Students Centric

Placements Report

Trackable results, real numbers

Reviews

Proven success, real voices

Trainers

Expert-led, Industry-Driven Training

Life at IIDE

Vibrant Spirit student life

Alumni

Successful Journeys, Inspiring Stories

Learning Centre

Webinars

Blogs

Case studies

Live, Interactive Masterclasses

Fresh Insights, quick reads

Real-life, Industry relevant

More

Hire from us

Hire Top Digital Marketing Talent

Work with us

Join Our Team, Make an Impact

Customised Training

Personalised digital marketing training for your company

Refer & earn

Simple, easy rewards

Contact us

Get the answers you need

About us

Know more about IIDE

Explore all course options

FOR FRESH GRADUATES

Post Graduation Program in Digital Marketing & Business Strategy- Ideal for Age: 20–25 Years

Can’t decide? Explore all our

Digital Marketing CoursesCOMPARE ALL 3 PROGRAMSOnline & Offline

Explore Top AI CoursesIndustry-Aligned TRACKMost Popular

UG Program in Digital Business & Entrepreneurship- Ideal for 12th Pass out / FY Degree Student

PARTNER PROGRAMS

Can’t decide? Explore all

BBA In Digital Marketing Colleges

Orginally Written by Aditya Shastri

Updated on May 20, 2026

Share on:

Aditya Birla Capital is one of India's most powerful financial services companies, but what truly sets it apart in 2026?

With fintech startups disrupting traditional finance and banking giants expanding aggressively, can ABCL hold its ground and grow?

This analysis dives deep into ABCL's strengths, weaknesses, opportunities, and threats to answer exactly that. Whether you are a business student, investor, or aspiring entrepreneur, the strategic insights here will help you understand how India's most diversified financial conglomerate is navigating one of its most competitive eras yet.

Before diving in, the research and initial analysis for this piece were conducted by Richa Shrestha, a current student in IIDE's Online Digital Marketing Course, November Batch 2025.

If you find the article Interesting feel free to connect with Richa Shrestha and send her a note of appreciation for her fantastic research work.

About Aditya Birla Capital

Aditya Birla Capital Limited (ABCL) is the financial services holding company of the Aditya Birla Group, one of India's most trusted conglomerates founded in 1857 by Seth Shiv Narayan Birla in Pilani, Rajasthan.

Today, the group spans 42 countries across Asia, Europe, Africa, and the Americas, generating a combined annual revenue of approximately US$70 billion.

Established in 2007 and chaired by Kumar Mangalam Birla, ABCL brings together life insurance, health insurance, mutual funds, home loans, personal loans, and MSME lending under one unified ecosystem, making it a true one-stop financial solutions provider for millions of Indians.

At the heart of ABCL's digital ambition is the ABCD (Aditya Birla Capital Digital) platform, built around the vision of making "Everything Finance as Simple as ABCD."

Quick Stats about Aditya Birla Capital:

| Detail | Info |

|---|---|

| Founded | 2007 (Aditya Birla Group est. 1857) |

| Chairperson | Kumar Mangalam Birla |

| Headquarters | Mumbai, India |

| Employees | 68,400+ |

| FY2026 Revenue | ₹53,871 crore (14% YoY growth) |

| Total AUM (FY2026) | ₹5,91,343 crore |

| Lending Portfolio (FY2026) | ₹2,07,368 crore |

| Market Capitalisation | ~₹93,686 crore |

| Key Digital Platform | ABCD App with 1.1 crore customers |

| Main Competitors | HDFC Bank, ICICI Bank, Kotak Mahindra Bank, SBI Life Insurance |

Why Does a SWOT Analysis of Aditya Birla Capital Matter in 2026?

India's financial services sector is changing faster than ever, and ABCL sits right at the centre of that transformation.

- Rapidly Evolving Regulations: With the RBI, SEBI, and IRDAI rolling out sweeping reforms, understanding ABCL's regulatory exposure is critical for investors, students, and analysts alike.

- Digital-First Disruption: Fintech startups and neobanks are reshaping how Indians borrow, invest, and insure, placing ABCL simultaneously in the role of disruptor and target.

