Application Deadline for 3-Year UG Program closes on 31st Aug. Book a Counselling to know more

Students Centric

Placements Report

Trackable results, real numbers

Reviews

Proven success, real voices

Trainers

Expert-led, Industry-Driven Training

Life at IIDE

Vibrant Spirit student life

Alumni

Successful Journeys, Inspiring Stories

Learning Centre

Webinars

Blogs

Case studies

Live, Interactive Masterclasses

Fresh Insights, quick reads

Real-life, Industry relevant

More

Hire from us

Hire Top Digital Marketing Talent

Work with us

Join Our Team, Make an Impact

Customised Training

Personalised digital marketing training for your company

Refer & earn

Simple, easy rewards

Contact us

Get the answers you need

About us

Know more about IIDE

Explore all course options

FOR FRESH GRADUATES

Post Graduation Program in Digital Marketing & Business Strategy- Ideal for Age: 20–25 Years

Can’t decide? Explore all our

Digital Marketing CoursesCOMPARE ALL 3 PROGRAMSOnline & Offline

Explore Top AI CoursesIndustry-Aligned TRACKMost Popular

UG Program in Digital Business & Entrepreneurship- Ideal for 12th Pass out / FY Degree Student

PARTNER PROGRAMS

Can’t decide? Explore all

BBA In Digital Marketing Colleges

Orginally Written by Aditya Shastri

Updated on Jun 2, 2026

Share on:

Is Digital Marketing the Right Career for You?

Find out in a free 45-min masterclass · Career paths, roles and growth explained · By Karan Shah, Founder & CEO, IIDE

Is Digital Marketing the Right Career for You?

Find out in a free 45-min masterclass · Career paths, roles and growth explained · By Karan Shah, Founder & CEO, IIDE

What is a SWOT Analysis?

Muthoot Finance didn't become India's largest gold loan company by simply being in the right business at the right time. Behind the 7,391 branches and Rs 1.64 lakh crore AUM lies a strategic story worth examining, one that reveals both extraordinary strengths and real vulnerabilities in 2026.

Competing against banks, NBFCs, and fintechs simultaneously is the defining challenge for every gold loan player and understanding how India's biggest bank navigates a similar multi-front battle is best explored in the SWOT Analysis of HDFC.

Now that we have understood the importance of the SWOT analysis, let’s dive into how Muthoot Finance used this matrix tool to its advantage.

