & Business Development Head at IIDE

Aditya Shastri leads the Business Development segment at IIDE and is a seasoned Content Marketing expert. With over a decade of experience, Aditya has trained more than 20,000 students and professionals in digital marketing, collaborating with prestigious institutions and corporations such as Jet Airways, Godrej Professionals, Pfizer, Mahindra Group, Publicis Worldwide, and many others. His ability to simplify complex marketing concepts, combined with his engaging teaching style, has earned him widespread admiration from students and professionals alike.

Aditya has spearheaded IIDE’s B2B growth, forging partnerships with over 40 higher education institutions across India to upskill students in digital marketing and business skills. As a visiting faculty member at top institutions like IIT Bhilai, Mithibai College, Amity University, and SRCC, he continues to influence the next generation of marketers.

Apart from his marketing expertise, Aditya is also a spiritual speaker, often traveling internationally to share insights on spirituality. His unique blend of digital marketing proficiency and spiritual wisdom makes him a highly respected figure in both fields.