- The India Growth Story: India is set to become the world's third-largest economy by 2030, and financial penetration in insurance, mutual funds, and formal credit still has enormous room to grow.

- MSME Credit Gap: With 63+ million MSMEs in India, platforms like Udyog Plus are chasing a trillion-dollar lending opportunity that is only just opening up.

- GenAI Leadership: ABCL has deployed 22+ GenAI projects, cut AI operating costs by 30 to 40%, and won the Celent Model Bank Award 2025, making it a standout enterprise AI case study.

- Competitive Benchmarking: A SWOT analysis reveals exactly where ABCL leads and where it still needs to catch up against India's financial heavyweights.

Learn Digital Marketing for FREE

Learn Digital Marketing for FREE

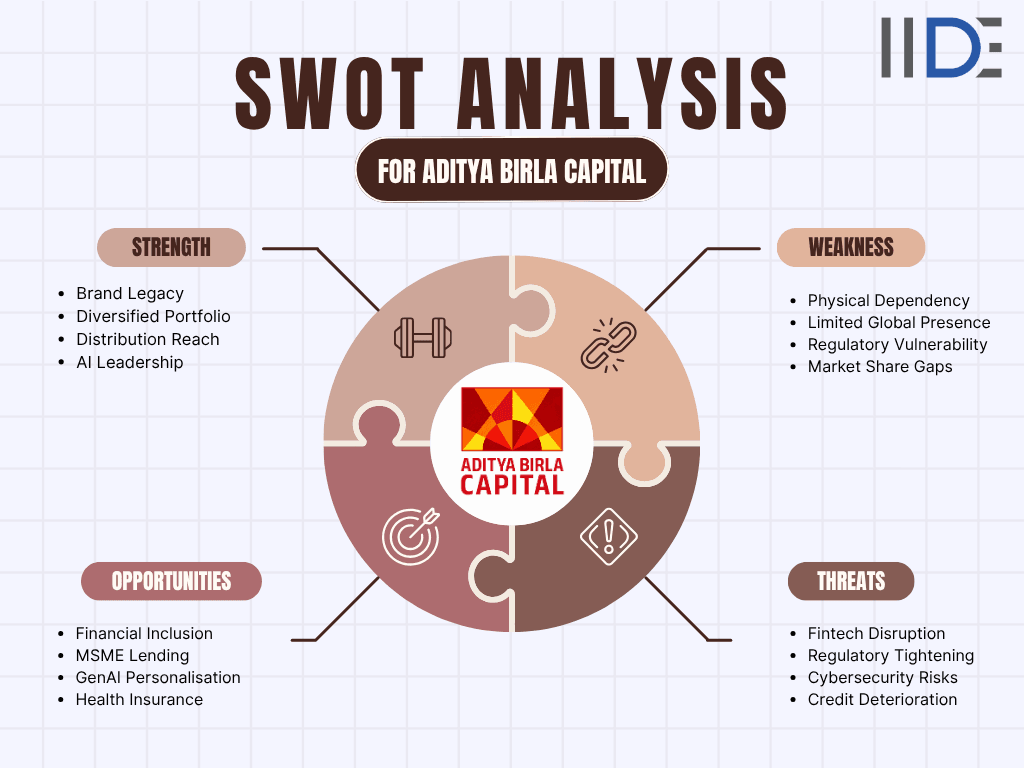

SWOT Analysis of Aditya Birla Capital

A SWOT analysis is more than a checklist it is a strategic lens that shows where a business truly stands and where it must head next. For ABCL, spanning nine segments from NBFC lending and housing finance to life insurance, asset management, and stock broking, this makes for a particularly compelling breakdown.

Strengths of Aditya Birla Capital: What Makes It a Market Leader in 2026

Iconic Brand Trust and Group Legacy:

- ABCL operates under the Aditya Birla Group, one of India's most trusted conglomerates with over 165 years of history.

- This brand heritage translates directly into consumer confidence, particularly in financial services where trust is non-negotiable.