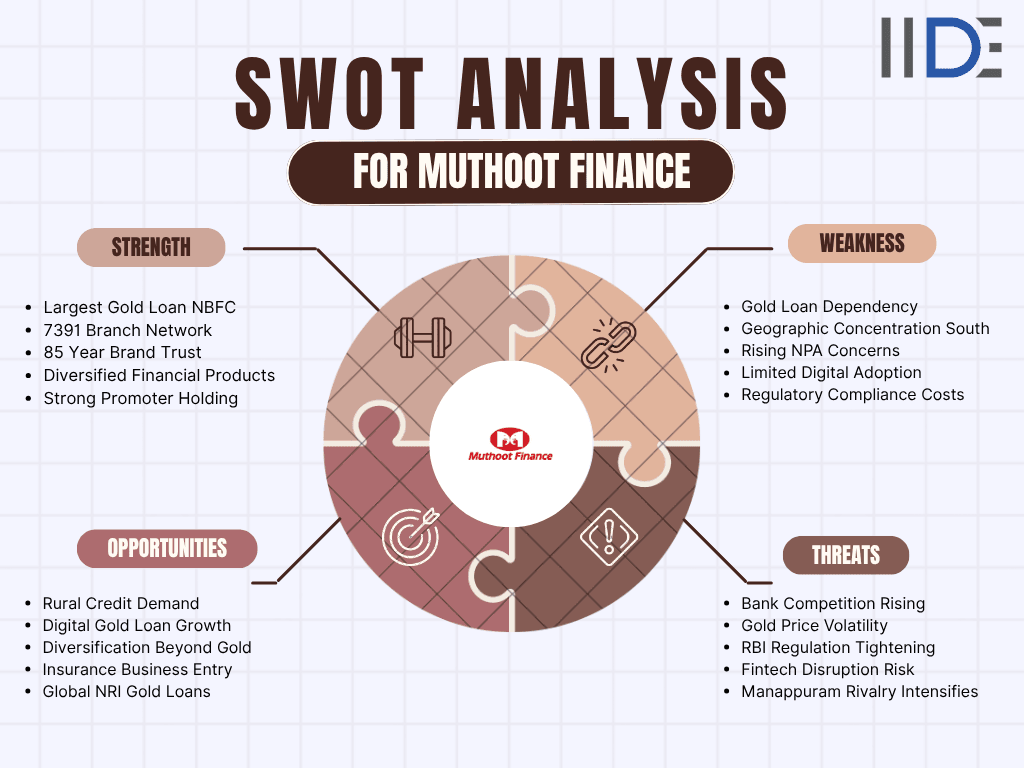

Strengths of the company

Muthoot Finance has a long list of strengths that make it a big player in the finance market. Some of its strengths include constant growth and a wide presence. Strengths are aspects of an organisation that contribute effectively or a system that distinguishes them from their competitors. Any aspect of the organisation is considered a strength if it brings them a clear advantage.

- Largest Gold Loan NBFC in India - With a Gold Loan AUM of Rs 1,02,956 crore, nearly double that of Manappuram Finance, Muthoot's scale gives it unmatched borrowing power, lower costs, and brand recognition that no smaller player can replicate.

- 7,391 Branch Network - Spread across all 29 states and union territories, Muthoot's physical reach goes deep into semi-urban and rural India, where gold loan demand is highest, a distribution advantage no fintech or bank comes close to matching.

- 85-Year Brand Trust - Eight decades of customer trust, particularly in South India, means that when someone walks in with their family gold, they choose Muthoot without a second thought. In this business, that trust is the product.

- Diversified Financial Products - Beyond gold loans, Muthoot now operates in home loans, microfinance, vehicle loans, insurance, and foreign exchange, reducing single-stream revenue dependency and opening new customer acquisition channels across India.

- Strong Promoter Holding - With promoters holding 73.4% of the company, strategic decisions are made with decades in mind. That founder-family commitment signals long-term confidence that institutional investors consistently reward.

Weaknesses of the company

Being such a strong player in the market, it has very few weaknesses. An organisation needs to recognise; thus,,, their weaknesses. It aids the company to grow and lead the market. Muthoot Finance’s weaknesses are low but not zero, thus let’s look into its main shortcomings.

- Gold Loan Dependency - Gold loans still account for 90% of total AUM. Any sustained drop in gold prices like the 8-12% dip in early 2026 directly compresses collateral values and puts immediate pressure on asset quality across the entire portfolio.

- Geographic Concentration in South India - A disproportionate share of Muthoot's business remains in Kerala, Tamil Nadu, and Andhra Pradesh. Any regional economic slowdown or political disruption hits the consolidated numbers harder than it should for a company of this scale.

- Rising NPA Concerns - Scaling to 7,391 branches while managing non-gold loan subsidiaries, microfinance and vehicle loans, particularly, is showing cracks. Rising NPAs in these verticals are a growing drag on consolidated profitability that cannot be ignored.

- Limited Digital Adoption - The iMuthoot app exists, but digital gold loan penetration remains low. The core customer base, older, rural, semi-urban, is not digitally comfortable, creating a structural gap that fintech competitors are actively exploiting.

- Regulatory Compliance Costs - New 2026 RBI guidelines on tiered LTV limits, stricter KYC, and gold auction norms add operational complexity and cost across every one of its 7,391 branches, a compliance burden that smaller rivals don't face at the same scale.

Opportunities of the company

Opportunities are targets to hit for something good to happen. These shouldn’t have to be game-changers: even minute advantages can help a company compete effectively. Changes in government regulations affecting their sector, as well as changes in social patterns, demographic profiles, and lifestyles, can all present fascinating opportunities.