- Customers who have interacted with Aditya Birla's cement, textiles, or telecom businesses are far more likely to explore its financial products, giving ABCL a built-in audience that few competitors can replicate.

Truly Diversified Financial Portfolio:

- Unlike banks constrained by their core model, ABCL offers a genuinely comprehensive suite of financial solutions.

- This includes life insurance, health insurance, general insurance broking, mutual funds, PMS, NBFC lending, housing finance, pension plans, stock broking, and digital payments, all under one roof.

- This diversification significantly reduces business concentration risk and allows the company to cross-sell products across its vast customer base, dramatically lowering customer acquisition costs.

Exceptional Distribution Reach:

- ABCL's on-the-ground presence is formidable.

- With 1,740+ branches, 2,00,000+ agents and channel partners, and tie-ups with major bank networks, the company reaches customers in Tier-1 cities as well as deeper geographies.

- Its life insurance subsidiary, Aditya Birla Sun Life Insurance, alone is supported by 26,300+ bank branches, 360+ own branches, and 60,000 agents across 4,700+ cities.

- This is a distribution architecture that would take a decade and billions of rupees for any new entrant to replicate.

Aggressive AI-First Digital Transformation:

- ABCL has made technology a genuine competitive differentiator, with its ABCD App serving 1.1 crore customers across 26+ product categories spanning loans, investments, insurance, and UPI payments.

- Udyog Plus has scaled to an AUM of ₹5,814 crore with 24 lakh MSME registrations, offering instant business loans and supply chain financing in a few clicks.

- SimpliFi, India's first GenAI-powered BFSI assistant built on Microsoft Azure OpenAI, has cut response latency from 30 seconds to under 1 second.

- With 22+ GenAI projects deployed, ABCL has reduced AI operating costs by 30 to 40% and won the Celent Model Bank Award 2025 for Excellence in Generative AI.

Strong and Consistent Financial Performance:

- In FY2026, ABCL posted a consolidated revenue of ₹53,871 crore, up 14% year-on-year, with net profit growing 21% to ₹3,797 crore.

- Q4 FY26 was particularly strong, with PAT jumping 30% year-on-year to ₹1,124 crore.

- The NBFC and Housing Finance lending book has more than tripled from FY22 to FY26, reflecting deep and sustained business growth.

- Consolidated PAT rising from ₹1,545 crore to ₹3,797 crore in just four years stands as a clear testament to ABCL's operational excellence.

Deep Human Capital and Talent Retention:

- With over 68,400 employees, ABCL benefits from the Aditya Birla Group's ability to attract premier talent.

- The Aditya Birla Group's strong employer reputation and structured leadership programmes help ABCL consistently attract top-tier professionals across actuarial, investment, technology, and distribution functions.

To understand how the parent group's brand strength and culture drives this talent advantage, explore the SWOT analysis of Aditya Birla Group the foundation on which ABCL's people strategy is built.

Weaknesses of Aditya Birla Capital: Challenges the Brand Must Address

Heavy Reliance on Traditional Distribution Channels:

- Despite its impressive digital push, a significant portion of ABCL's business, especially in life insurance and housing finance, still flows through physical branches, agents, and bancassurance partners.

- This dependence creates a structural cost disadvantage compared to digitally native competitors and limits ABCL's ability to serve high-growth tech-savvy consumer segments at scale and speed.

Comparatively Limited International Presence:

- While the Aditya Birla Group operates in 42 countries, ABCL's financial services operations remain overwhelmingly India-centric.

- Global peers like HDFC Bank or multinational insurers have far greater cross-border revenue diversification.

- This concentration in a single market, however large, exposes ABCL to domestic macro risks including currency volatility, inflation shocks, and politically driven policy changes.

Operational Complexity Across Nine Business Segments:

- Managing nine segments including NBFC lending, housing finance, life insurance, asset management, and digital payments introduces significant operational complexity.

- Aligning risk frameworks, compliance obligations, and technology systems across entities drives up overheads and slows decision-making.

- Maintaining consistency in customer data and internal processes across independently regulated business units remains a persistent challenge.

High Vulnerability to Regulatory Changes:

- ABCL operates under the simultaneous jurisdiction of multiple regulators, including the RBI (for NBFC and housing finance), SEBI (for asset management and broking), and IRDAI (for insurance).

- Any regulatory tightening such as stricter provisioning norms, new solvency requirements, or caps on insurance commission structures can materially impact profitability across one or more of its business lines.

- This multi-regulator exposure is a structural vulnerability that few single-product peers face.

Market Share Gaps in Key Segments:

- Despite being a large and growing player, ABCL does not hold a dominant market share position in several of its key segments.

- In life insurance, it trails behind LIC, HDFC Life, and SBI Life. In mutual funds, Aditya Birla Sun Life AMC competes against larger players like SBI Mutual Fund and HDFC AMC.

- Closing these gaps requires sustained capital investment, aggressive distribution expansion, and product innovation, all of which take time.

Opportunities for Aditya Birla Capital: Where Growth Is Waiting

India's Financial Inclusion Boom:

- India's financial services sector is at an inflection point. Insurance penetration stands at approximately 4% of GDP, well below the global average of 7%.

- Mutual fund penetration in Tier-2 and Tier-3 cities remains nascent, and formal credit access for the bottom of the pyramid is still limited.

- ABCL, with its distribution depth and digital infrastructure, is exceptionally positioned to capture this wave of first-time financial product consumers over the next decade.

MSME Digital Lending - A Trillion-Dollar Opportunity:

- India's 63+ million MSMEs represent one of the world's largest underserved credit markets, making it a trillion-dollar opportunity.

- Udyog Plus offers instant business loans up to ₹10 lakh, supply chain financing, and value-added services tailored for MSMEs.

- The platform has already clocked 24 lakh registrations and an AUM of ₹5,814 crore, reflecting strong product-market fit.

- As MSME formalisation accelerates through GST data and OCEN, ABCL's digital infrastructure gives it a clear first-mover advantage.

Generative AI and Data-Driven Personalisation:

- ABCL's ongoing investment in GenAI creates a compounding advantage.

- By deploying AI across sales, servicing, audit, marketing, and finance, the company is simultaneously reducing costs and improving customer experience.

- As AI capabilities advance, ABCL can leverage its vast proprietary customer data to offer hyper-personalised financial advice, predictive product recommendations, and real-time risk assessment at a scale that human advisors cannot match.

Expanding the "One ABC" Cross-Selling Ecosystem:

- ABCL's "One ABC, One P&L" strategy, which aims to make every customer a user of multiple ABCL products, represents a significant untapped revenue opportunity.

- With 1.1 crore ABCD app users but a far larger universe of 40+ million customers across its various businesses, the cross-sell and upsell potential is enormous.

- Each successful cross-sell also dramatically improves customer lifetime value and reduces churn.

Strategic Acquisitions, Partnerships, and International Expansion:

- With a market cap of Approx ₹93,686 crore and strong institutional backing, ABCL is well-placed to pursue acquisitions in health-tech, wealth-tech, or regional microfinance.

- Strategic partnerships in Southeast Asia or Gulf markets could unlock meaningful international revenue through the large, financially active Indian diaspora.

- Both moves would reduce domestic market dependence and fast-track entry into high-potential adjacent segments.

Health Insurance - The Next Big Frontier:

- India's health insurance penetration stands at under 40% of the population, with a large segment relying exclusively on government schemes.

- ABCL's health insurance subsidiary, Aditya Birla Health Insurance, is already differentiated through its "Activ Health" model, which rewards customers with health returns for maintaining healthy behaviour.

- As healthcare costs rise and post-pandemic awareness of health coverage grows, this segment holds enormous long-term potential.

Threats to Aditya Birla Capital: Risks That Demand Vigilance

Intensifying Competition from Banks and Fintech Players:

- ABCL faces a two-front competitive battle.

- On one side, banking giants like HDFC Bank, ICICI Bank, Kotak Mahindra Bank, and SBI are aggressively expanding their financial product portfolios, often bundling insurance and investment products at lower costs.