- Rural Credit Demand - India's rural households hold an estimated 25,000+ tonnes of gold, most of it sitting idle. Muthoot's branch depth in these markets gives it first-mover access to a credit opportunity that banks and fintechs are still struggling to reach.

- Digital Gold Loan Growth - Muthoot's 85-year brand trust, combined with a scaled digital platform, could capture urban millennials who want fintech speed with NBFC reliability, a combination no pure-play digital lender can offer.

- Diversification Beyond Gold - Home loans, microfinance, and vehicle loans are still small relative to the core business. Aggressively scaling these in Tier 2 and 3 cities could meaningfully reduce gold concentration risk while adding stable, long-tenure revenue streams.

- Insurance Business Entry - With 2 lakh customers walking into branches daily, cross-selling insurance products is a high-margin, low-capital opportunity. Shareholders approved the insurance intermediary business in May 2026. The distribution engine is already built.

- Global NRI Gold Loans - With existing branches in the UAE, UK, and US, Muthoot is uniquely positioned to offer NRI-focused gold loan and remittance products to India's 32 million-strong diaspora, a high-value segment no domestic competitor can easily enter.

Threats to the company

Anything that might have a negative impact on your firm from the outside is considered a threat. Consider the challenges you’ll encounter in bringing your product to market and marketing it. It could be a drop in the quality of the products or services presented. However, whatever it may be, anything that could cause harm to the organisation should be recognised.

- Bank Competition Rising - SBI, HDFC Bank, and Kotak are aggressively expanding gold loan portfolios at lower interest rates backed by cheaper cost of funds that NBFCs structurally cannot match. Customer retention is becoming increasingly expensive.

- Gold Price Volatility - An 8-12% gold price drop in early 2026 directly reduced collateral values, borrower confidence, and new loan disbursements. With 90% AUM in gold loans, there is no buffer when prices fall sharply.

- RBI Regulation Tightening - New 2026 tiered LTV limits and stricter auction norms directly impact disbursement speed Muthoot's single biggest competitive advantage over banks. Every new regulation chips away at the operational edge it has built over 85 years.

- Fintech Disruption Risk - Rupeek and other digital gold loan startups are winning urban customers with app-based doorstep loans and competitive rates. Muthoot's rural moat is intact, but its urban premium segment is being steadily eroded.

- Manappuram Rivalry Intensifies - Manappuram is closing the gap on technology and product breadth. As the distance between the two narrows, Muthoot will need continuous reinvestment to maintain the dominance it has long taken for granted.

Now that you have a complete picture of Muthoot Finance's strategic position, explore how India's largest fintech challenger is disrupting the same lending market the SWOT Analysis of Paytm shows what digital disruption looks like from the other side.

Conclusion

Muthoot Finance's story is not just about gold; it is about trust built over 85 years, one loan at a time. The branch network, the AUM scale, and the promoter commitment give it a foundation that no bank or fintech can dismantle overnight. But the business is at an inflexion point. Gold price volatility, aggressive bank competition, tightening RBI regulations, and a digitally-savvy new generation of borrowers are all pushing Muthoot to evolve faster than it ever has before.

The company that built India's largest gold loan empire on physical branches and family trust now needs to prove it can win in a digital-first, regulation-heavy, multi-product world. The infrastructure is there. The brand is there. The question in 2026 is whether the strategy can keep pace with the speed at which the market is changing around it.

Want to Know Why 2,50,000+ Students Trust Us?

Dive into the numbers that make us the #1 choice for career success

MBA - Level

Post Graduate in Digital Marketing & Business Strategy

Best For

Fresh Graduates

Mode of Learning

On Campus (Mumbai & Delhi)

Starts from

Oct 1, 2026

Duration

11 Months

Live & Online

Advanced Online Digital Marketing Course

Best For

Working Professionals

Mode of Learning

Online

Starts from

Sep 4, 2026

Duration

4-6 Months

Online

Professional Certification in AI Strategy

Best For

AI Enthusiasts

Mode of Learning

Online

Starts from

Sep 8, 2026

Duration

5 Months

Online or Offline

Top AI Courses to Make You Future Ready!