- On the other side, nimble fintech startups such as Groww, PolicyBazaar, Zerodha, and Navi are acquiring millions of young digital-first customers at low cost, directly eroding ABCL's addressable market.

For context on how a close rival is navigating the same pressures, the SWOT analysis of Bajaj Finserv makes for a compelling read another diversified financial player fighting the same battle in India's fast-evolving market.

Regulatory Tightening Across Multiple Fronts:

- The RBI, SEBI, and IRDAI have all signalled a more interventionist approach to financial services regulation in 2025 and 2026.

- The RBI's tightened norms on NBFC provisioning and risk weights pose a direct threat to ABCL's lending business margins.

- SEBI's scrutiny of asset management fee structures and IRDAI's push for expense management in insurance add further margin pressure across business lines.

- This risk of simultaneous regulatory tightening across multiple fronts is unique to diversified financial conglomerates like ABCL.

Cybersecurity and Data Privacy Risks:

- As ABCL processes financial data for tens of millions of customers across nine business lines, it becomes an increasingly attractive target for cyberattacks.

- A significant data breach could trigger heavy regulatory penalties under the Digital Personal Data Protection (DPDP) Act 2023.

- In financial services, where trust is the foundational currency, even a single breach could cause irreparable reputational damage that no marketing campaign can reverse.

Economic Slowdowns and Credit Quality Deterioration:

- ABCL's NBFC and housing finance businesses are directly exposed to the credit cycle, making them sensitive to macroeconomic shifts.

- Global headwinds, domestic inflation, or job market stress can trigger a rise in non-performing assets (NPAs) and force higher provisioning.

- This compresses net interest margins and puts pressure on overall profitability across lending business lines.

- Although ABCL's current Gross Stage 3 ratio stands at a healthy 2.80%, sustaining asset quality during economic downturns remains a constant challenge.

Talent War in Financial Technology:

- Building and retaining top-tier data scientists, AI engineers, and product managers is increasingly difficult in India's competitive talent market.

- Global tech giants, well-funded fintech startups, and international financial services firms actively poach talent from established players like ABCL.

SWOT Summary Table: Aditya Birla Capital 2026

IIDE Student Takeaway, Recommendations & Conclusion for Aditya Birla Capital in 2026 and Beyond

Aditya Birla Capital enters the second half of 2026 from a position of genuine strength. Its FY26 results, which include 14% revenue growth, 21% profit growth, and a 32% expansion in its lending portfolio, confirm that the business model is working.

The real question is not whether ABCL can sustain current performance, but whether it can use this momentum to leap into the next tier of Indian financial services leadership.

Core Tension: ABCL must accelerate its digital-first future without alienating the traditional agent network that still drives the majority of its insurance and lending revenues. Moving too fast or too slow both carry real risks.

Future Outlook: The next three to five years will be defined by how effectively ABCL executes the "One ABC" strategy, converting its 40 million+ customers into multi-product, digitally engaged relationships where each additional product dramatically improves loyalty and profitability.

Strategic Recommendations:

- Double down on the ABCD platform: Target 3 crore active users by FY28 by deepening engagement features, adding vernacular language support, and integrating more embedded finance use cases

- Aggressively capture the MSME lending opportunity: Scale Udyog Plus with expanded credit products, co-lending partnerships, and deeper rural penetration through banking correspondents

- Invest in regulatory technology (RegTech): Build proprietary compliance monitoring systems to reduce the cost and risk of operating under multiple regulators simultaneously

- Expand international presence selectively: Target the Gulf Cooperation Council (GCC) region and Southeast Asia, where the Indian diaspora's financial services needs are significantly underserved

- Strengthen cybersecurity infrastructure: As the custodian of tens of millions of customers' financial data, ABCL must treat data security as a board-level strategic priority, not just an IT function

- Differentiate through financial wellness: Leverage ABCL's Activ Health model and GenAI capabilities to build India's first genuinely integrated financial and physical wellness platform, a space no competitor currently occupies

Aditya Birla Capital is not just another financial holding company. It is one of India's most ambitious bets on the convergence of technology, financial inclusion, and the aspirations of 1.4 billion people building better financial lives.