Best For

AI Enthusiasts

Mode of Learning

2–5 Month Program

Starts from

Sep 8, 2026

Duration

Flexiable

On Campus

Advanced Certification in Artificial Intelligence

Best For

AI Enthusiasts

Mode of Learning

On Campus (Mumbai)

Starts from

Sep 1, 2026

Duration

3 Months

Offline

Undergraduate Program in Digital Business & Entrepreneurship

Best For

12th Passouts

Mode of Learning

On Campus (Mumbai)

Starts from

Aug 19, 2026

Duration

3 Years

Offline

Degree In 2026 ≠ Enough Degree + Digital Skills = Future-Ready

Best For

12th Passouts

Mode of Learning

At IIDE Campus

Starts from

Aug 19, 2026

Duration

3 Years

Recent Post

Muthoot Finance is India's largest gold loan NBFC, founded in 1939 in Kerala by M. George Muthoot. It is famous for making gold loans accessible to millions of Indians, particularly in rural and semi-urban areas, by accepting household gold jewellery as security. Today, it operates 7,391 branches, holds 202 tonnes of gold, and serves over 2 lakh customers daily.

Muthoot Finance's strengths include: India's largest gold loan NBFC with Rs 1,02,956 crore gold loan AUM; an unmatched 7,391-branch network across 29 states; 85 years of brand trust, especially in South India; a diversified product portfolio beyond gold loans; and strong promoter holding of 73.4%, signalling long-term commitment.

Muthoot Finance's key weaknesses include 90% AUM concentration in gold loans making it vulnerable to gold price swings, heavy geographic concentration in South India, rising NPAs in non-gold subsidiaries like microfinance and vehicle loans, limited digital adoption compared to fintech competitors, and high compliance costs from new 2026 RBI regulations on tiered LTV limits.

Muthoot Finance's biggest opportunities include tapping India's rural credit demand backed by 25,000+ tonnes of household gold, scaling its digital gold loan platform to capture urban millennials, expanding into home loans and microfinance to reduce gold concentration risk, cross-selling insurance products to its 2 lakh daily branch visitors, and growing NRI gold loan services in UAE, UK, and US.

Muthoot Finance's primary threats include banks like SBI and HDFC expanding gold loans at lower interest rates, gold price volatility (8-12% drop in early 2026) directly compressing collateral values, new RBI 2026 tiered LTV regulations impacting disbursement speed, digital gold loan fintechs like Rupeek eroding urban customers, and intensifying rivalry from Manappuram Finance.

Muthoot Finance's SWOT analysis reveals India's largest gold loan company with unmatched branch depth and brand trust (strengths), offset by 90% gold loan concentration and limited digital presence (weaknesses). Key opportunities lie in rural credit demand, digital lending, and insurance cross-selling. Main threats include bank competition, gold price volatility, and RBI regulatory tightening.

Lead Trainer & Business Development Head at IIDE

Aditya Shastri leads the Business Development segment at IIDE and is a seasoned Content Marketing expert. With over a decade of experience, Aditya has trained more than 20,000 students and professionals in digital marketing, collaborating with prestigious institutions and corporations such as Jet Airways, Godrej Professionals, Pfizer, Mahindra Group, Publicis Worldwide, and many others. His ability to simplify complex marketing concepts, combined with his engaging teaching style, has earned him widespread admiration from students and professionals alike.

Aditya has spearheaded IIDE’s B2B growth, forging partnerships with over 40 higher education institutions across India to upskill students in digital marketing and business skills. As a visiting faculty member at top institutions like IIT Bhilai, Mithibai College, Amity University, and SRCC, he continues to influence the next generation of marketers.

Apart from his marketing expertise, Aditya is also a spiritual speaker, often traveling internationally to share insights on spirituality. His unique blend of digital marketing proficiency and spiritual wisdom makes him a highly respected figure in both fields.