The FY2026 results say it all. Revenue grew 14%, net profit rose 21%, and the lending portfolio expanded 32%, confirming that ABCL's momentum is real and building.

Backed by 165 years of brand trust, a thriving ABCD platform with 1.1 crore customers, and 22+ GenAI projects already delivering results, ABCL has built advantages that no fintech startup can replicate overnight.

Challenges around regulatory complexity, distribution dependence, and intensifying competition are real, but ABCL has consistently adapted, invested, and grown through every cycle.

With focused execution of the "One ABC" strategy and continued digital innovation, ABCL is well on its way to becoming India's defining financial services institution of the 2030s.

Want to Know Why 2,50,000+ Students Trust Us?

Dive into the numbers that make us the #1 choice for career success

MBA - Level

Post Graduate in Digital Marketing & Business Strategy

Best For

Fresh Graduates

Mode of Learning

On Campus (Mumbai & Delhi)

Starts from

Oct 1, 2026

Duration

11 Months

Live & Online

Advanced Online Digital Marketing Course

Best For

Working Professionals

Mode of Learning

Online

Starts from

Aug 7, 2026

Duration

4-6 Months

Online

Professional Certification in AI Strategy

Best For

AI Enthusiasts

Mode of Learning

Online

Starts from

Sep 8, 2026

Duration

5 Months

On Campus

Advanced Certification in Artificial Intelligence

Best For

AI Enthusiasts

Mode of Learning

On Campus (Mumbai)

Starts from

Sep 1, 2026

Duration

3 Months

Online or Offline

Top AI Courses to Make You Future Ready!

Best For

AI Enthusiasts

Mode of Learning

2–5 Month Program

Starts from

Sep 8, 2026

Duration

Flexiable

Offline

Undergraduate Program in Digital Business & Entrepreneurship

Best For

12th Passouts

Mode of Learning

On Campus (Mumbai)

Starts from

Aug 19, 2026

Duration

3 Years

Offline

Degree In 2026 ≠ Enough Degree + Digital Skills = Future-Ready

Best For

12th Passouts

Mode of Learning

At IIDE Campus

Starts from

Aug 6, 2026

Duration

3 Years

Recent Post

You May Also Like

Aditya Birla Capital Limited (ABCL) is a leading diversified financial services company under the Aditya Birla Group, offering life insurance, asset management, NBFC lending, wealth management, health insurance, and broking services all under one roof.

ABCL competes with HDFC Ltd, ICICI Prudential, Bajaj Finserv, SBI Life, Kotak Mahindra, and Mirae Asset across its various financial services verticals including lending, insurance, and asset management.

ABCL has invested heavily in digital platforms, launching paperless KYC, online account opening, robo-advisory tools, and mobile-first customer experiences positioning itself strongly to serve India's rapidly growing digital-savvy investor base.

ABCL was incorporated in 2007 as an NBFC and operates as a majority-owned subsidiary of the Aditya Birla Group.

With ₹4 lakh crore+ in managed assets and a 150+ year group legacy, ABCL is one of India's most trusted and comprehensive financial services brands.

Lead Trainer & Business Development Head at IIDE

Aditya Shastri leads the Business Development segment at IIDE and is a seasoned Content Marketing expert. With over a decade of experience, Aditya has trained more than 20,000 students and professionals in digital marketing, collaborating with prestigious institutions and corporations such as Jet Airways, Godrej Professionals, Pfizer, Mahindra Group, Publicis Worldwide, and many others. His ability to simplify complex marketing concepts, combined with his engaging teaching style, has earned him widespread admiration from students and professionals alike.

Aditya has spearheaded IIDE’s B2B growth, forging partnerships with over 40 higher education institutions across India to upskill students in digital marketing and business skills. As a visiting faculty member at top institutions like IIT Bhilai, Mithibai College, Amity University, and SRCC, he continues to influence the next generation of marketers.

Apart from his marketing expertise, Aditya is also a spiritual speaker, often traveling internationally to share insights on spirituality. His unique blend of digital marketing proficiency and spiritual wisdom makes him a highly respected figure in both fields.